Savings Rate for FIRE: The Fastest Path to Freedom

Most people think FIRE is an investment problem.

It’s not.

It’s a behavior + math problem, disguised as “Should I buy VTI or VOO?” so we can avoid the real villain: your savings rate.

Because here’s the uncomfortable truth: you can’t out-invest a life that eats your paycheck like it’s an all-you-can-eat buffet.

And the buffet is crowded. A CNBC report cites survey data showing about 60% of Americans are living paycheck to paycheck, and financial stress is basically the national hobby. The FIRE crowd isn’t immune, they just track their chaos in prettier spreadsheets.

The savings rate for FIRE is the cheat code (because it hits twice)

Meet Sarah.

Sarah makes $110,000, has a solid job, and tells people she saves “around 25%.” She also has six subscriptions she forgot about, a car payment that feels like a second rent, and a grocery bill that suggests she’s feeding a youth soccer league.

When she finally does the math (with real transactions, not vibes), her actual savings rate is 11%.

Then she makes three changes:

- Cancels the forgotten subscriptions.

- Drops one “nice-to-have” fixed cost.

- Auto-invests the difference the day after payday.

Her savings rate climbs to 25% for real, and suddenly FIRE stops being a fantasy and starts being a date on a calendar.

That’s why the savings rate for FIRE is the fastest path to freedom: it simultaneously shrinks the life you need to fund and boosts the money you invest.

Quotable truth: Your savings rate is the speedometer. Everything else is interior design.

What “savings rate” actually means (and why people argue about it)

Savings rate sounds simple until you try to calculate it and your bank feed looks like a toddler scribbled it.

There are two common definitions. Both are useful, as long as you don’t mix them and accidentally congratulate yourself for paying your credit card bill.

| Version | Formula (plain English) | Best for | Watch-outs |

|---|---|---|---|

| Cash-flow savings rate | (Take-home pay minus spending) / take-home pay | Day-to-day budgeting and lifestyle control | Easy to inflate if transfers get miscategorized |

| FIRE savings rate | Long-term savings / gross income | Retirement timeline math and FIRE planning | Requires consistency about what counts as “savings” |

If you want a clean walkthrough, FIYR has a deeper explainer here: Savings Rate Calculator: The One Metric That Matters.

The math: why a higher savings rate nukes your timeline

FIRE is basically two numbers:

- Your annual spending (what your life costs)

- Your FI number (commonly spending × 25, based on the 4% rule)

When your savings rate goes up, you win twice:

- Your spending goes down (or grows slower), so your FI number gets smaller.

- Your investing goes up, so you reach that smaller number faster.

This is why high earners who spend like they’re in a rap video can be “broke,” while normal earners with a strong savings rate quietly hit freedom.

Savings rate to FIRE timeline (rule-of-thumb table)

Below is a simplified timeline estimate assuming:

- You start from $0 invested (life is unfair, but math likes clean starts).

- You earn a 5% real return (after inflation).

- You target 25× annual expenses (the classic 4% rule framing).

These are approximations, not a blood oath.

| Savings rate | Approx. years to FI | What it feels like in real life |

|---|---|---|

| 10% | 51 years | “Normal retirement, maybe, if life behaves.” |

| 20% | 37 years | “Better, but still a long grind.” |

| 30% | 28 years | “Now we’re talking.” |

| 40% | 22 years | “You have options.” |

| 50% | 17 years | “This is the FIRE on-ramp.” |

| 60% | 12 years | “You’re basically speedrunning adulthood.” |

| 70% | 9 years | “Are you okay? Do you eat?” |

This concept is famously popularized by Mr. Money Mustache (the patron saint of bike commuting and financial side-eye).

Quotable truth: In FIRE math, 10% more savings rate is not 10% better, it’s often years better.

What counts as “savings” for FIRE (and what’s just money cosplay)

For FIRE, “savings” usually means money that increases your net worth long-term. The cleanest categories:

- Contributions to retirement accounts (401(k), IRA, etc.)

- Brokerage investing

- HSA contributions (if invested and used strategically)

- Extra principal payments on high-interest debt (especially credit cards)

Gray area (still legit, but define it consistently):

- Extra mortgage principal (building home equity is real, but less liquid)

- Cash savings beyond your emergency fund target (useful, but too much cash can drag returns)

Not savings:

- Credit card payments (that’s just settling last month’s decisions)

- Transfers between accounts

- Reimbursements (unless you also include the expense)

If you’ve ever thought, “I saved $1,200 this month,” and what you really did was move $600 from checking to savings twice, welcome to the club.

Step 1: Calculate your savings rate for FIRE (without lying to yourself)

If you want one clean method that works for W-2 employees, freelancers, and “my income is a rollercoaster” people, do this:

Use the last 12 months, not last Tuesday

Monthly data is noisy. The last 12 months gives you reality.

- Add up gross income (paychecks, side income, bonuses).

- Add up long-term savings (investments, retirement contributions, debt payoff above minimums).

- Divide savings by gross income.

Then calculate your “spending floor” too: housing, utilities, insurance, minimum debt payments, groceries, transportation. This is the number that decides whether you’re doing Lean FIRE, Regular FIRE, or “Fat FIRE but I still pack snacks onto flights.”

