FIYR Net Worth Tracker: How to Set It Up for Accuracy

If your net worth number is wrong, everything downstream is wrong too: your savings rate, your FIRE date, your “can we afford this?” confidence, and your ability to sleep like a normal mammal.

And in 2026, that matters more than ever. When 60% of Americans are still living paycheck to paycheck, “close enough” finances are how people accidentally end up financing groceries at 24% APR.

Meet Alex. Solid job, decent income, maxing the 401(k) match. Alex also had a net worth tracker that looked like a crypto chart (random spikes, sudden drops, mostly vibes). The culprit was not “bad with money.” It was the setup: missing liabilities, double-counted transfers, and a house value last updated when sourdough starter was a personality.

This guide is how to set up the FIYR net worth tracker so your number is boring, stable, and trustworthy. Because the goal is not a sexy chart. The goal is decisions that don’t ruin your next decade.

What “accurate net worth” actually means (and what it doesn’t)

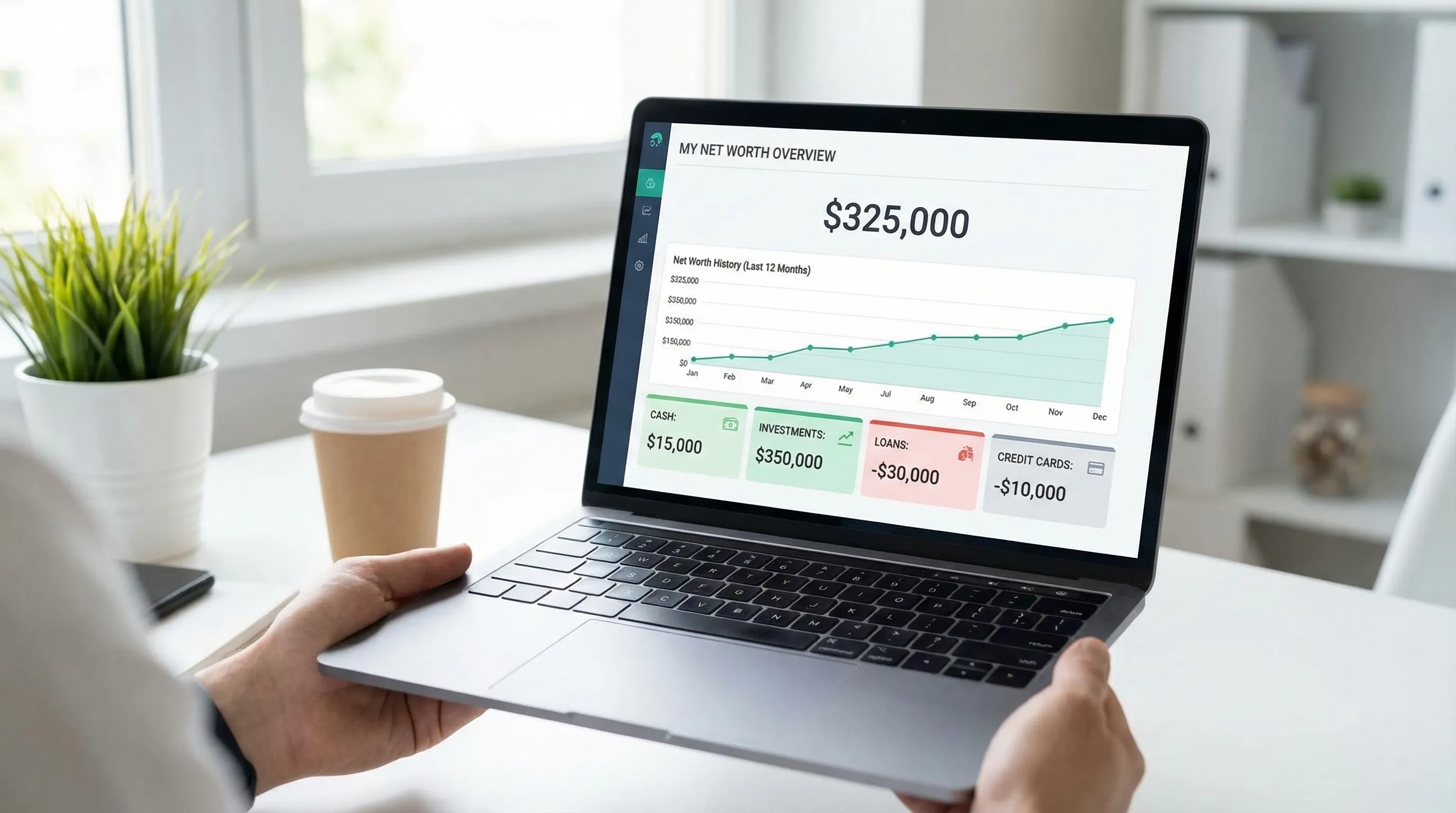

Net worth is simple:

Net worth = assets − liabilitiesAccuracy, though, is a standard. Here’s a practical one that works in real life:

- Directionally correct month to month (you can trust the trend)

- Complete enough to make decisions (no giant blind spots)

- Consistent (same rules every month)

It does not mean “perfect to the dollar every day.” If you’re trying to get net worth precision like a NASA launch, congratulations, you just invented a new hobby called “financial anxiety.”

