Budgeting With Irregular Income: A Practical System That Actually Works

Most budgets are built for people with neat paychecks and tidy lives. If your income swings like a crypto chart, that advice feels like a prank. Here is the truth, budgeting with irregular income is not about predicting paydays, it is about installing a system that pays you on schedule even when clients, commissions, or gigs do not.

Meet the roller-coaster crew

Ava is a freelance designer. January was a desert, February was payday-palooza, March was… who knows. She kept trying to “tighten up” in slow months and “catch up” in big months. It was exhausting, and worse, it was expensive. Panic swipes carry interest.

Then she made one change, she stopped guessing and started paying herself a steady salary from a buffer account. Same work, same chaos, new system. Suddenly the bills got boring, which is the goal.

Here is the part nobody talks about, irregular income is a volatility problem, not a morality problem. You do not need more discipline, you need a shock absorber.

The data gut-check

- According to CNBC, about 60 percent of Americans still live paycheck to paycheck, even many six-figure earners. That is a volatility problem in disguise. Source.

- Surveys in 2023 and 2024 consistently show roughly 70 percent of people feel stressed about money, only around 45 percent report an emergency fund, and roughly 3 in 5 carry credit card balances around six thousand dollars on average.

When income is lumpy, stress spikes, spending gets reactive, and high-interest debt sneaks in. The cure is not another color-coded spreadsheet. It is a simple cash-flow engine.

The insight

Predictable bills with unpredictable deposits require a translator. You smooth income into a salary, you flatten big annual costs into monthly “sinking funds,” and you rank your spending by priority so cuts are automatic, not emotional. The budget becomes a policy, not a mood.

Here is the system that works for freelancers, gig workers, and commission-based pros.

