Money Planning Before Buying a Home: The Checklist That Saves You

Buying a home is the adult version of adopting a dragon.

Looks majestic on Instagram. Eats cash in private.

Here’s the uncomfortable truth: most people “qualify” for a mortgage on paper, then get mugged by the boring costs in real life. The down payment is just the bouncer at the club. Inside, you’ll meet closing costs, escrow, repairs, moving, higher utilities, and the little gremlin named “Home Depot on a random Tuesday.”

And because America loves chaos, a lot of buyers are trying to do this with finances held together by duct tape and good intentions. Per CNBC reporting, about 60% of Americans live paycheck to paycheck, 70% are stressed about money, and only 45% have an emergency fund (with many under $5,000). Also, 61% carry credit card debt. That’s not a moral failing, it’s a math problem with a marketing budget.

This post is your money planning before buying a home checklist, the one that saves you from becoming “house poor” with granite countertops.

The real goal: buy a home without buying financial stress

Meet Jenna and Marco.

They’re responsible-ish. They meal prep sometimes. They have a spreadsheet they respect, like a household pet.

They saved a down payment, got pre-approved, and started touring homes. Then the inspector casually mentioned the HVAC was “functioning… spiritually.” Replacement quote: $9,200.

They didn’t walk because they were dumb. They walked because their plan only included the down payment.

Your goal is not “get the keys.” Your goal is:

- Close with enough cash left to sleep.

- Afford the monthly payment without playing whack-a-mole with credit cards.

- Keep your other goals alive (emergency fund, debt payoff, investing, FIRE plans).

A mortgage is a monthly subscription you cannot cancel without a legal process. Choose accordingly.

