Best Budgeting Apps 2026: Honest Picks for Real Life

Your money doesn’t need “a budget.” It needs a lie detector.

Because in 2026, the default setting for modern life is: frictionless spending, 17 subscriptions you didn’t approve, and a credit card that quietly whispers “treat yourself” like it’s your therapist.

And you’re not alone. A reported 60% of Americans are living paycheck to paycheck (yes, even plenty of high earners), according to CNBC’s coverage of recent survey data. The problem isn’t that people are dumb. It’s that money is now invisible until it’s catastrophic.

So let’s talk best budgeting apps 2026 style, with zero fluff, real trade-offs, and picks that survive real life (kids, chaos, travel, side hustles, and the occasional “we deserved it” weekend).

What “best” actually means in 2026 (hint: not the prettiest charts)

Most budgeting app reviews act like you’re a robot with one job: “Optimize.”

Real humans have different jobs:

- “Stop overdrafting because my autopay schedule looks like a Jackson Pollock painting.”

- “Figure out why I’m broke when I make decent money.”

- “Get a clean savings rate so FIRE isn’t just a Pinterest board.”

- “Handle irregular income without sweating through my shirt.”

A budgeting app is only “best” if it helps you do three things consistently:

- See the truth (clean, accurate transactions).

- Make decisions (clear categories, budgets, safe-to-spend, alerts).

- Stick with it (automation, low friction, fast weekly check-ins).

If an app can’t do those, it’s not a budgeting tool. It’s financial entertainment.

