How to Track Liabilities Accurately Without Missing Details

Your net worth is a scoreboard. Liabilities are the points your opponent scored while you were busy high-fiving yourself for having a savings account.

Most people think they’re tracking debt because they know they “have a car payment.” Cute. The problem is the details: the forgotten promo APR, the HELOC you used for “renovations” (translation: Home Depot therapy), the Buy Now Pay Later plan quietly nibbling your future.

And it’s not a niche problem. A CNBC report cited that roughly 60% of Americans are living paycheck to paycheck, and 3 in 5 are in credit card debt (average balance $5,875). If your liabilities are fuzzy, your plan is fiction.

Let’s fix that.

What “tracking liabilities” actually means (not the vibes version)

Tracking liabilities accurately means you can answer, instantly, without sweating:

- What do I owe (right now)? Not “around $12k,” not “whatever the app says.”

- What does it cost me (APR and fees)? Debt has rent.

- What am I required to pay (minimum and due date)? Cash flow kills dreams faster than bad investing.

- What type of debt is it (revolving vs installment)? This changes payoff strategy and risk.

- Is it included in my net worth and updated consistently? If you “forget” a liability, your net worth is doing performance art.

Quotable truth: A budget can survive denial. Net worth cannot.

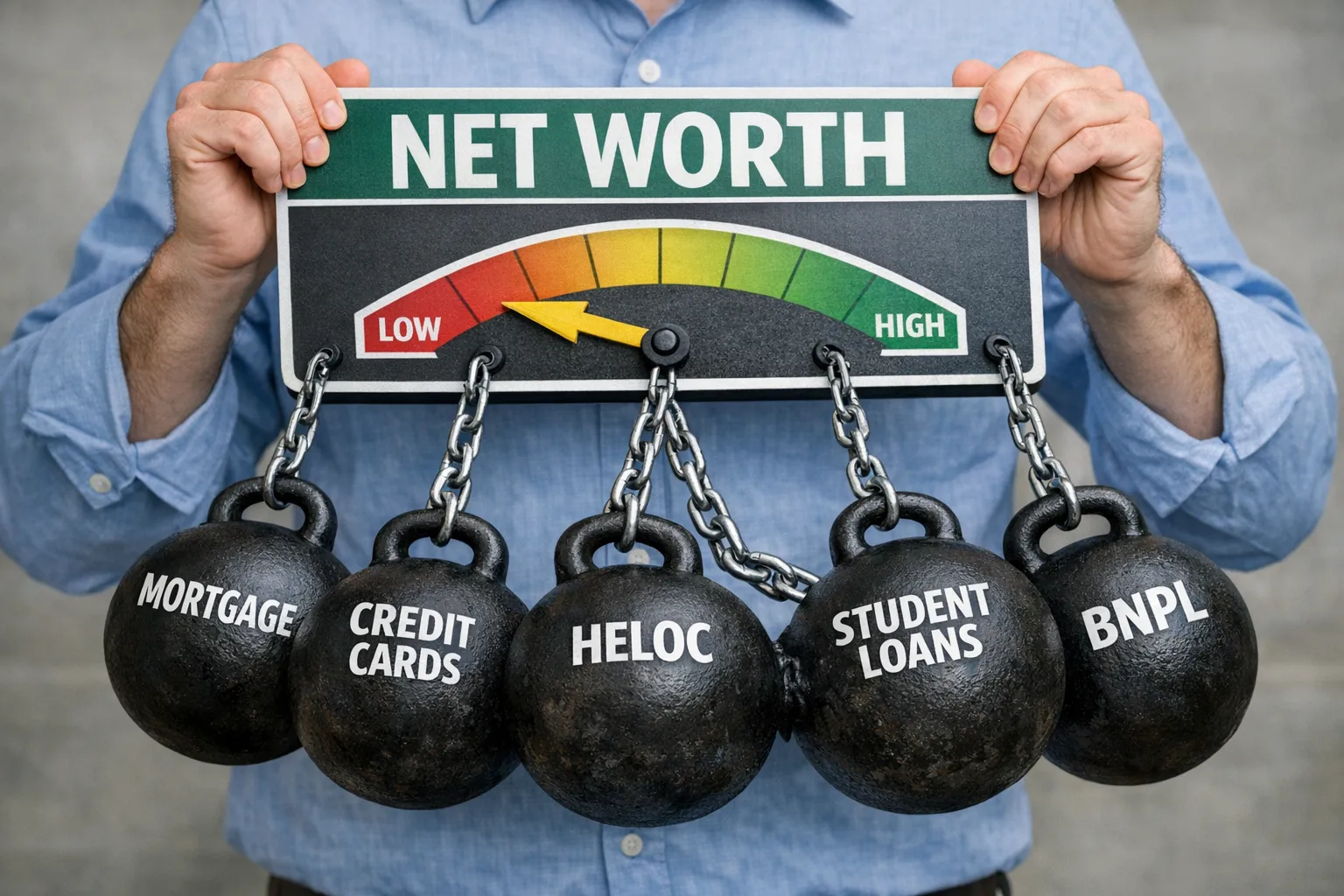

The main liability types you must track (and where they hide)

You’re not just tracking “debt.” You’re tracking contracts you signed while optimistic.

1) Mortgages (and HELOCs)

A mortgage is the big, respectable liability. Everyone remembers it. The mistakes happen in the details.

Track:

- Current principal balance (not original loan amount)

- Interest rate and whether it’s fixed or adjustable

- Next payment due date

- Escrow portion (if applicable) and whether it changes annually

HELOCs are mortgage-adjacent chaos. They act like a credit card with a house as collateral. Track:

- Current balance

- Interest rate (often variable)

- Draw period vs repayment period

One-liner: A HELOC is just a credit card wearing a blazer.

2) Installment loans (auto, student, personal loans)