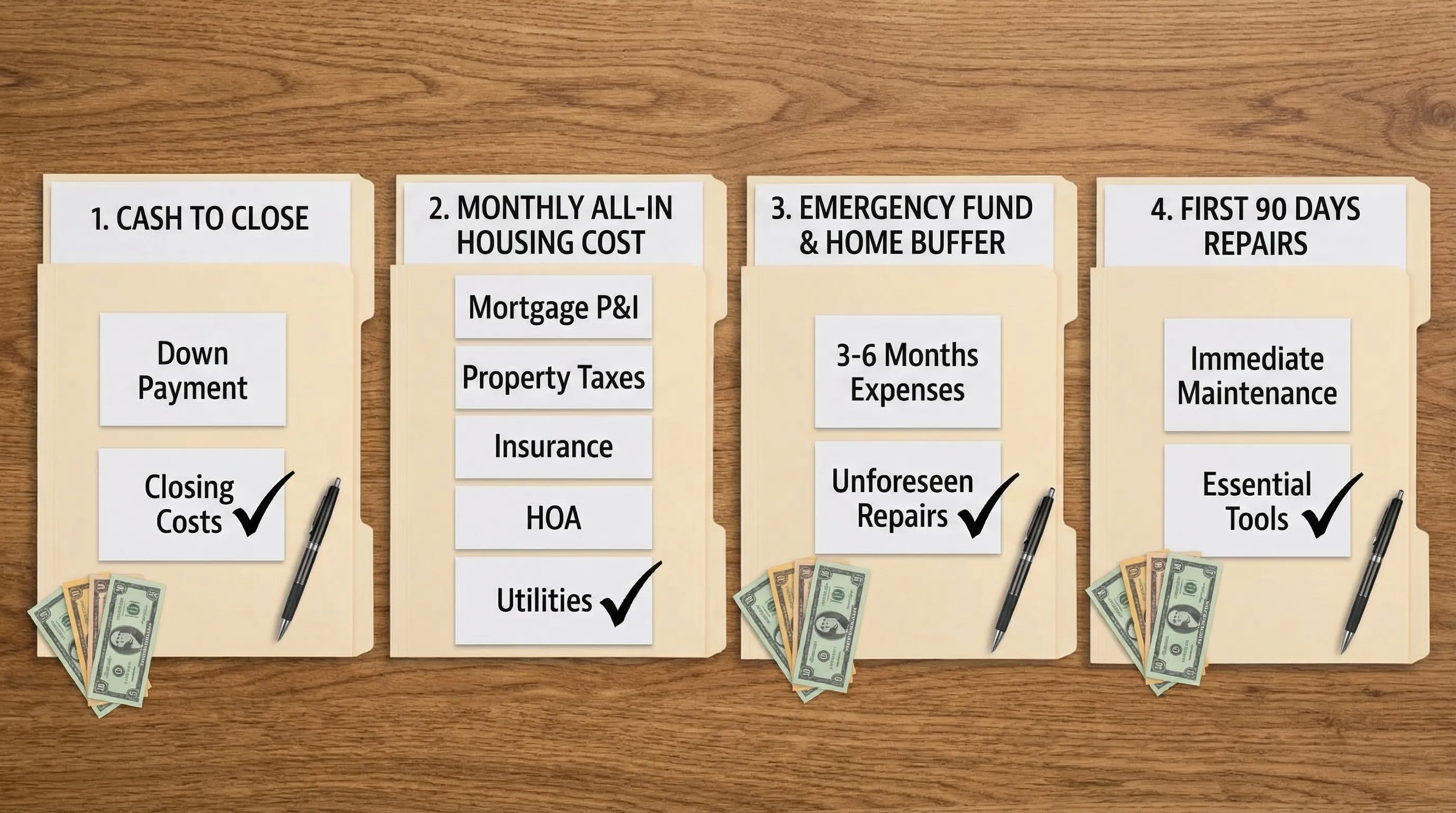

Step 1: Calculate your “All-in Cash to Close” (not just down payment)

Most first-time buyers plan like this:

Down payment ✅

And then they act shocked when the universe presents the invoice.

The cash buckets you need before you make an offer

Closing costs often run roughly 2% to 5% of the purchase price, depending on location and loan details. The Consumer Financial Protection Bureau (CFPB) has a helpful explainer on what shows up in your closing disclosure.

Here’s the checklist that matters.

| Cash item | What it covers | How to plan it (simple) |

|---|---|---|

| Down payment | Your equity from day one | Set a target percent or dollar amount based on your loan type and risk comfort |

| Earnest money | Good-faith deposit | Keep it liquid, assume it will be tied up during escrow |

| Inspection + appraisal | Due diligence + lender requirement | Assume $500 to $1,500+ depending on area and property complexity |

| Closing costs | Lender fees, title, escrow, prepaids | Estimate 2% to 5% of purchase price, refine once you get loan estimates |

| Moving + setup | Trucks, movers, deposits, tools, “wait, we need curtains?” | Use a flat placeholder (ex: $2,000 to $8,000), then adjust after quotes |

| Immediate repairs | The stuff you cannot ignore | Create a “First 90 Days” buffer (often $1,000 to $10,000+) |

| Post-close cash cushion | Your sanity fund | Minimum: emergency fund stays intact, plus a home buffer |

If you only remember one line: Cash to close is not the finish line, it’s the starting line.

The “Cash to Close + Sleep” formula

Use this as a planning baseline:

Total cash needed = down payment + closing costs + inspection/appraisal + moving/setup + first-90-days repairs + minimum cash cushionNotice what’s missing: vibes.

Step 2: Run the “Monthly Reality” math (the payment is not the cost)

A mortgage payment is the headline. Homeownership is the full article.

Most buyers focus on principal and interest, then get blindsided by:

- Property taxes (that can jump after purchase)

- Homeowners insurance

- PMI (if applicable)

- HOA dues

- Utilities that are suddenly… mature

- Maintenance and repairs

A common planning rule of thumb is budgeting 1% to 3% of the home’s value per year for maintenance, depending on age and condition. Some years you’ll spend $200. Other years your water heater will choose violence.

Build your “All-in Housing Cost” estimate

| Monthly cost | What to include | How it surprises people |

|---|---|---|

| Mortgage (P+I) | Loan payment | Rate changes what you can afford fast |

| Property taxes | Monthly escrow portion | Assessed value can reset after sale |

| Homeowners insurance | Monthly escrow portion | Premiums can rise, especially in higher-risk areas |

| HOA | Dues, special assessments | Special assessments are basically surprise boss fights |

| Utilities | Electric, gas, water, trash, internet | Bigger space, bigger bills |

| Maintenance fund | Repairs, replacements, seasonal upkeep | Not optional, just delayed if unfunded |

Add them up and compare to your current housing cost.