If you want the FIRE number side of this, read: How to Calculate FIRE Number (Without Guesswork).

Step 2: Stop losing to invisible spending (subscriptions, fees, and tiny betrayals)

Here’s the part nobody talks about: your savings rate usually isn’t being destroyed by one big mistake.

It’s being mugged by a gang of small ones.

- Subscriptions you forgot about

- “Free trials” that became permanent roommates

- Delivery fees that cost more than your actual willpower

- Bank and card fees that feel like a tax for being busy

If you need a tactical reset, FIYR’s subscription workflow is covered here: Best Apps to Manage Subscription Renewals.

Quotable truth: A budget doesn’t fail, it gets quietly pickpocketed.

Step 3: The Big 3 levers that move your savings rate fastest

You can “latte factor” yourself into exhaustion, or you can hit the big levers like an adult.

Lever 1: Housing (the final boss)

Housing is usually the largest line item, which means it’s the easiest place to buy years of freedom.

Ideas that actually move the needle:

- Refinance or renegotiate at renewal (when applicable)

- Get roommates (yes, even as a grown-up, especially short-term)

- House hack (rent a room, ADU, or duplex strategy)

- Move one notch down the prestige ladder (zip codes do not love you back)

Lever 2: Transportation (the “I deserve it” trap)

Cars are sneaky because they’re not one expense. They’re an ecosystem:

- Payment

- Insurance

- Maintenance

- Gas

- Parking

- Depreciation (the silent killer)

If your car costs $700/month all-in, that’s $8,400/year.

At a 4% withdrawal lens, that single line item can add roughly $210,000 to your FI number (8,400 × 25). That’s not “just a car.” That’s “a car that delays your freedom.”

Lever 3: Income (the underrated accelerator)

Yes, spending control matters. But once you’ve stopped the bleeding, income growth is rocket fuel.

A simple rule: don’t let raises turn into lifestyle creep.

If you want a structured approach, this pairs well with: How to Avoid Lifestyle Creep in 2026 (And Start Saving More).

