Spending Analysis Sankey Chart: Follow the Money Like a Pro

Most budgets aren’t broken. They’re just… vague.

A pie chart tells you “Dining is 18%.” Cool. That’s like your doctor saying, “You have a body.” Thanks.

A spending analysis sankey chart is different. It shows you the path your money takes, from paycheck to paycheck. Literally. It’s the financial equivalent of following footprints in the snow, except the footprints are labeled “DoorDash,” “Amazon,” and “Annual subscription you forgot existed.”

And in 2026, with one-tap buying and subscription creep thriving like mold in a college fridge, you need more than “here’s a category total.” You need the money story.

Here’s how to read it, build it, and use it to make smarter decisions without turning into a spreadsheet hermit.

What a Sankey chart is (and why it hits different)

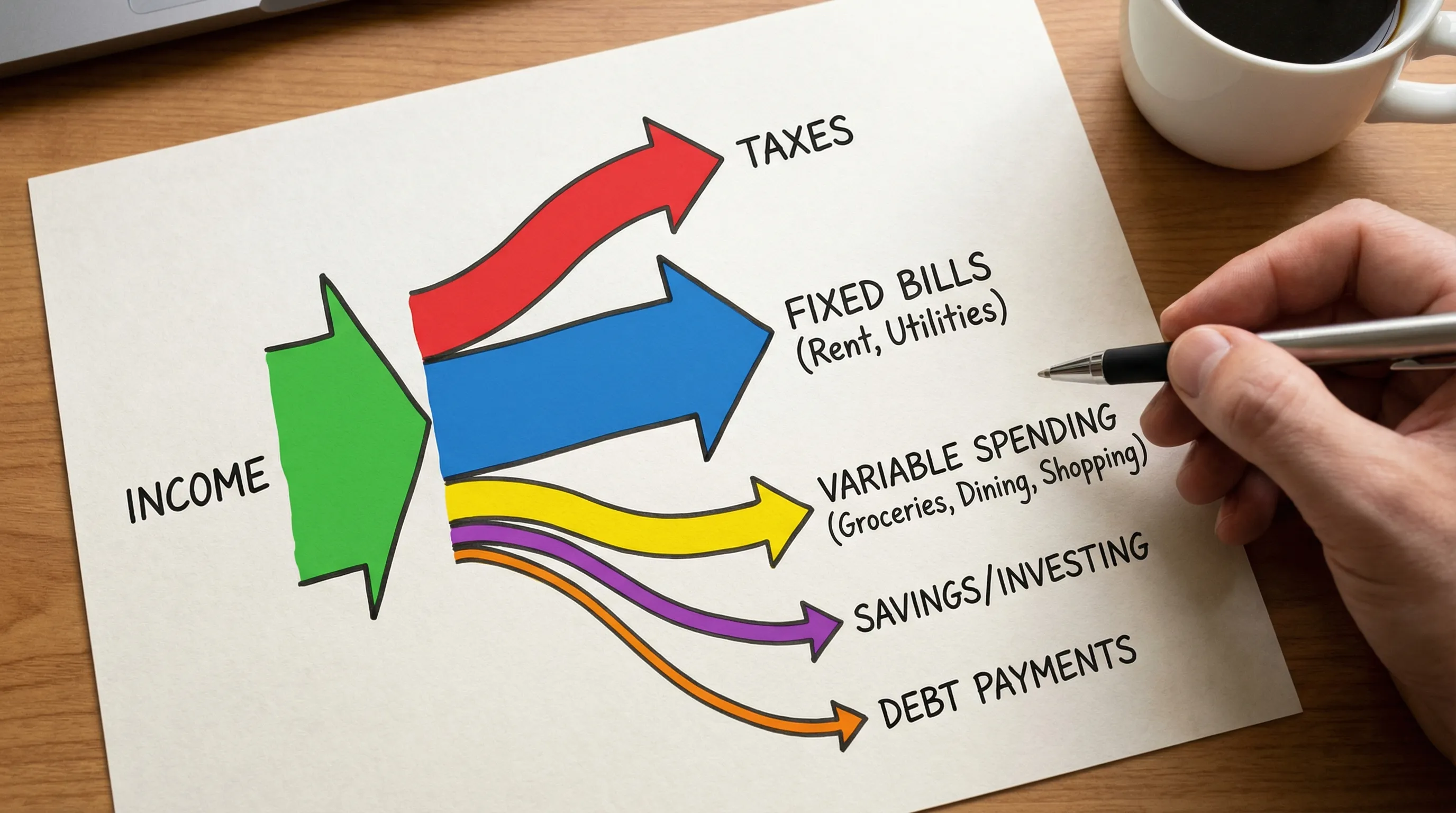

A Sankey chart is a flow diagram where the width of each flow is proportional to the amount of money.

