Money Resolutions 2026: Make Them Unbreakable With One System

If your money resolutions 2026 plan is “try harder,” I have bad news: willpower has the half-life of a grocery store rotisserie chicken.

Meet Jake. January 2, he vows to “save more” and “stop eating out.” January 17, he’s ordering DoorDash because work was chaos and cooking feels like a second job. February 3, he checks his bank app and whispers the ancient personal finance prayer: “Where did it go?”

Jake isn’t lazy. Jake just doesn’t have a system. And money without a system is like a leak without a bucket. Eventually, your floor is wet.

Why money resolutions fail (it’s not your character, it’s your calendar)

Most people set resolutions like they’re making wishes on a birthday candle: vague, emotional, and instantly forgotten.

Also, the environment is brutal.

- 60% of Americans are still living paycheck to paycheck (CNBC, 2023). That leaves basically zero margin for error, or surprise tires, or “it’s been a week” sushi.

- 70% are stressed about finances, which makes rational decision-making about as likely as a calm group chat.

- Only 45% have an emergency fund, and among those, 26% have less than $5,000 saved.

- 61% carry credit card debt, averaging $5,875, with a chunk going deeper monthly.

Source: CNBC

So if you’re trying to “be better with money” in 2026 while your budget is held together with vibes, you’re not failing. You’re simply bringing a spoon to a knife fight.

Here’s the part nobody talks about: resolutions don’t fail because they’re too ambitious. They fail because they’re not operational.

Quotable truth: A goal without a routine is just a fantasy with good PR.

