FIRE Number Formula Explained in Plain English

You don’t need a vision board to hit FIRE. You need a formula.

Because your “FIRE number” is not a mystical destiny number whispered by a minimalist influencer in linen pants. It’s just the amount of money your investments need to cover your yearly spending, reliably, for a long time.

Here’s the uncomfortable truth: most people don’t know what they spend, they vibe what they spend. And vibes don’t compound.

In a world where 60% of Americans live paycheck to paycheck and money stress is basically a national hobby, “I think I spend about…” is not a strategy. It’s a plot twist.

What your FIRE number actually is (and what it isn’t)

Your FIRE number is the size of the portfolio you need so you can stop trading hours for dollars and still pay for:

- Your lifestyle (housing, food, fun, healthcare, taxes, the occasional existential crisis)

- Your future (inflation, market drops, longer life)

It is not:

- Your net worth goal (net worth includes your house, your car, and your dusty Peloton)

- A flex (no one is impressed by your spreadsheet if your life is miserable)

- A single “set it and forget it” number (life changes, your plan should too)

Memorable takeaway: FIRE is a math problem wearing a lifestyle costume.

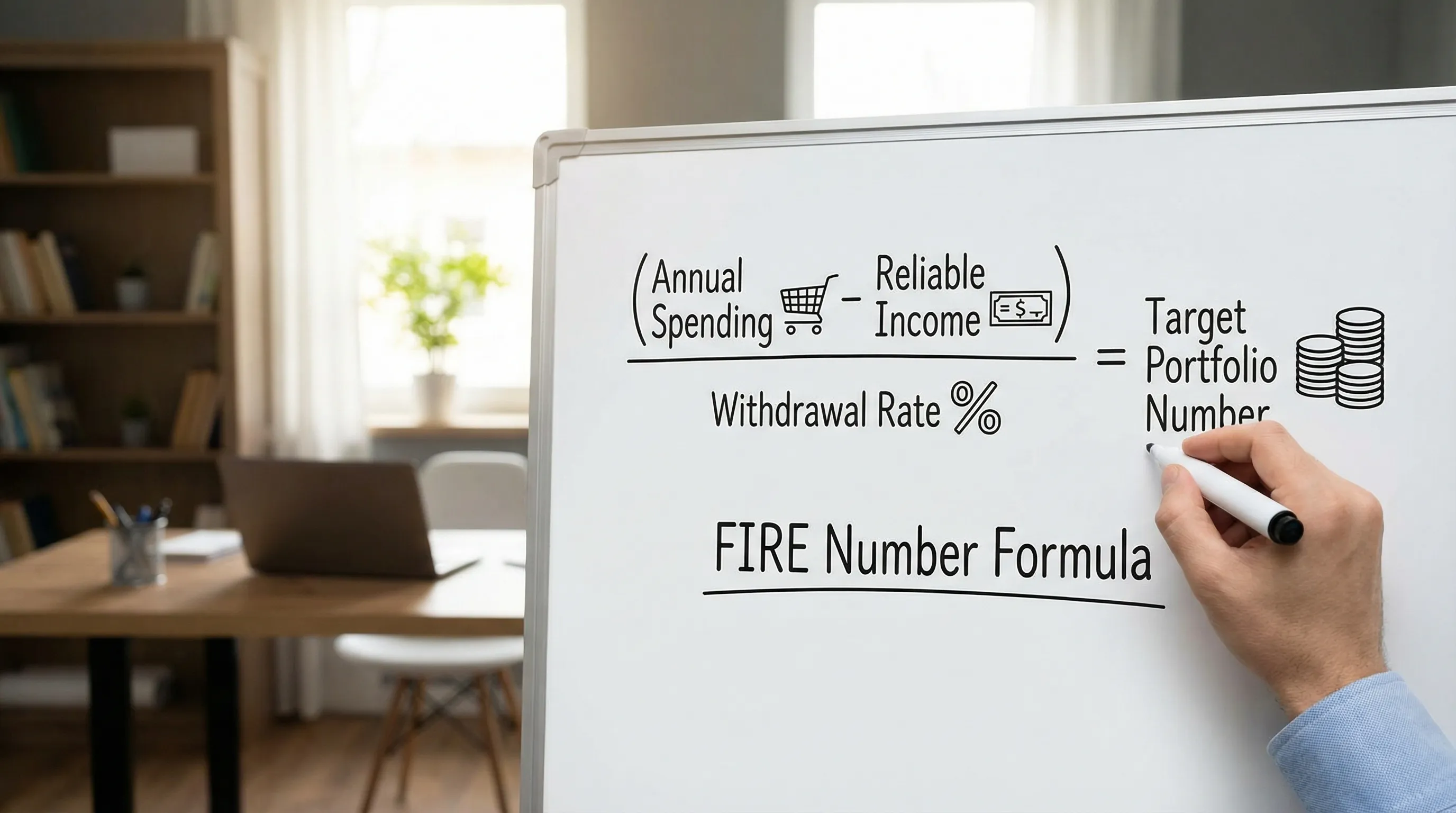

The FIRE number formula (plain English version)

Let’s put the whole thing on one clean line.