Installment debt is structured, predictable, and still capable of ruining your mood.

Track:

- Current balance

- APR

- Minimum payment

- Payoff date (or remaining term)

- Servicer (because loans love getting sold like baseball cards)

Student loans deserve extra attention if you have multiple groups, changing rates, or forgiveness programs. Your “one loan” might actually be eight loans in a trench coat.

3) Revolving credit lines (credit cards, personal lines of credit)

These are the liabilities that breed when the lighting is dim and Apple Pay is enabled.

Track:

- Current balance (today), not last statement

- APRs by category if applicable (purchases, cash advances, promo)

- Minimum payment and due date

- Credit limit (because utilization matters)

If you carry balances, the difference between statement balance and current balance is not trivia. It’s the difference between control and confusion.

4) BNPL (Buy Now Pay Later) and “micro-debt”

BNPL is how you end up making monthly payments on socks. Financially, it’s an installment plan. Psychologically, it’s a magic trick.

Track:

- Remaining balance

- Payment schedule (weekly, biweekly, monthly)

- Linked funding source (card or bank)

- Late fee rules and “deferred interest” terms if any

BNPL often slips through because it’s split across apps, merchants, and cards. You feel fine until four “small” payments land in the same week.

One-liner: BNPL is debt with a marketing degree.

Why liabilities change your net worth (and your FIRE timeline)

Net worth is:

Net worth = Assets − LiabilitiesSo every dollar of debt is a direct subtraction. No drama. No debate.

But liabilities also hit you twice:

- They reduce your net worth today.

- They reduce your future investing power because payments eat cash flow.

A quick example (small numbers, big truth)

Let’s say you have:

- Assets: $95,000 (cash, 401(k), car value, etc.)

- Liabilities you remember: $20,000 (student loan)

You think your net worth is $75,000.

Now add the liabilities you “forgot”:

- Credit card: $4,200

- BNPL: $900

- Personal loan: $3,400

Actual liabilities: $28,500.

Actual net worth: $66,500.

That’s an $8,500 gap created by forgetting a handful of debts. You didn’t get poorer, you just stopped lying to yourself.