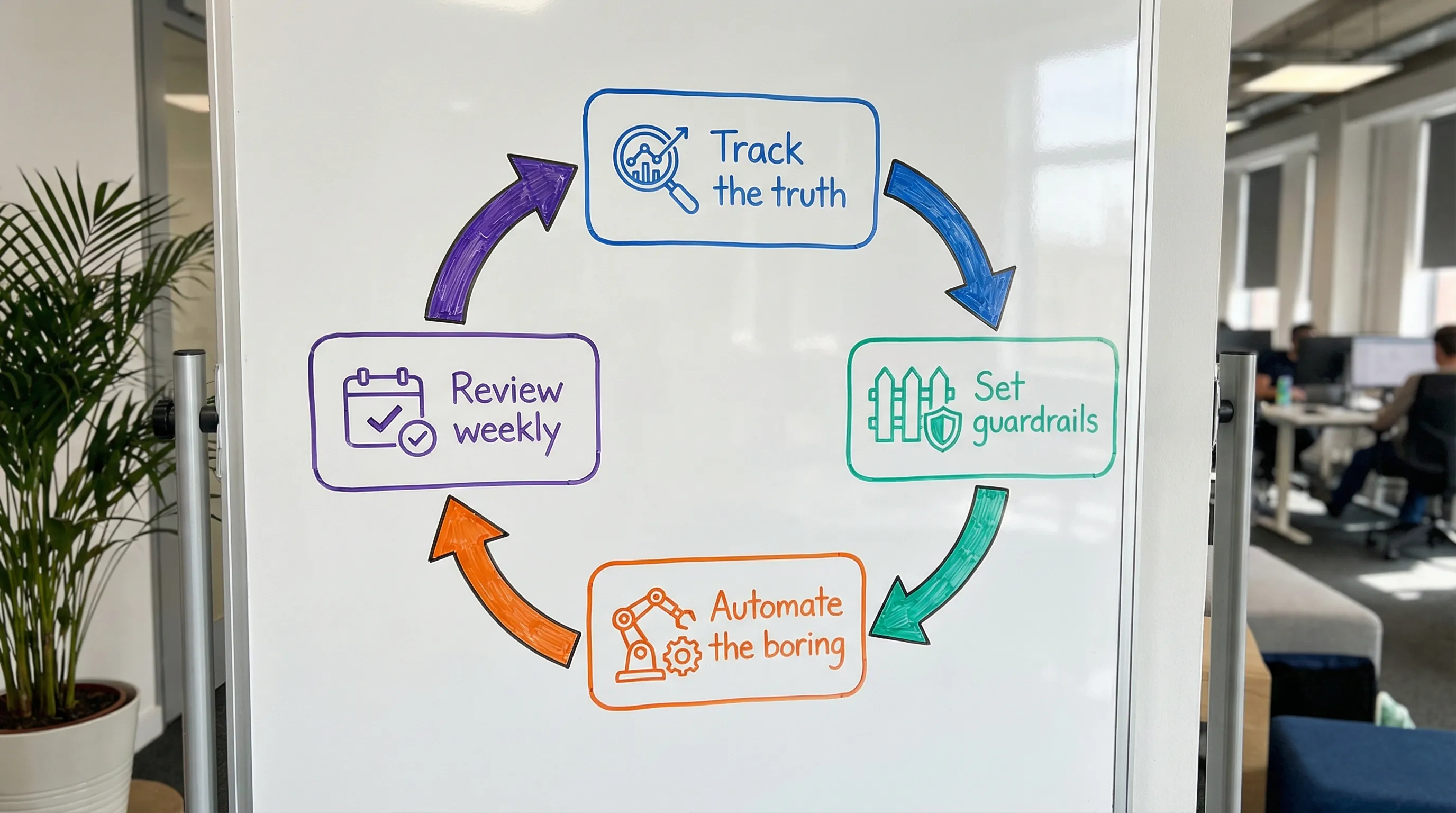

The one system that makes money resolutions unbreakable: the Loop

You need one repeatable mechanism that turns “I should…” into “I did.”

I call it The Loop:

1) Track the truth (fast)

2) Set guardrails (simple)

3) Automate the boring (consistent)

4) Review weekly (short)

That’s it. No 47-tab spreadsheet. No daily shame spiral. Just a loop you can run even when life is messy.

And yes, a modern money tracker makes this dramatically easier. FIYR is built for exactly this kind of loop: spending tracking, flexible budgets, automatic transaction rules, subscription tracking, net worth, savings rate, and FIRE projections, without feeling like you enrolled in an accounting degree.

Quotable truth: Your budget isn’t broken. Your feedback loop is.

Step 1: Track the truth (because optimism is not a financial strategy)

Tracking is not about perfection. Tracking is about not lying to yourself with confidence.

Your job in this step is simple: create a clean view of what’s actually happening.

The “Truth Snapshot” (20 minutes)

Pick a recent 30 to 90 days window and answer:

- What’s my average monthly spend?

- What’s my top 5 spending categories?

- What recurring charges hit every month?

- What’s my current savings rate?

If you’re coming from Mint (RIP), this is where many people faceplant: exports, messy categories, missed subscriptions, and duplicate transfers. Tools like FIYR are designed to make the “truth” easier to capture and maintain, especially if you want a Mint-style view but more control.

If you want a deeper setup walkthrough, FIYR has a clean starting point here: FIYR budgeting tutorial: your first week setup.

Quotable truth: If your numbers are dirty, your decisions are fiction.

Step 2: Convert resolutions into guardrails (not vibes)

Most resolutions are adjectives:

- “Better”

- “More”

- “Less”

- “Finally”

Guardrails are verbs plus numbers:

- “Keep dining out under $350/month.”

- “Auto-move $250 to savings on payday.”

- “Cap subscriptions at $60/month.”

The Resolution Translator (steal this)

Use this format:

Resolution → Metric → Rule → TriggerHere are examples that actually survive real life:

| Money resolution | Metric to track | Guardrail rule | Trigger to run it |

|---|---|---|---|

| “Save more” | Savings rate (or $ saved) | Auto-transfer a fixed amount on payday | Payday (every paycheck) |

| “Stop overspending” | Safe-to-spend balance | Weekly flex allowance, spend from that first | Every Monday |

| “Pay off debt” | Highest APR balance | Extra payment amount set as a monthly goal | Month start |

| “Cut subscriptions” | Total subscription spend | Subscription cap + one-in-one-out rule | New signup attempt |

| “Retire earlier” | FIRE date + burn rate | Reduce one high-leverage category by 5% | Monthly review |

FIYR helps because it’s not just a budgeting app, it’s a money scoreboard: savings rate, net worth, subscriptions, and a FIRE date calculator tied to your real data.

Related deep-dives if you want them:

- Reduce subscriptions in 2026: a 30-minute cleanup plan

- Savings rate calculator: the one metric that matters

Quotable truth: A guardrail beats a pep talk every time.

Step 3: Automate the boring (so your future self doesn’t sabotage you)

The enemy of financial progress isn’t ignorance. It’s Tuesday.

Automation turns your “good intentions” into default behavior. The goal is fewer decisions, fewer chances to drift.