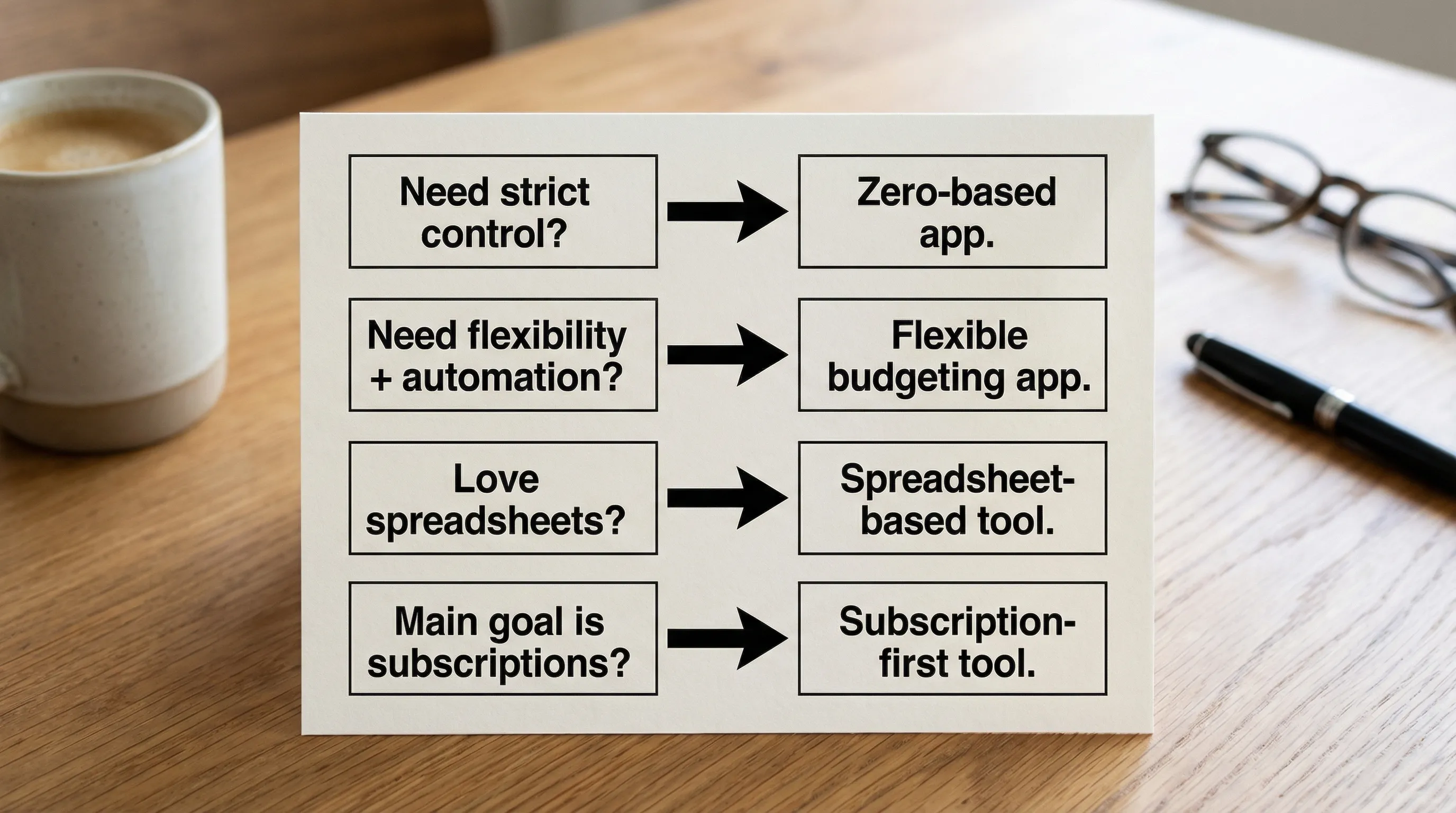

The 5-question filter: how to choose the right budgeting app fast

Before you download seven apps and spiral into analysis paralysis, answer these.

1) Are you trying to budget, or just track spending?

Tracking tells you what happened.

Budgeting tells your money where to go next.

If you’re currently in “I need to stop bleeding money” mode, start with tracking. Once the bleeding slows, you can layer in budgets.

2) Do you want strict rules or flexible guardrails?

Some people need a drill sergeant. Others need bumpers.

- If you want a strict plan where every dollar has a job, you’ll like zero-based systems.

- If you want a realistic plan that bends with real life, you’ll like flexible budgeting with category caps and ranges.

3) Is your income predictable?

If you’re freelance, commission, self-employed, or gig-based, you’re not “bad with money.” You’re dealing with a cash-flow problem.

Choose a tool that can handle:

- Income swings

- Buffering

- Easy category customization

- Rules that reduce manual cleanup

4) Do you need subscription visibility?

Subscription creep is the modern tax. The charge is small, the pain is slow, and one day you’re paying $19.99 a month for an app you used once to identify a plant.

If you have a lot of recurring charges, prioritize a tool with subscription tracking and a clean recurring-spend view.

5) Are you trying to build wealth (not just “be good”)?

If you care about FIRE, retirement, debt payoff, or long-term goals, budgeting alone is not enough.

You want a system that ties together:

- Spending

- Savings rate

- Net worth

- Goals (and ideally an FI timeline)

If your app can’t connect today’s choices to your long-term timeline, you’re driving with a broken GPS.

The honest picks: best budgeting apps for 2026 (real-life edition)

Below are the tools that show up in actual adult life, not just app store screenshots.

| App | Best for | What it’s great at | Watch-outs (the honest part) |

|---|---|---|---|

| FIYR | Mint refugees, FIRE-minded planners, people who want customization without chaos | Spending + budgeting + net worth + savings rate + FIRE insights in one place | If you want ultra-strict zero-based methodology above all else, you might prefer a tool built specifically for that |

| YNAB | People who want strict control and a proven method | Zero-based budgeting, behavior change through structure | Can feel intense if you just want “keep me on track” guardrails |

| Monarch Money | Households who want a premium, shared view | Strong overall budgeting and visibility for many users | If you want the simplest possible workflow, some people find it heavier than necessary |

| Copilot Money | Apple-first users who want a sleek experience | Beautiful UX and strong day-to-day tracking for many | Best fit is often Apple ecosystem, and some users want deeper long-term planning tooling |

| Rocket Money | Subscription-heavy users who want recurring-charge visibility | Good focus on finding recurring expenses | If you want deeper budgeting systems and FIRE-style planning, you may want a more full-stack finance app |

| Tiller | Spreadsheet lovers who want total control | Custom spreadsheets, maximum flexibility | Setup and maintenance are real work, if you don’t like spreadsheets, don’t cosplay as someone who does |

| Quicken Simplifi | People leaving legacy tools who still want structure | Traditional personal finance management with modern touches | If you want a cleaner, more customizable budgeting feel, you may prefer a newer “rules + categories” style app |

| Empower Personal Dashboard | People who want a free net worth and investment view | Net worth tracking and portfolio visibility | Budgeting features are not the main event |

Now the quick mini-reviews, with who each tool is actually for.

FIYR: best for people who want budgeting plus a real path to financial independence

If Mint was your financial home base and you’re now wandering the app store like it’s a post-apocalyptic wasteland, FIYR is built for that exact moment.