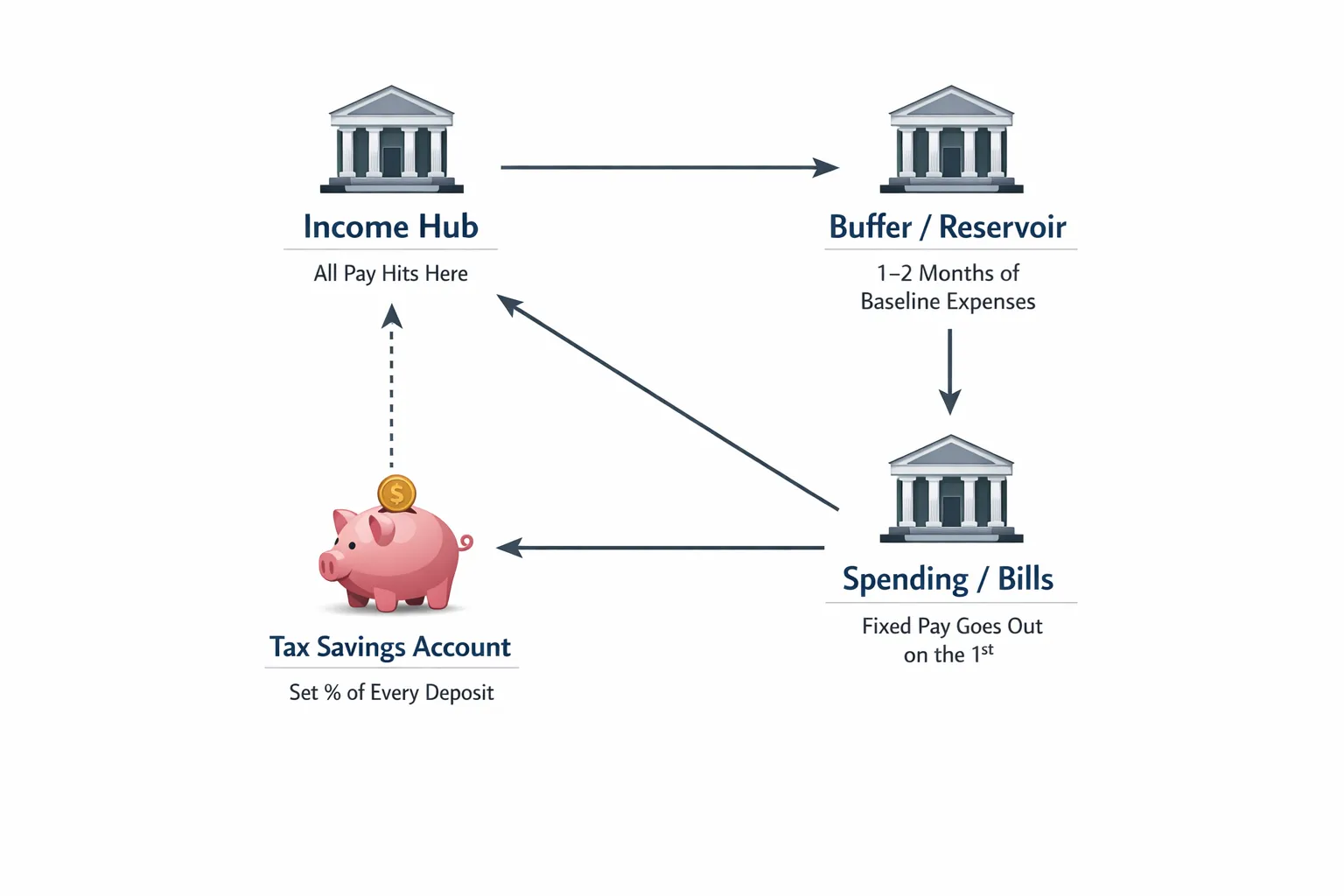

---The 3-account system for irregular income

Think of this like your own tiny payroll department. Three accounts, four rules.

- Income Hub, all deposits land here.

- Buffer, your reservoir that holds 1 to 2 months of baseline expenses.

- Spending/Bills, the account you pay yourself into, same amount, same date.

- Tax Savings, for 1099 or commission income, skim a percent of every deposit here and do not touch it.

One-liner, you cannot control when clients pay, but you can control when you pay yourself.

---Step 1, build your baseline and priority categories

Your baseline budget is what it takes to keep the lights on, rent or mortgage, utilities, groceries, transport, minimum debt, insurance, phone, internet, childcare. This is not your “ideal life,” it is your monthly floor.

Then classify everything into priority buckets so cuts are surgical, not chaotic.

- Must, essentials and minimum debt payments.

- Should, practical but flexible spending like groceries above bare minimum, gas, basic personal care.

- Could, discretionary wants, dining out, travel, subscriptions, fun money.

- Growth, investments, extra debt payoff, professional development.

Treat non-monthly bills like they happen monthly. If car insurance is 1,200 dollars every six months, you set aside 200 dollars per month into a sinking fund. No more budget ambushes.

| Category | Priority | Baseline monthly | Stretch monthly | Notes |

|---|---|---|---|---|

| Housing + utilities | Must | 1,650 | 1,650 | Fixed bills |

| Groceries | Should | 450 | 650 | Floor vs nicer-to-have |

| Transport | Should | 220 | 300 | Gas, transit, rideshare |

| Insurance sinking funds | Must | 200 | 200 | Annualized cost divided by 12 |

| Minimum debt payments | Must | 180 | 180 | Keep credit score intact |

| Phones + internet | Must | 140 | 140 | Fixed |

| Subscriptions | Could | 30 | 120 | Trim aggressively |

| Dining + fun | Could | 100 | 300 | Weekly allowance works well |

| Growth, investing/extra debt | Growth | 0 | 500 | Fill once buffer is healthy |

Numbers are sample placeholders, swap yours in. The point is structure, not perfection.

One-liner, priorities turn cuts into policy, not pain.

---Step 2, set your buffer target

Target 1 month of baseline expenses to start, then stretch to 2 months. This is separate from your emergency fund. The buffer smooths income, the emergency fund covers actual emergencies. Different jobs.

How to seed it fast, funnel every extra dollar from big months until you hit target. Sell unused gear, list a small retainer with a current client, or take overflow gigs during busy seasons. Momentum beats elegance.

One-liner, first you buy stability, then you buy freedom.

---Step 3, income averaging that pays you a salary

Set your monthly “salary” using a rolling average so you are not guessing.

- Formula, average the last 3 months of net business income, after skim for taxes and business costs. If very lumpy, use 6 months.

- Choose a salary slightly below that average to be conservative. Example, if the 3-month average net is 5,400 dollars, set salary at 4,800 dollars.

- Pay yourself on the same date each month from the Buffer into Spending/Bills. Let automation do the boring thing.

Keep the salary stable for at least a quarter unless reality forces a change. Stability builds habits, habits build wealth.

One-liner, your budget is now clocked in, even when your clients are not.

---Step 4, install a paycheck distribution rule

Every deposit hits Income Hub and triggers the same sequence.

- Taxes, skim 25 to 35 percent to Tax Savings if you receive 1099 or commission income without withholding.

- Buffer refill, until Buffer equals your target, send extra cash there.

- Next payroll, if your buffer is healthy, top up to guarantee next month’s salary.

- Sinking funds and Growth, only after steps 1 to 3.

If a slow month drains the Buffer, your salary still lands. Your system absorbs the shock while you work on pipeline.

One-liner, pay policies, not feelings.

---Step 5, flatten the annual costs

Annual or quarterly bills are what nuke irregular income budgets. Make them monthly through sinking funds.