The Big 3 automations (high impact, low drama)

Pay-yourself-first routing

On payday, route money in a set order. A simple version:

- Minimums and fixed bills

- Savings or investing

- Debt extra payment (if applicable)

- Flex spending

If you have irregular income, you’ll want a baseline approach instead of paycheck-to-paycheck chaos. Start here: variable income budgeting system.

Subscription containment

Subscriptions are the financial equivalent of “just one more episode.”

Set a monthly subscription cap, then enforce:

- One-in-one-out (new subscription requires canceling another)

- Annual fees get monthly sinking funds

- Trials get a calendar reminder the day you sign up

FIYR’s subscription tracking is made for this, because you can actually see recurring charges and stop playing “Guess That $14.99.”

Transaction rules (so your categories stop gaslighting you)

If your “Dining” category includes Starbucks, DoorDash, and that one time you bought batteries at Walgreens, your data is screaming for help.

Rules-based categorization means your tracker learns your life patterns and stops asking you to manually tag every transaction like it’s 2011.

If you want the nerdy-but-practical version: spending rules automation.

Quotable truth: Automate what you’re tired of failing at.

Step 4: The weekly review (15 minutes, no self-loathing)

This is where the magic happens, because it’s where you close the loop.

A weekly review is the difference between:

- “I think we’re fine”

- “We are not fine, but we can fix it before it becomes a $900 problem.”

The 15-minute Money Meeting script

Do this once a week, same day, same time.

- Check your safe-to-spend (or the closest equivalent you track).

- Review your top 3 categories for the week.

- Flag anything weird (duplicates, mis-categorized transfers, surprise charges).

- Choose one micro-action for next week.

Micro-actions that work:

- Drop your dining cap by $25 this week.

- Cancel one subscription.

- Move one bill to autopay.

- Set one transaction rule for a merchant that keeps showing up.

The point is not to be perfect. The point is to be consistent.

Quotable truth: Weekly beats heroic.

The “Unbreakable” part: design for your worst week

The best money system is the one that works when:

- your kid is sick

- you’re traveling

- your boss discovered “urgent” at 4:47 PM

- your brain is fried and your wallet is loose

So build a system that assumes you’re not a robot.

Minimum Viable Money Routine (MVMMR)

Make the default small enough that you keep doing it.

- Weekly: 15-minute review

- Monthly: one “close the month” cleanup (categories, subscriptions, goals)

- Quarterly: one bigger audit (insurance, rent, debt refi check, goals refresh)

If you want a broader habit framework, this pairs nicely with: how to build financial habits that survive real life.

Quotable truth: Your plan should survive a bad Tuesday, not just a perfect January.

Quick-start: your 72-hour money resolutions 2026 reboot

If you do nothing else, do this.

- Day 1: Track the truth (connect accounts, clean obvious categories, find recurring charges).

- Day 2: Set 3 guardrails (one spending cap, one savings move, one subscription rule).

- Day 3: Schedule your weekly review and automate one thing (payday transfer or transaction rule).

If you want a bigger reset with fewer moving parts, you can also steal the structure from: why budgets fail (and how to fix yours in 2026).

Quotable truth: Momentum loves a calendar invite.

Frequently Asked Questions

What are the best money resolutions for 2026? The best ones are measurable and tied to a routine: build an emergency buffer, cut subscription waste, raise your savings rate, and pay down high-interest debt. Why do I always quit my money resolutions by February? Usually because the resolution is vague and there’s no weekly review loop. You need guardrails, automation, and a short cadence to course-correct. How many financial resolutions should I set for 2026? Three is a power number: one stability goal (cash buffer), one wealth goal (savings/investing), one lifestyle goal (spending cap that protects joy). What’s the simplest system to keep money resolutions? Track the truth, set guardrails, automate the boring, and review weekly. If your system requires daily motivation, it’s a fragile system. Do I need a budgeting app to stick to money resolutions 2026? You can do it manually, but apps reduce friction. A tool like FIYR helps by tracking spending, subscriptions, savings rate, net worth, and your FIRE timeline in one place.Make 2026 the year your money resolutions stop being comedy

If you’re tired of starting over every January, stop hunting for motivation and start installing infrastructure.

FIYR is built for the exact system you just read: clean spending tracking, flexible budgets, automation rules, subscription visibility, savings rate and net worth tracking, and FIRE-focused insights.

If you want to run The Loop with less manual work, explore FIYR at blog.fiyr.app and start with a simple setup guide like Custom budget setup in 30 minutes.

Final quotable truth: 2026 won’t change your money. Your system will.