Then do the part nobody wants to do.

The “3-month pretend mortgage” stress test

Before you buy, simulate the new housing payment for 3 months.

You do this by transferring the difference between your current housing cost and your projected all-in cost into a separate account (or at least a dedicated “Home” goal).

If that transfer makes your month feel like a hostage situation, congrats, you just avoided becoming house poor.

Your future budget should not swing like a crypto chart.Step 3: Protect the emergency fund (your anti-foreclosure device)

If your emergency fund becomes your down payment, you are not “resourceful.” You are “one surprise expense away from panic.”

CNBC’s reporting highlights how thin the margin is for many households: only 45% of adults said they have emergency savings, and many who do have under $5,000 saved. (Source)

Here’s a clean approach:

- Keep your core emergency fund intact (often 3 to 6 months of bare-bones expenses).

- Add a separate homeownership buffer (even $2,000 to $10,000 to start).

- If your down payment plan requires draining both, you’re not “ready,” you’re “overreaching.”

A house is a lever. An empty emergency fund is the fulcrum snapping.

If you want a deeper emergency fund playbook, FIYR has a solid guide on building a safety net that actually holds: Emergency Fund Guide.

Step 4: Clean up debt and credit before underwriting gets nosy

Underwriters are not impressed by your “girl math.” They want clean lines.

CNBC also notes 3 in 5 Americans (61%) are in credit card debt, owing an average of $5,875. That matters because high-interest debt eats the very cash flow you need to handle homeownership.

Pre-approval is not the time for new debt

If you’re within 3 to 6 months of buying:

- Avoid opening new credit cards unless necessary.

- Don’t finance furniture “because it’s 0%.” It’s still a payment.

- Pause BNPL behavior (it can muddy your debt picture).

- Keep utilization low and payments on-time.

And if you have high-interest balances, your best “down payment hack” might be paying them down first.

Want a clean system for keeping liabilities truthful? Start here: How to Track Liabilities Accurately Without Missing Details.

Step 5: Use guardrails, not generic rules

You’ve heard the internet’s greatest hits:

- “Don’t spend more than 30% on housing.”

- “Do 20% down or you’re doomed.”

These rules are not evil. They’re just incomplete. Your life is not a median statistic.

Instead, use a guardrail dashboard. It’s less sexy, more effective.

| Metric | Green | Yellow | Red |

|---|---|---|---|

| Housing cost as % of take-home pay | 25% to 35% | 35% to 45% | 45%+ |

| Fixed costs as % of take-home pay (housing + debt + insurance + childcare) | Under 50% | 50% to 65% | 65%+ |

| Savings rate after buying | 15%+ | 5% to 15% | Under 5% |

| Cash buffer after closing | Emergency fund intact + home buffer | Emergency fund reduced | Emergency fund drained |

This is the part where people get honest. If your dashboard turns red, it’s not a failure. It’s a signal.

The bank approves your loan, your budget approves your life.The checklist that saves you (print this, tattoo it, whatever works)

This is the core of money planning before buying a home. Not glamorous, extremely profitable.

60 to 90 days before you shop seriously

- Pull 60 to 90 days of real transactions and calculate your true monthly baseline (including the “random” stuff that is somehow always there).

- Build your first draft “All-in Cash to Close” number.

- Run a subscription audit, because hidden recurring charges have immaculate timing.

- Start the 3-month pretend mortgage stress test by transferring the estimated payment difference into savings.

- Decide your non-negotiables: minimum emergency fund, minimum savings rate, max fixed-cost ratio.

If your numbers feel fuzzy, that’s not because you’re bad at money. It’s because you’re missing a system.

30 days before you make offers

- Get initial loan estimates and update your closing-cost range.

- Create a “First 90 Days Repairs” buffer (even if it’s small).

- Pay down revolving debt if your utilization is high.

- Freeze your budget categories so you can compare month to month cleanly.

- Start tracking home-related spending separately (inspection, appraisals, contractor quotes) so it doesn’t camouflage itself as “misc.”