- Divide the annual amount by 12 and move that number each month. Car maintenance, insurance premiums, software, professional dues, holiday travel.

- Shop the big-ticket items once a year. Cutting 30 to 50 dollars per month from insurance is the cheapest pay raise on earth.

If you are based in the UAE, you can compare and buy insurance online in the UAE to lock in better rates on car, health, home, or life plans and turn lumpy premiums into a sane monthly line item. Price stability is a budgeting superpower.

One-liner, the only surprise bill you want is a tax refund.

---What to do in droughts and windfalls

Droughts happen. So do pop-off months. Pre-decide your moves.

- Drought mode, keep paying yourself the same salary until Buffer drops below 1 month. Then cut “Could” by 100 percent, “Should” by 20 percent, and pause Growth. Rebuild Buffer first when cash returns.

- Windfall mode, allocate with a simple split, 50 percent to Buffer until full, 30 percent to Growth, 20 percent to fun or upgrading “Should” for the month. Or pick 60, 20, 20. The point is that you picked it.

Decisions made in calm beat decisions made at midnight on the 29th.

One-liner, luck favors the pre-committed.

---The weekly rhythm that keeps spending honest

Give yourself a weekly allowance for the flexible stuff, groceries, gas, dining, personal. Move that money every Monday from Spending to a debit card or separate “allowance” sub-account. When it is gone, it is gone. No scolding, just a reset next week.

A weekly cycle shortens feedback loops and slams the door on end-of-month chaos.

One-liner, most budgets fail in the last 10 days of the month, yours will not.

---The simple template

Copy, paste, edit, done.

Baseline monthly expenses, list your Musts and minimums

- Housing + utilities, $____

- Groceries (floor), $____

- Transport (gas/transit), $____

- Insurance sinking funds, $____

- Minimum debt payments, $____

- Phones + internet, $____

- Childcare/medical basics, $____

Baseline total, $____

Buffer target, Baseline x 1 to 2 months = $____

Monthly salary to self, $____, paid on the 1st (or the 15th)

Paycheck distribution rule (every deposit)

- Taxes set-aside, ____% to Tax Savings

- Buffer refill, until Buffer hits target

- Next payroll top-up, guarantee next month’s salary

- Sinking funds and Growth

Priority categories

- Must, rent, utilities, minimum debt, insurance

- Should, groceries above floor, gas, basic personal care

- Could, dining, subscriptions, shopping, travel

- Growth, investing, extra debt payoff, professional development

Weekly allowance, move $____ every Monday for groceries, gas, dining, personal

Quarterly review checklist

- Update 3 to 6 month income average

- Adjust salary if needed

- Re-shop 2 to 3 big bills

- Audit subscriptions and cancel at least one

One-liner, templates turn intentions into routines.

---Pro tips for freelancers, gig workers, and sales pros

- Use retainer or minimums, convert one-off clients into small retainers that cover part of your baseline. Even 400 dollars per month smooths the ride.

- Stage invoices, 50 percent upfront, 25 percent mid-project, 25 percent on delivery. Cash flow beats markdowns.

- Auto-transfer taxes weekly, your future self will sleep better and so will your accountant.

- Label non-monthly costs by month, car maintenance April and October, insurance March and September, conferences June. Seasonality reveals itself fast.

- Give yourself a raise carefully, only lift your salary after three strong months and a full Buffer. Then lock it for a quarter.

One-liner, be the CFO who signs your paycheck, not the intern who asks for advances.

---Where FIYR helps, without the hard sell

You can run this system on a whiteboard. It is just faster with a tool built for people who do not earn on a perfect schedule.

- Custom categories and labels, tag spending by project, client, or season, like “Q3 Estimated Taxes,” “New York Trip 2025,” or “Car Insurance Oct.”

- Transaction rules, auto-categorize income streams and recurring bills so your baseline stays accurate.

- Dynamic budgets and safe-to-spend, turn sinking funds and weekly allowances into guardrails you actually follow.

- Net worth and savings rate tracking, watch progress and volatility shrink, which is how FIRE timelines get real.

- FIRE date projections, once your baseline and savings rate stabilize, model your independence date and track it like a project.

The point is control, not complexity. If you want the all-in-one tracker designed for FIRE-minded users and irregular income, FIYR ties the daily spend, the monthly buffer, and the long game together.

---

--- The bottom line

Budgeting with irregular income is not a punishment, it is a payroll you run for yourself. Smooth the income with a Buffer, flatten the expenses with sinking funds, and let priorities make the tough calls. You are not guessing anymore, you are operating.

Today’s move, set a salary, name your Buffer target, and pick a start date. By next month your cash flow will feel boring. Boring is the new rich.