What FIYR does well (especially in 2026):

- Full money tracking: income, expenses, assets, liabilities, net worth

- Flexible budgeting: dynamic budgets instead of rigid fantasy caps

- Custom categories and category groups: so your budget matches your life, not someone else’s template

- Automatic transaction rules: fewer “why is Costco in Entertainment?” moments

- Subscription tracking: recurring charges don’t get to hide

- Savings rate + FIRE date calculator: because “someday” is not a plan

- Goal tracking and safe-to-spend: clarity without obsessive spreadsheet behavior

The vibe: FIYR is for people who want control without becoming a part-time accountant.

If you want to go deeper on the Mint transition, this pairs well with: FIYR vs Mint: Which Budgeting Style Fits You Best in 2026?

Quotable truth: Your budget shouldn’t require a weekend retreat and a color-coded binder.

YNAB: best for strict zero-based budgeting (the “every dollar has a job” crowd)

YNAB is the budgeting equivalent of meal prepping.

If you do it, it works. If you don’t do it, it doesn’t. No mystery. No magic.

Best for:

- People who want strict intentionality

- Households that need a hard system (especially after debt or overspending)

- Anyone who likes structure and doesn’t mind being told “no” by their own categories

The trade-off: if you’re looking for flexible guardrails, YNAB can feel like it’s yelling at you for buying strawberries.

Quotable truth: YNAB isn’t a budget, it’s a lifestyle.

Monarch Money: best for households that want a premium shared dashboard

If you want a more polished, household-level view and you’re coordinating money across multiple accounts, Monarch is a common pick.

Best for:

- Couples and families who want shared visibility

- People who want a “finance HQ” feel

The trade-off: some users want simpler workflows and faster setup. If you’re allergic to complexity, it can feel like a lot.

Quotable truth: The best app is the one you’ll still open when life gets busy.

Copilot Money: best for Apple-first users who care about UX

Copilot is the cool minimalist apartment of budgeting apps. Clean. Sleek. Calm.

Best for:

- Apple ecosystem users

- People who want a modern, smooth day-to-day experience

The trade-off: depending on what you want (FIRE forecasting, deeper customization, more planning), you may want something more explicitly built for long-term independence planning.

Quotable truth: Pretty charts don’t pay bills, but they can get you to look at them.

Rocket Money: best for subscription-heavy households that want recurring charges visible

If your bank statement looks like a graveyard of “$9.99 monthly” charges, Rocket Money is often on the shortlist.

Best for:

- People trying to reduce recurring expenses

- Anyone who wants subscription visibility front and center

The trade-off: if your goal is a full budgeting system plus net worth tracking and FIRE-style metrics, you may outgrow a subscription-first tool.

Related reading if you want to go full subscription detective: Best Apps to Manage Subscription Renewals

Quotable truth: Subscriptions are the financial equivalent of termites, small, quiet, expensive.

Tiller: best for spreadsheet people (and people who think they’re spreadsheet people)

Tiller is for the control freaks (said with love). It’s a spreadsheet-based system with automation, and it can be incredibly powerful.

Best for:

- People who already live in spreadsheets

- Anyone who wants full customization and doesn’t mind setup

The trade-off: you’re choosing flexibility over convenience. If your idea of fun isn’t “debugging a template,” you may hate it.

Quotable truth: If you won’t track it weekly, don’t build it like NASA.

Quicken Simplifi: best for people who want a more traditional personal finance manager

Simplifi is often considered by people leaving older tools and wanting a familiar structure.

Best for:

- Users who want a more traditional approach

- People transitioning from legacy software but not ready for pure spreadsheet life

The trade-off: if you want more modern customization and automation-first budgeting workflows, newer platforms can feel more natural.

If you’re coming specifically from Quicken-style budgeting, this is a useful comparison path: Quicken Alternatives for 2026: Better Budgeting Apps for Modern Users

Quotable truth: Legacy tools teach discipline. Modern tools remove friction.

Empower Personal Dashboard: best for free net worth and investment visibility

If your main goal is seeing your net worth and investments in one place, Empower is a common free option.

Best for:

- People who want net worth visibility without paying for a budgeting suite

- Investors who prioritize portfolio-level views

The trade-off: it’s not built first and foremost as a budgeting OS.

Quotable truth: Net worth tracking is the scoreboard, budgeting is the practice.

Real-life matchups: which budgeting app fits your actual situation?

This is where things get interesting, because “best” changes based on the problem you’re solving.

Scenario 1: The Mint refugee who wants a clean replacement (without starting over emotionally)

Meet Jake.