Your tracker should feel like a bathroom scale: not perfect, but honest. And if it’s honest, it changes behavior.

The 5 ways net worth trackers lie (so you can stop believing them)

Most net worth numbers go off the rails for one of these reasons:

1) Missing liabilities (the classic “optimism tax”)

Mortgage not included. Student loans ignored. Credit cards “because I pay them off.” BNPL lurking like a raccoon in the trash.

If you don’t track liabilities, you’re not tracking net worth, you’re tracking a mood.

For a deeper dive on the liability side, this pairs well with How to Track Liabilities Accurately Without Missing Details.

2) Double counting transfers (the silent killer)

Money moves from checking to savings and suddenly your “income” rises. Or you pay a credit card and your “spending” explodes. Transfers should be treated as… transfers.

3) Stale asset values (hello, 2021 Zestimate)

If your home value hasn’t been updated since your pandemic houseplant phase, your chart is basically historical fiction.

4) Ghost accounts and duplicates

Old brokerages, closed cards, duplicate connections. Your net worth looks bigger because you’re counting a corpse.

5) Mixing “liquid money” with “life is complicated” money

Retirement accounts, home equity, and your emergency fund are all wealth, but they behave differently. If you treat them the same, you’ll make dumb decisions faster.

Net worth is one number. Good net worth tracking is a system.

The FIYR accuracy setup: do this once, benefit forever

This is the setup flow I’d use if I wanted a net worth number I could bet my sanity on.

Step 1: Pick your net worth rules (so you don’t argue with yourself every month)

Before you add anything, decide two things:

- What counts as an asset? (Cash, investments, home, car, HSA, etc.)

- What counts as a liability? (Cards, loans, mortgage, taxes due, etc.)

Your rules do not need to match your friend’s rules. Your rules need to match reality and stay consistent.

If you want a quick refresher on the basics (with examples), keep How to Calculate Net Worth: A Simple Guide With Examples bookmarked.

Quotable truth: Consistency beats perfection, and perfection is usually procrastination.Step 2: Add your “core accounts” first (the stuff that actually moves the needle)

Start with the accounts that explain 90% of your financial life:

- Checking and savings

- Credit cards

- Loans (student loans, auto loans)

- Mortgage (if you have one)

- Retirement accounts (401(k), IRA)

- Brokerage accounts

In FIYR, the goal is a complete view of assets + liabilities so your net worth isn’t missing a limb.

Here’s the part nobody talks about: the first net worth snapshot is allowed to be ugly. Your job is to make it accurate, then make it effortless.

Step 3: Build a “net worth map” (so nothing gets forgotten)

Once core accounts are in, sweep for the common “oops” items people forget.

This table gives you a clean, accuracy-first map.

| Item type | Examples | Where people mess it up | Accuracy rule that works |

|---|---|---|---|

| Cash | checking, savings, HYSA | counting transfers as income | cash balances should match statements |

| Investments | brokerage, 401(k), IRA, HSA invested | duplicating the same account or missing old rollovers | one account, one balance, no duplicates |

| Property | home value | stale estimates | update periodically, not daily |

| Vehicles | car value | fantasy pricing | use a conservative estimate and update occasionally |

| Credit cards | all cards, even “paid off” | ignoring cards because they’re paid monthly | include the current balance at all times |

| Loans | student, auto, personal | missing a loan because autopay exists | autopay is not a tracking system |

| BNPL | Klarna, Afterpay style plans | treating it like “not real debt” | if you owe it, it’s a liability |

If you want an even bigger list of weird but real assets, read Hidden Assets Most People Forget to Track (And Why They Matter).

Step 4: Stop double counting with a “transfer truth” rule

Most net worth chaos is not spending too much. It’s mislabeling money movement.

Use this mental model:

- Spending is money leaving your world.

- Income is money entering your world.

- Transfers are money moving within your world.

If you’re coming from Mint or a spreadsheet, this is where your graphs usually go from “helpful” to “haunted.”

FIYR supports customizable categories and automatic transaction rules, which is how you keep transfers clean over time (instead of re-fixing the same mess every month).

For the full automation mindset, see Spending Rules Automation: Categorize Faster and Never Miss a Transaction.

One-liner: A transfer miscategorized is just financial fan fiction.Step 5: Use categories and labels like a grown-up (context beats clutter)

Accuracy is not just “correct balances.” It’s also understanding what changed.

This is where FIYR’s customization shines: you can keep categories stable and use labels for context.

Examples that make net worth tracking more useful:

- Label a one-time expense that hit cash hard: “New York Trip 2025”

- Label a home project that increased value (or at least your happiness): “Kitchen Reno”

- Label a job change lump sum: “Severance” or “Signing Bonus”

Your net worth chart won’t just move, it’ll make sense.

If your categories are messy, fix that first (it’s the foundation for clean reports): Budgeting Categories List: A Clean Setup That Works.