Quotable truth: You can’t out-invest math you refuse to measure.

The right way to track liabilities (the system that doesn’t crumble in month two)

Here’s the part nobody talks about: tracking debt isn’t hard, it’s annoying. The winning strategy is building a system that survives your laziness.

Step 1: Define your “source of truth” and update rhythm

Pick one place where liabilities live. One.

- Monthly update is enough for most people.

- Weekly update helps if you’re paying down revolving balances aggressively or juggling BNPL payments.

If you’re using an app, the goal is fewer manual updates, fewer mistakes.

Step 2: Track the 7 fields that prevent “oops” moments

For every liability, record:

- Type (mortgage, installment, revolving, BNPL)

- Current balance

- APR (or rate range if variable)

- Minimum payment

- Due date

- Autopay status (yes/no and from which account)

- Notes (promo ends, deferment ends, repayment phase changes)

Those last two fields are where accuracy lives.

Step 3: Separate net worth tracking from cash flow tracking

This is where people faceplant.

- Net worth is a snapshot of balances.

- Cash flow is what moved this month.

Debt payments affect both, but differently:

- Principal payments reduce the liability balance (net worth improves).

- Interest payments are an expense (cash flow worsens).

If you want clean budgets, treat debt payments properly in your tracker. For credit cards specifically, many people avoid double-counting by treating card payments like transfers rather than “spending.” (If you want the full workflow, see FIYR’s guide on budgeting with credit cards.)

One-liner: Debt is a balance-sheet problem that disguises itself as a monthly payment.

Step 4: Stop letting “estimated” balances live forever

If you don’t have exact balances, fine. Start with estimates today, then replace them with real numbers in your first review.

A good rule: No estimate survives past 30 days.

Step 5: Reconcile like an adult (10 minutes, once a month)

Once a month:

- Check each liability balance against the lender/app

- Confirm minimum payment and due date (lenders love changing portals and terms)

- Update notes for any promo APR end dates or repayment phase shifts

This is boring. It also prevents expensive mistakes. Welcome to personal finance.

Liabilities checklist (a quick sweep that catches the sneaky stuff)

Use this list to do a “liability audit.” If you hesitate, you probably have it.

- Mortgage(s)

- HELOC(s)

- Auto loan(s)

- Student loan(s) (including multiple loan groups)

- Personal loan(s)

- Credit cards (including store cards)

- Personal line of credit

- Business debt (business cards, SBA loans, equipment financing)

- Medical payment plans

- IRS or state tax payment plans

- Childcare or tuition payment plans

- 401(k) loan (yes, you owe yourself, still a liability)

- Margin loan (brokerage borrowing)

- BNPL plans (Affirm, Klarna, Afterpay, PayPal Pay in 4, merchant plans)

- “I owe a friend” debt (if it’s real, track it)

Quotable truth: If it has a payment schedule, it deserves a row in your tracker.

Example liability tracking table (copy this and pretend you invented it)

Below is a clean format that works in a spreadsheet or inside a net worth tracker. Numbers are examples.

| Liability | Type | Current balance | APR | Minimum payment | Due date | Autopay | Notes |

|---|---|---|---|---|---|---|---|

| Primary mortgage | Mortgage | $312,450 | 6.25% | $2,150 | 1st | Yes | Escrow increases annually |

| HELOC | Revolving (secured) | $18,900 | Variable (Prime + margin) | Interest-only | 15th | No | Draw period ends 2028 |

| Student loan group A | Installment | $22,600 | 5.10% | $265 | 10th | Yes | Verify repayment plan yearly |

| Auto loan | Installment | $9,850 | 4.49% | $315 | 22nd | Yes | Extra $100 principal monthly |

| Credit card (travel) | Revolving | $4,200 | 24.99% | $140 | 18th | Yes | Promo balance transfer ends May |

| BNPL (electronics) | BNPL | $900 | 0% (if on time) | $150 | Weekly | No | Late fees apply after 7 days |

If you maintain this, you’ll know your debt position in under 60 seconds. That’s what “control” feels like.