So instead of:

- “Spending by category”

You get:

- Income → Bills → Leftover → Spending choices → Savings (or debt)

It’s not just “what.” It’s “how the heck did we get here?”

If a pie chart is a snapshot, a Sankey chart is the surveillance footage.

Why you should care: most people are stressed, and the numbers are a mess

Money stress is not a niche hobby. It’s mainstream.

CNBC reported that 60% of Americans are living paycheck to paycheck, and financial stress is widespread (including high credit card debt levels). That’s not “some people need to budget better.” That’s “the system is doing parkour on everyone’s face.” (CNBC)

A Sankey chart helps because it does something your brain actually responds to:

- It makes the invisible visible.

- It exposes the “death by a thousand cuts” category.

- It shows tradeoffs (if you increase X, what gets thinner?).

Your budget doesn’t need more guilt. It needs better diagnostics.

The mini-story: “Meet Sarah, who thought she was ‘fine’”

Sarah is a former Mint user. Smart, employed, not reckless. She opens her budgeting app, sees a clean pie chart, and thinks: “Okay, dining is a bit high, but overall I’m fine.”

Then she builds a Sankey.

Her flow looks like this:

- Income → Fixed bills (reasonable)

- Income → Subscriptions (wait, why is that stream thick?)

- Income → “Convenience spending” (why is that stream basically a river?)

The punchline: she wasn’t “bad with money.” She was blind to flow.

Pie charts hide the journey. Sankeys snitch.

Sankey vs. pie vs. bar: use the right weapon

Sankey charts are not “better.” They’re sharper for a specific job.

| Chart type | Best for | What it’s bad at | When to use it |

|---|---|---|---|

| Pie chart | Quick composition snapshot | Tradeoffs, sequences, sources and destinations | “What share is this category?” |

| Bar chart | Comparing category totals over time | Showing where money came from and where it went next | “What’s trending up or down?” |

| Sankey chart | Flow and causality (sources → uses) | Detailed drill-down for dozens of categories | “How does my paycheck get eaten?” |

If you want behavior change, flow beats fractions.

The real power move: make your Sankey chart answer one question

A Sankey can show a million things. Don’t.

Pick one:

- Where does my income go before I even touch it? (taxes, benefits, payroll deductions)

- What portion of take-home becomes fixed commitments? (rent, debt minimums, insurance)

- What part of my “flex spending” is actually autopilot? (subscriptions, convenience food)

- How much of my spending is aligned with my values vs my impulses?

A good Sankey chart is a sniper rifle, not a confetti cannon.

How to build a spending analysis Sankey chart (step-by-step)

You do not need to be a data scientist. You need clean transactions and a plan.

Step 1: Start with clean, consistent transaction data

A Sankey chart is only as honest as your categorization.

Before you build anything, make sure you:

- Fix transfers so they are not counted as spending (common credit card payment mistake)

- Split mixed transactions when needed (hello, Costco)

- Use categories that map to decisions, not vibes

If your categories are chaos, start here: Budgeting categories list.

And if you want your data to stay clean without weekly suffering, rules are your friend: Spending rules automation.

Step 2: Choose your “nodes” (the buckets in your flow)

For a first Sankey, don’t overcomplicate it. Use 2 layers.

Layer 1 (source):- Income (paychecks, client deposits)

- Taxes and payroll

- Fixed bills

- Debt payments

- Variable essentials

- Lifestyle

- Savings and investing

Then, if you want one more layer, break “Lifestyle” into a few subcategories (Dining, Shopping, Travel, Entertainment).

The goal is readability, not a museum exhibit.

Step 3: Aggregate your spending into a simple flow table

A Sankey tool usually needs rows like:

- Source, Target, Value

Example:

| Source | Target | Value |

|---|---|---|

| Income | Fixed bills | 2,400 |

| Income | Variable essentials | 850 |

| Income | Lifestyle | 620 |

| Income | Debt payments | 300 |

| Income | Savings and investing | 1,030 |

If you add a third layer, it becomes:

| Source | Target | Value |

|---|---|---|

| Lifestyle | Dining | 260 |

| Lifestyle | Shopping | 210 |

| Lifestyle | Entertainment | 150 |

Yes, your “Lifestyle → Coffee” stream might be thicker than you expected. That’s the point.

Step 4: Build the chart in a Sankey tool

Here are a few options, depending on your tolerance for fiddling:

- SankeyMATIC for quick-and-dirty charts

- RAWGraphs for flexible, open-source visualization

- Flourish for polished, shareable visuals

- Power BI if you already live in dashboards

You paste your flow table, map columns, and boom: your money has a storyline.