Step 6: Set an update cadence by asset type (accuracy without obsession)

Not everything needs the same refresh rate. Updating your car value weekly is a cry for help.

Use a cadence that matches how the asset behaves.

| Asset or liability | Suggested update cadence | Why |

|---|---|---|

| Checking/savings | daily to weekly | balances change constantly |

| Credit cards | daily to weekly | prevents “surprise” debt drift |

| Investments | weekly to monthly | markets move, but you’re not day trading your retirement (hopefully) |

| Loans (student/auto) | monthly | payment cycles are monthly |

| Mortgage balance | monthly | same logic as loans |

| Home value estimate | quarterly to semiannually | values change, but not with your mood |

| Vehicles | semiannually to annually | depreciation is slow and predictable |

This is how you stay accurate without turning personal finance into your entire personality.

Step 7: Do a monthly “net worth close” (10 minutes, one coffee)

The secret to accurate tracking is not setting it up once. It’s closing the month like a calm accountant, not a panicked raccoon.

Here’s a simple monthly close you can repeat.

- Confirm cash balances roughly match reality.

- Scan for duplicate accounts or weird spikes.

- Confirm credit card balances and any new loans.

- Update any manual values you track (property, vehicle, other assets).

- Spot-check a few large transactions that might be miscategorized.

- Note what moved your net worth this month (income, spending, market, debt payoff).

If you want your net worth to actually improve, pair this with savings rate tracking. FIYR includes a savings rate calculator and FIRE-focused insights so you can connect daily behavior to long-term freedom.

Related reading: Savings Rate Calculator: The One Metric That Matters.

Truth bomb: What gets reviewed monthly gets better. What gets “checked someday” gets expensive.The “Accuracy Checklist” (print this mentally, tattoo it spiritually)

If your FIYR setup hits these, you’re in the top tier of people who actually know their money.

- You track all major assets and all major liabilities.

- Transfers are not counted as spending or income.

- Credit card payments are not double-counted.

- Big weird stuff (BNPL, old accounts, hidden assets) is accounted for.

- Manual values have an update cadence.

- You do a monthly close.

And then things get interesting: once the number is accurate, it becomes motivating. Net worth stops being a scoreboard you avoid and becomes a game you can win.

How to use net worth once it’s accurate (so it’s not just financial trivia)

An accurate net worth tracker is not a vanity metric. It’s a decision engine.

Here are three practical ways to use it:

Use it to catch “Debt Drift” early

If liabilities creep up while income stays flat, your future self is getting mugged quietly.

(And yes, people really do feel it. CNBC reports 70% of Americans are stressed about finances, and debt drift is a major contributor to that ambient panic.)

Use it to separate “wealth building” from “wealth cosplay”

If your net worth is rising only because you’re under-withholding taxes or floating expenses on a card, that’s not wealth. That’s a magic trick with a bill at the end.

Use it to make FIRE math real

FIYR has a FIRE date calculator based on real user data, which is exactly what you want when you’re sick of guessing.

Net worth is the raw material. Savings rate is the speed. FIRE projections translate the whole thing into: “When can I stop doing this Zoom call forever?”

Common setup mistakes (and the simple fixes)

| Mistake | What it looks like | Fix |

|---|---|---|

| Missing a credit card | net worth looks higher than it feels | add every card, even “rarely used” |

| Counting transfers as spending | budgets look blown up for no reason | treat transfers as transfers, use rules |

| Tracking home value daily | net worth swings wildly | update quarterly or semiannually |

| Too many categories | you stop maintaining it | simplify categories, use labels for context |

| Never reconciling | chart slowly becomes fiction | do a monthly close, 10 minutes |

If you need a broader “clean data” reset mindset, Error-Proof Budgeting: How FIYR Keeps Spending Categories Clean is the companion piece.

Frequently Asked Questions

How often should I check my net worth in FIYR? Weekly is fine for curiosity, monthly is where the value is. A monthly close (balances, duplicates, manual updates) keeps your number honest without obsession. Should I include my home in my net worth? If you want a full balance sheet, yes. Just update it on a sensible cadence (quarterly to semiannually) and don’t treat home equity like spendable cash. Do I include my car as an asset? You can, especially if it’s meaningful relative to your finances. Use a conservative estimate and update once or twice a year so your net worth doesn’t turn into used-car market theater. Why does my net worth drop even when I’m saving? Investments can fall in the short term, large annual bills can hit cash, or you might be finally tracking liabilities you used to ignore. Accuracy sometimes feels worse before it feels empowering. What’s the fastest way to improve net worth once tracking is accurate? Usually: reduce high-interest debt, cut recurring leaks (subscriptions), and raise savings rate. The fastest win is often stopping money from leaving silently.Build a net worth number you can trust (and actually use)

If you’re done with vague charts and “I think we’re fine” energy, set up FIYR like an accuracy-first tracker: full assets and liabilities, clean transfers, smart categories, and a monthly close.

Want the broader system that makes this stick? Start with FIYR Budgeting Tutorial: Your First Week Setup, Step by Step, then bring it home with net worth and savings rate tracking.

Because the point of tracking isn’t to admire your data. It’s to stop your money from freelancing.