Common mistakes that make your liabilities wrong (even when you’re trying)

Mistake 1: Tracking the original loan amount

Your lender does not care that you “originally borrowed $30k.” Track the current balance. Net worth is a present-tense number.

Mistake 2: Ignoring variable rates

HELOCs, some student loans, and many credit lines float. If rates change and you don’t update, your payoff plan becomes a fairy tale.

Mistake 3: Forgetting deferred interest terms

Some promos are “0% if paid in full by X date.” Miss the date and the interest can retroactively apply. Read the fine print like it personally insulted you.

Mistake 4: Letting BNPL live outside your system

BNPL is still debt. It still reduces net worth. It still claims future cash flow. The only thing “buy now” about it is the dopamine.

Mistake 5: Not tracking liabilities because “I’m investing more now”

Investing while ignoring debt is like installing marble countertops while the foundation is on fire. Sometimes it’s fine. Often it’s delusion.

How FIYR makes liability tracking less painful (and more accurate)

You can track liabilities in a spreadsheet. People also floss daily. In theory.

FIYR is built to make this process easier to stick with by keeping your money picture in one place:

- Net worth tracking that includes both assets and liabilities, so your progress is real, not motivational.

- Income and expense tracking so you can see how debt payments hit cash flow.

- Custom categories and category groups to keep debt-related transactions clean.

- Automatic transaction rules to reduce miscategorization and keep your budget from turning into a junk drawer.

- Savings rate tracking and FIRE-focused insights, because debt payoff is often the fastest way to improve your financial trajectory.

The vibe is simple: fewer spreadsheets, fewer forgotten balances, more decisions you can defend.

If you’re rebuilding after Mint, you’ll also appreciate why FIYR is positioned as a modern alternative that’s flexible and customization-friendly. (Mint was great, until it wasn’t. Like many relationships.)

A monthly “Liability Review” you’ll actually do (10 minutes)

Put this on your calendar. Make it recurring. Treat it like brushing your teeth, except it saves you money.

- Update each liability balance

- Confirm due dates and minimums

- Check for promo APR end dates in the next 90 days

- Scan your transactions for any “new debt behavior” (rising card balances, new BNPL payments)

- Decide one action for the next month (extra payment, refinance research, balance transfer payoff plan)

One-liner: What gets reviewed doesn’t get out of hand.

Frequently Asked Questions

What’s the best way to track liabilities without missing anything? Use a single source of truth and track the fields that prevent surprises: current balance, APR, minimum payment, due date, autopay status, and notes for promos or term changes. Then reconcile monthly. Should I include BNPL in my net worth calculation? Yes. If you owe money, it’s a liability, even if the app makes it feel like a “payment plan.” Leaving BNPL out inflates your net worth and understates future cash flow commitments. Do I track credit card debt as the statement balance or current balance? For net worth, use the current balance (what you owe today). For payment planning, the statement balance matters because it’s what avoids interest if you pay in full. Is a 401(k) loan a liability? Yes. You owe it back on a schedule, and missed payments can create taxes and penalties. Track it like any other installment loan. How often should I update my liabilities? Monthly is enough for most people. Weekly helps if you’re aggressively paying down revolving debt, using BNPL frequently, or managing variable income. What’s the biggest mistake people make when tracking liabilities? They track payments but not balances. Payments are cash flow. Balances are reality.CTA: Turn your liabilities from “mystery meat” into clean data

If you want your net worth to mean something (and not just flatter you), start tracking liabilities like a grown-up with a Wi‑Fi connection.

FIYR helps you keep liabilities, spending, net worth, and FIRE progress in one place, with customization and rules that cut down on the busywork. If you’re coming from Mint or debating Monarch, Copilot, Rocket Money, or Quicken, this is the part where you stop duct-taping spreadsheets together.

Explore more on net worth tracking, including what to look for in a tool, in Best Net Worth Tracker for 2026: Honest Comparison + What to Look For.