Step 5: Read it like a pro (the “thick stream” rule)

When you look at the Sankey, ignore the tiny streams. Your life isn’t ruined by the occasional $14.99.

Focus on:

- The thickest 3 streams (these are your actual levers)

- Anything surprisingly thick (subscriptions, fees, “misc shopping”)

- Anything that should be thick but isn’t (savings, debt payoff)

Your biggest wins live where the width is.

What patterns to look for (and what to do about them)

Pattern 1: “Fixed bills ate my paycheck”

If Income → Fixed bills is a firehose, you have a structural issue, not a willpower issue.

Moves that actually matter:

- Renegotiate housing (roommates, refi, move, downsize)

- Re-shop insurance

- Fix car costs (the sneakiest wealth-killer in suburbia)

This is also why flexible budgeting beats rigid budgeting, because you need a system that bends without snapping: Flexible budgeting.

Pattern 2: “Lifestyle looks normal… until you split it”

A single “Lifestyle” node can hide a lot of dumb.

Split it once, and you usually find:

- Convenience spending (food delivery, rideshares)

- Shopping creep (small purchases that feel like nothing)

- Social spending (events, weekend trips, gifts)

This is where labels can help you stop arguing with yourself and start measuring reality (example label: “NYC Trip 2025” so it doesn’t pollute your normal month).

Pattern 3: “Subscriptions are a stealth tax”

If the Subscriptions stream is thick, congratulations: you have recurring charges that no longer spark joy.

Run the subscription playbook: Subscription overload solutions.

Your future self does not need seven streaming services. Your future self needs options.

Pattern 4: “Debt payments are thick, but balances barely move”

This usually means interest is eating your effort.

If your Sankey shows a chunky stream to debt, but your net worth isn’t improving, you need an actual payoff strategy, not vibes: Debt payoff strategies.

The 15-minute weekly routine (so your Sankey stays useful)

A Sankey chart is not a one-time art project. It’s a recurring truth serum.

Here’s a simple rhythm:

- Weekly: check the top 3 categories by spend, scan for “what the heck is that?” transactions

- Monthly: rebuild the flow table, regenerate the chart, compare month-over-month thickness

- Quarterly: decide one lever to pull (cut, cap, renegotiate, or automate)

If that sounds like work, remember the alternative is “wondering where your money went” forever. That’s not a plan. That’s a haunted house.

Where FIYR fits (without the cringe sales pitch)

A Sankey chart needs clean inputs.

FIYR helps you keep those inputs sane by making it easier to:

- Track income and expenses consistently

- Use custom categories and category groups so your nodes match your real life

- Create automatic transaction rules so your data stays clean over time

- Track subscriptions and recurring charges so they do not hide in plain sight

- Monitor savings rate and net worth so you can connect spending flow to FIRE progress

And when you’re ready to do deeper visualization work, having accurate categories, rules, and labels makes exporting and mapping flows dramatically easier.

If you want the FIRE tie-in, this is the underrated part: your Sankey chart is basically the pre-work for an honest FIRE number. Clean spending data in, realistic retirement math out. (Related: FIRE number formula explained.)

Frequently Asked Questions

What is a spending analysis sankey chart? A spending analysis sankey chart is a flow diagram that shows where your money comes from and where it goes, with thicker lines representing larger dollar amounts. Why use a Sankey chart for budgeting instead of a pie chart? Pie charts show proportions, but Sankey charts show flow. If you want to understand tradeoffs and how money moves from income to bills, spending, and savings, Sankey is clearer. How do I make a Sankey chart from my bank transactions? Categorize transactions, aggregate totals into a simple source-target-value table, then paste that table into a Sankey tool like SankeyMATIC, RAWGraphs, or Flourish. What categories should I use in my first Sankey chart? Start simple: Income → Taxes/Payroll, Fixed Bills, Variable Essentials, Lifestyle, Debt Payments, Savings/Investing. Add a third layer only if you need it. How often should I update my spending Sankey chart? Monthly is the sweet spot. Weekly is great for catching weird transactions, but monthly gives you enough data for real patterns.Ready to follow the money for real?

If you’ve ever said “I make decent money, so why do I feel broke?” a Sankey chart will answer you. Sometimes gently. Sometimes like a slap.

The winning move is building a system where your data stays clean enough to trust. That’s where FIYR shines: flexible categories, automation rules, subscription tracking, and FIRE-focused metrics that keep you honest without making budgeting your second job.

If you want to stop guessing and start steering, head over to FIYR and start with a clean month of tracking. Your money already has a story. You might as well read it.