The core FIRE number formula

FIRE Number = (Annual retirement spending − Reliable annual income) ÷ Withdrawal rateIn English:

- Annual retirement spending: what you expect to spend each year once work income stops

- Reliable annual income: income you can count on in retirement (pension, Social Security if you’re conservative about it, etc.)

- Withdrawal rate: the percent you plan to withdraw from your portfolio each year

Most people use the 4% rule, which is why you’ll also hear:

The “Rule of 25” shortcut

FIRE Number = Annual spending × 25That “25” is just 1 ÷ 0.04. That’s it. That’s the magic.

If you remember one thing: Your FIRE number is spending, multiplied by a safety factor.

The withdrawal rate cheat sheet (because 4% isn’t a law of physics)

The 4% rule is based on historical U.S. market data and a 30-year retirement horizon, popularized by research from William Bengen (1994) and later discussions like the Trinity Study era. It’s a guideline, not a guarantee.

If you’re aiming for early retirement (40s, 50s), you might choose a lower rate to be safer.

| Withdrawal rate | Multiplier (approx.) | What it implies |

|---|---|---|

| 5% | 20× | Aggressive, less margin for bad markets |

| 4% | 25× | Classic “Rule of 25” baseline |

| 3.5% | 28.6× | More conservative, common for early retirees |

| 3% | 33.3× | Extra conservative for long horizons or high anxiety |

Quotable truth: Lower withdrawal rate = bigger FIRE number, smaller chance of waking up employed again.

A quick story: the “FIRE number” that vanished overnight

Meet Sarah.

Sarah told her friends she was “basically Coast FIRE.” Then she actually pulled her last 12 months of spending.

- The “little” subscriptions added up to real money.

- Travel wasn’t a line item, it was a personality.

- Her grocery budget had the discipline of a toddler in a candy aisle.

Her projected annual spending wasn’t $50,000. It was $72,000.

At 4%, her FIRE number didn’t gently adjust. It teleported.

- $50,000 × 25 = $1.25M

- $72,000 × 25 = $1.8M

Same person. Same job. Different reality.

This is why the formula matters, and why your inputs matter more.

How to calculate your FIRE number without self-delusion

Step 1: Get your real annual spending (not your “best month”)

The cleanest approach is simple:

- Use your last 12 months of spending

- Remove one-time weirdness (a move, medical event, wedding)

- Add predictable “true expenses” you undercount (annual insurance, holiday spending, car repairs)

If you’re using FIYR, this is where it gets dramatically easier because you can:

- Categorize spending cleanly (custom categories and category groups)

- Auto-sort repeat transactions with rules

- Tag one-off events with labels (example: “New York Trip 2025”) so they don’t poison your baseline forever

Reality check: Your FIRE number is only as accurate as your spending data is honest.

Step 2: Convert “current life” spending into “retirement life” spending

Retirement spending is not just today’s spending with “work clothes” removed.

Some things go down (commuting). Some go up (healthcare, time to do things, taxes depending on your setup).

Use this table as a starting brain-jogger:

| Category | Often changes? | Why |

|---|---|---|

| Commuting, parking, lunch out | Down | Work friction disappears |

| Healthcare | Up | Employer coverage may vanish |

| Travel, hobbies, activities | Up | Free time is expensive |

| Taxes | Depends | Withdrawal strategy matters |

| Housing | Depends | Mortgage payoff, downsizing, or moving |

The goal is not precision to the dollar. The goal is not lying to yourself.

One-liner: Retirement is a lifestyle change, not a coupon code.

Step 3: Choose a withdrawal rate that matches your risk tolerance

Here’s the part nobody talks about: your withdrawal rate is partly math and partly psychology.

Ask yourself:

- Are you retiring at 65 or 45?

- Would a 40% market drop make you panic-sell like it’s 2008 and you just discovered fear?

- Do you have flexibility (part-time work, variable spending) or a fixed-cost lifestyle?

If you want a simple rule of thumb:

- 4%: solid baseline for many, especially if you have flexibility

- 3.5%: common for early retirees wanting more margin

- 3%: conservative, often chosen for very long horizons or higher spending rigidity

For a deeper dive, FIYR’s guide on the topic is here: Unlocking the 4% Rule.

Step 4: Subtract reliable retirement income (only the stuff you’d bet your house on)

This is where people get cute and ruin the math.

“Reliable income” can include:

- Pension income

- Conservative Social Security estimates

- Net rental income (after vacancy, maintenance, property taxes)

Not reliable:

- “I’ll just consult a little”

- “My side hustle will totally keep printing money forever”

- “Crypto will bounce back, bro”

If you have reliable income, your formula becomes:

FIRE Number = (Spending − Reliable income) ÷ Withdrawal rateExample:

- Spending: $80,000/year

- Reliable income: $20,000/year

- Withdrawal rate: 4%

Clean. Boring. Powerful.