Jake used Mint for years. Not because it was perfect, but because it was familiar. Now he’s trying three apps at once, which is the budgeting version of dating six people and wondering why you’re exhausted.

Jake needs:

- Spending tracking that doesn’t require constant manual cleanup

- Custom categories so his budget isn’t forced into someone else’s box

- Subscription visibility (because Jake absolutely is paying for something called “Pro Upgrade”)

- Net worth and savings rate so he can track progress, not just guilt

This is a strong FIYR use case, especially if Jake is also thinking about FIRE and wants to connect spending to timelines.

If Jake’s bigger issue is that he doesn’t have a budgeting rhythm, start here: Why Budgets Fail (And How to Fix Yours in 2026)

Scenario 2: The couple who wants fewer fights and more clarity

Meet Priya and Dan.

They don’t need “a better budget.” They need a better system for shared decisions.

They need:

- Shared visibility

- Categories that match reality (childcare is not “miscellaneous,” it’s a small GDP)

- A quick weekly check-in rhythm

If you’re building a shared money system, read: Budgeting for Couples: Build a System You Both Can Trust

Tool-wise, people often look at Monarch for shared household dashboards, and FIYR if they want customization, automation, and FIRE metrics without a heavy workflow.

Scenario 3: The freelancer whose income swings like a crypto chart

Meet Alex.

Alex has great months and terrifying months. Budgeting advice that starts with “just set a fixed amount” makes Alex want to scream into a pillow.

Alex needs:

- Flexible budgeting

- Clear income and expense tracking

- Buffer visibility

- Categories and rules that reduce manual sorting

If you’re in this boat, build the system first: Budgeting With Irregular Income: A Practical System That Actually Works

Quotable truth: Irregular income doesn’t need willpower, it needs a buffer.

The “test drive” method: how to evaluate any budgeting app in 30 minutes

Don’t pick a budgeting app by vibes. Pick it by whether it survives the following.

Step 1: Check data truth (10 minutes)

Pick the last 30 to 60 days and look for:

- Duplicates

- Missing transactions

- Transfers miscategorized as spending

- Refunds treated like income

If the data is messy, your budget will be fiction.

For a deeper checklist (and what to demand from a tracker), use: Spending Tracker App Checklist: What to Demand

Step 2: Build categories that match decisions (10 minutes)

Create categories that answer real questions:

- “Are we eating out too much?”

- “Are fixed costs crowding out savings?”

- “How much are subscriptions actually costing us?”

A killer move in FIYR is using custom categories and labels for real-life tracking like “New York Trip 2025” so you can see the full cost without wrecking your monthly categories.

If you want a clean category setup, start here: Budgeting Categories List: A Clean Setup That Works

Step 3: Stress test the workflow (10 minutes)

Ask:

- Can I do a weekly check-in in 10 to 15 minutes?

- Can the app automate the boring parts (rules, recurring items, clean categorization)?

- Does it show me a “safe-to-spend” style signal or clear category caps?

If you dread opening it, it will die by week three. Like most New Year’s resolutions.

A simple decision framework (so you actually pick one)

Here’s the decision tree I wish more people used.

And yes, you can mix approaches, but start with the tool that solves your biggest bottleneck.

- If your problem is overspending and you need structure, choose strict.

- If your problem is chaos and inconsistency, choose flexible plus automation.

- If your problem is recurring charges, choose subscription visibility.

- If your problem is long-term planning, choose net worth plus savings rate plus goals.

Quotable truth: The best budgeting app is the one that turns stress into a system.

How FIYR fits in (without the salesy nonsense)

FIYR shines when you want one place to run your financial life, not five different apps that each know one fun fact about your bank account.

It’s especially useful if you care about:

- Accurate spending tracking with customizable categories

- Automation via transaction rules so your budget doesn’t degrade into a cleanup project

- Subscription tracking so recurring charges stop ambushing you

- Savings rate and net worth tracking so you can measure progress, not just activity

- FIRE-focused insights like a FIRE date calculator, based on real data

If you want to connect budgeting to the actual math of freedom, pair this with: FIRE Number Formula Explained in Plain English

The final takeaway (the one you’ll remember)

The budgeting app isn’t the goal. The goal is making money boring.

Boring means:

- Bills are handled.

- Spending is intentional.

- Subscriptions don’t multiply like gremlins.

- Savings happens automatically.

- Net worth trends up.

Pick a tool that helps you tell the truth, make decisions, and keep going when life gets messy.

Because the real flex in 2026 isn’t a perfectly optimized budget.

It’s waking up with options.