Here’s the part nobody talks about: the best time to practice homeownership is before you own the home.

Offer week (yes, money still matters when emotions spike)

- Confirm you will still have cash after closing.

- Double-check that the new monthly payment fits your guardrails.

- Decide your walk-away line on inspection items.

- Keep your accounts boring, no big deposits, no mysterious transfers, no “I sold a jet ski for cash” energy.

Also, if you ever need to write a letter of explanation (for a credit inquiry, deposit, or job change) and you use AI to draft it, make it sound like a human who pays bills. Tools that help you sanity-check whether your text reads “robotic” can be useful, here’s a directory of AI text detection and humanizer tools.

First 90 days after closing

- Set a monthly maintenance transfer (treat it like a bill).

- Create sinking funds for predictable-but-irregular costs (insurance renewals, property taxes if not escrowed, seasonal maintenance).

- Track your new “fixed cost ratio” and adjust lifestyle spending if needed.

- Do one monthly net worth check-in, because the mortgage is a liability and home equity is not the same thing as cash.

If you need a sinking fund walkthrough, start here: Sinking Funds Guide.

How FIYR makes this easier (without turning you into a spreadsheet goblin)

Buying a home is a data problem pretending to be a feelings problem.

FIYR is built for the part that actually moves the needle: clean tracking, flexible budgets, and goal clarity, especially if you are coming from Mint or trying to pick between Monarch Money, Copilot, Rocket Money, or Quicken.

Here’s a simple setup that works:

Track the purchase like a project

Create a dedicated label like “Home Purchase 2026” and tag everything that touches the transaction. Inspections, appraisals, earnest money, rate lock fees, it all gets captured.

One home purchase, one clean story.

Build decision-focused categories

Instead of letting everything become “Fees” or “Other,” use categories that map to choices:

- Closing Costs

- Moving + Setup

- Repairs (First 90 Days)

- Home Maintenance (Ongoing)

If you want a clean category system, FIYR’s template approach is here: Budgeting Categories List: A Clean Setup That Works.

Use goals and safe-to-spend so you do not guess

Home buying breaks people because they keep asking: “Can we afford this?”

FIYR helps you answer with a practical number: safe-to-spend, plus goal tracking for your down payment, closing costs, and reserves.

And when your transactions are categorized consistently, your budget stops being inspirational fiction.

Common mistakes (so you can skip the pain)

Most homebuyer mistakes are not dramatic. They’re boring, consistent, and expensive.

- Planning for the down payment but not the “All-in Cash to Close.”

- Buying at the top of your pre-approval range because the lender said it was fine.

- Draining the emergency fund and calling it a “temporary sacrifice.”

- Ignoring maintenance until it becomes debt.

- Letting subscriptions and lifestyle creep quietly eat the margin you needed.

Frequently Asked Questions

How much money should I save before buying a home? A practical baseline is: down payment + estimated closing costs (often 2% to 5% of purchase price) + moving/setup + a first-90-days repair buffer, while keeping your emergency fund intact. What’s the biggest money mistake people make before buying a house? Confusing “mortgage payment” with “total cost of ownership.” Taxes, insurance, HOA, utilities, and maintenance turn a comfortable payment into a stressful month fast. Should I pay off credit cards before buying a home? If you carry balances at high APR, paying them down can improve cash flow and reduce risk. It can also help credit utilization, which may support better loan terms. How can I stress test whether I can afford the new payment? Run a 3-month pretend mortgage by transferring the difference between your current housing cost and your projected all-in housing cost into savings. If your budget breaks, your plan was fantasy. Do I need a separate fund for home repairs? Yes. Even small repairs arrive with perfect timing. A dedicated home buffer prevents you from using credit cards as your maintenance plan.Ready to buy a home like a grown-up?

If you’re serious about money planning before buying a home, stop relying on bank-balance vibes.

FIYR helps you track income, spending, subscriptions, net worth, savings rate, and goals in one place, with custom categories and automation rules that keep your numbers clean. That matters when you’re making the biggest purchase of your life.

Set up a “Home Purchase” goal, run the 3-month stress test, and let your data tell you the truth before the house does.