Worked examples (so you can steal the structure)

Here are three realistic scenarios with the same formula.

| Persona | Annual spending | Reliable income | Withdrawal rate | FIRE number |

|---|---|---|---|---|

| “Regular FIRE” professional | $70,000 | $0 | 4% | $1,750,000 |

| Early retiree, more conservative | $70,000 | $0 | 3.5% | $2,000,000 |

| Pension-backed planner | $90,000 | $30,000 | 4% | $1,500,000 |

What should jump out at you:

- Spending drives everything.

- A small withdrawal-rate change moves the goal by hundreds of thousands.

- Reliable income can shrink the target fast.

Memorable takeaway: Your FIRE number is not about being rich, it’s about being funded.

The two hidden multipliers: taxes and “life happens”

People love the clean 25× math. Markets love chaos.

Two big gotchas:

1) Taxes (yes, even in FIRE)

Depending on whether your money is in pre-tax accounts, Roth accounts, or taxable brokerage, your effective tax rate in retirement can vary wildly.

You don’t need to solve your tax plan today, but you do need to stop pretending taxes are optional.

If you want a simple approach:

- Build your spending number to include taxes (conservatively)

- Or use a slightly lower withdrawal rate to create margin

2) One-time costs and “surprise” expenses

The average adult experience includes:

- Car replacements

- Medical costs

- Family support

- Home repairs

And because modern life is a subscription you can’t cancel, you also get the classics: forgotten renewals, fees, and financial leaks.

Given that only 45% of adults report having an emergency fund (per the same CNBC reporting), lots of people are trying to FIRE without a financial seatbelt.

Practical move: treat “buffer” as a feature, not a failure.

The simple system to keep your FIRE number accurate (without turning into Spreadsheet Guy)

The FIRE number formula is easy.

The hard part is keeping your inputs current while life changes, prices inflate, and your spending categories mutate like Pokémon.

Use this monthly rhythm:

- Review last month’s spending (10 minutes)

- Check your rolling 12-month spending (5 minutes)

- Update any big life changes (new rent, daycare, insurance, debt payoff) (5 minutes)

- Re-run your FIRE number with 4%, 3.5%, and 3% (5 minutes)

This is also where an app like FIYR earns its keep, not by “budgeting harder,” but by making the tracking cleaner:

- Transactions get categorized with rules so you stop babysitting your data

- Subscriptions get tracked so you stop funding apps you forgot existed

- Savings rate and net worth update so your FIRE timeline is based on reality, not hope

If you’re coming from Mint or evaluating modern alternatives, this comparison can help: FIYR vs Mint: Which Budgeting Style Fits You Best in 2026?

One-liner: Your FIRE number isn’t hard, your inputs are messy. Clean inputs, clean future.

Common mistakes that make your FIRE number useless

Using income instead of spending

Your income is what you make. Your FIRE number is about what you consume.

High income with high spending equals a fancy hamster wheel.

Forgetting “true expenses”

Annual bills, car repairs, holidays, insurance premiums. They still count, even if they only show up once a year like a villain in a sequel.

Not separating one-time events from ongoing lifestyle

If you label major trips, moves, and big purchases, you can keep them visible without letting them distort your baseline forever.

Picking a withdrawal rate based on vibes

A withdrawal rate is a risk decision. Treat it like one.

Frequently Asked Questions

What is the fire number formula? The fire number formula is: (annual retirement spending minus reliable annual income) divided by your withdrawal rate. Many people use a 4% withdrawal rate, which is why the shortcut is spending × 25. Why do people multiply by 25 for FIRE? Multiplying by 25 is the “Rule of 25,” based on a 4% withdrawal rate (1 ÷ 0.04 = 25). It estimates the portfolio size needed to fund your annual spending. Should I use 4% or 3.5% for my FIRE number? 4% is a common baseline. 3.5% is more conservative and often used by early retirees or people with less flexibility in spending. The right choice depends on your timeline and risk tolerance. Do I subtract Social Security from my FIRE number? You can subtract Social Security if you use a conservative estimate and you’re confident about the timing. Many people prefer to treat it as a safety buffer instead of a core input. Is my FIRE number the same as my net worth goal? Not necessarily. Your FIRE number is the investable portfolio needed to fund spending. Net worth includes assets that may not produce income (like home equity), unless you plan to tap it. ---Want a FIRE number that’s based on reality (not a guess)?

The formula is simple. The execution is where people faceplant, usually because their spending data is incomplete, messy, or quietly lying to them.

If you want to calculate and track your FIRE number using real inputs, not optimism, use a system that makes the basics automatic: clean transaction categorization, subscription visibility, savings-rate tracking, and a clear view of net worth.

FIYR is built for exactly that, especially if you’re a former Mint user or comparing modern apps like Monarch, Copilot, Rocket Money, or Quicken. Start by reading: How to Calculate FIRE Number (Without Guesswork).

Final one-liner: FIRE isn’t about escaping work, it’s about buying back your time with receipts.