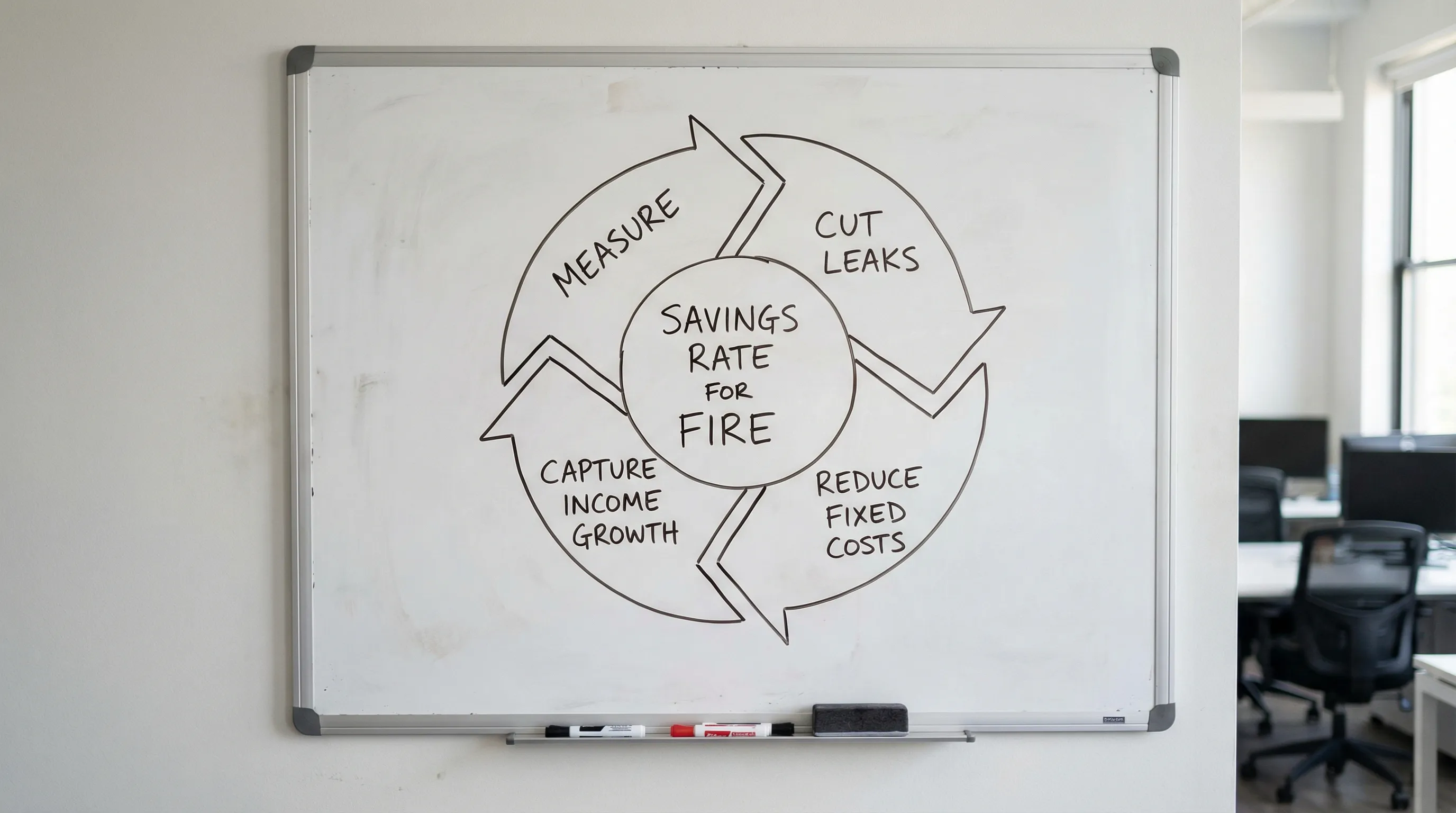

A repeatable system: the “Savings Rate Flywheel”

This is the system you can run every month without becoming a spreadsheet goblin.

1) Measure (real numbers, not vibes)

2) Cut leaks (subscriptions, fees, impulse buys)

3) Reduce fixed costs (housing, transportation, insurance)

4) Capture income growth (raises, side gigs, tax optimization)

Quotable truth: Willpower is not a plan. Systems are.

The 14-day sprint to raise your savings rate (without becoming a monk)

Do this once, then maintain it with a short weekly check-in.

| Day range | What you do | Outcome |

|---|---|---|

| Days 1 to 3 | Pull last 90 days of transactions. Categorize them into 10 to 15 buckets. | You stop guessing where your money goes. |

| Days 4 to 6 | Subscription audit: cancel, downgrade, or annualize (only if you truly use it). | Instant monthly savings, zero lifestyle pain. |

| Days 7 to 10 | Attack one fixed cost: housing, car, insurance, phone, or internet. | Big savings that compound every month. |

| Days 11 to 14 | Automate: paycheck split, auto-invest, and a “safe-to-spend” guardrail. | Your savings rate rises without daily decisions. |

If you want a habit rhythm that sticks, borrow the cadence from FIYR’s “weekly check-in” style posts like Why You’re Overspending (And the One Habit That Could Save You $50,000).

Where FIYR fits (especially if you’re done with Mint-era chaos)

A higher savings rate is mostly a data problem:

- Are transactions categorized correctly?

- Are transfers messing up your numbers?

- Do you know your real “safe-to-spend,” or are you playing financial roulette?

- Are subscriptions visible, or hiding like raccoons in the attic?

FIYR is built for people who want modern tracking without the legacy-app headache:

- Track income, expenses, and net worth in one place

- Use custom categories and category groups (so your budget matches your life)

- Set automatic transaction rules (so your data stays clean)

- Track subscriptions and recurring charges

- See your savings rate and connect it to a FIRE date calculator

If you’re comparing tools, this is a good starting point: Best Mint Replacement App for 2025 and FIYR vs Mint: Which Budgeting Style Fits You Best in 2026?.

The biggest mistake people make with savings rate for FIRE

They treat it like a moral score.

Your savings rate is not a measure of your worth. It’s a measure of your current strategy.

A new parent with childcare costs may be doing everything right at 15%.

A high earner with no dependents “stuck” at 25% is probably leaking money through lifestyle defaults.

The goal is not to win the FIRE Olympics.

The goal is to buy back your time.

Quotable truth: FIRE isn’t about never spending. It’s about spending on purpose.

Frequently Asked Questions

What is a good savings rate for FIRE? A common FIRE-oriented target is 35%+, because it meaningfully compresses the timeline. That said, the “good” number is the one you can sustain while still living like a human. Is savings rate more important than income for FIRE? Savings rate is usually the better first lever because it reduces spending and increases investing at the same time. Income becomes more powerful after you’ve stopped major spending leaks. Should I calculate savings rate using gross or net income? For FIRE planning, gross income is often cleaner and more consistent (especially when retirement contributions come out pre-tax). For budgeting behavior, net (take-home) can be more intuitive. Just pick one and stick with it. Do retirement contributions count toward savings rate for FIRE? Yes, typically. 401(k) contributions, IRA contributions, and employer matches are generally counted as long-term savings in a FIRE-style savings rate. Does paying off debt count as saving for FIRE? Paying above the minimum on high-interest debt is usually treated as a form of saving because it improves net worth and reduces future drag. Credit card payoff is especially high impact. How can I raise my savings rate without feeling deprived? Start with “low-pain” wins (subscription cleanup, fee elimination, impulse friction), then target one major fixed cost. Deprivation fails. Systems stick.The takeaway (and your next move)

If you’re serious about FIRE, stop obsessing over the perfect investment pick and start obsessing over the metric that actually moves the finish line.

Measure your savings rate. Clean up the leaks. Hit one fixed cost. Automate the rest.

If you want the easiest way to keep this all straight, with clean categories, rules that prevent messy data, subscription tracking, and FIRE-focused insights, start here: FIYR’s blog.

Because freedom isn’t complicated.

It’s just rarely tracked. And almost never automated.