Habits That Improve Financial Success (No, Not “Skip Lattes”)

Your financial plan doesn’t fail because you bought a latte.

It fails because your system is basically: “I hope the vibes improve.”

And the vibes are not improving. In the U.S., about 60% of people are living paycheck to paycheck, roughly 70% are stressed about money, only 45% say they have an emergency fund, and 61% carry credit card debt (average balance $5,875) according to reporting cited by CNBC. That’s not a “too much oat milk” problem. That’s a “the floor is lava and the lava is interest charges” problem.

So let’s talk about habits that improve financial success that actually move the needle, without turning your life into a sad spreadsheet monastery.

The real secret: financial success is boring (and that’s good)

Meet Jordan. Solid job. Solid intentions. Zero clue where the money goes.

Jordan’s strategy was classic:

- Get paid

- Pay bills

- Spend whatever is left

- Swear to “be better next month”

Then Jordan finally tracked spending for real and discovered three things:

- Subscriptions were multiplying like gremlins after midnight.

- “Random” spending wasn’t random, it was a category (and it was huge).

- The “savings plan” was just leftover money, which is the financial equivalent of “I’ll work out if I have time.”

Here’s the part nobody talks about: you don’t need more discipline. You need a tighter feedback loop.

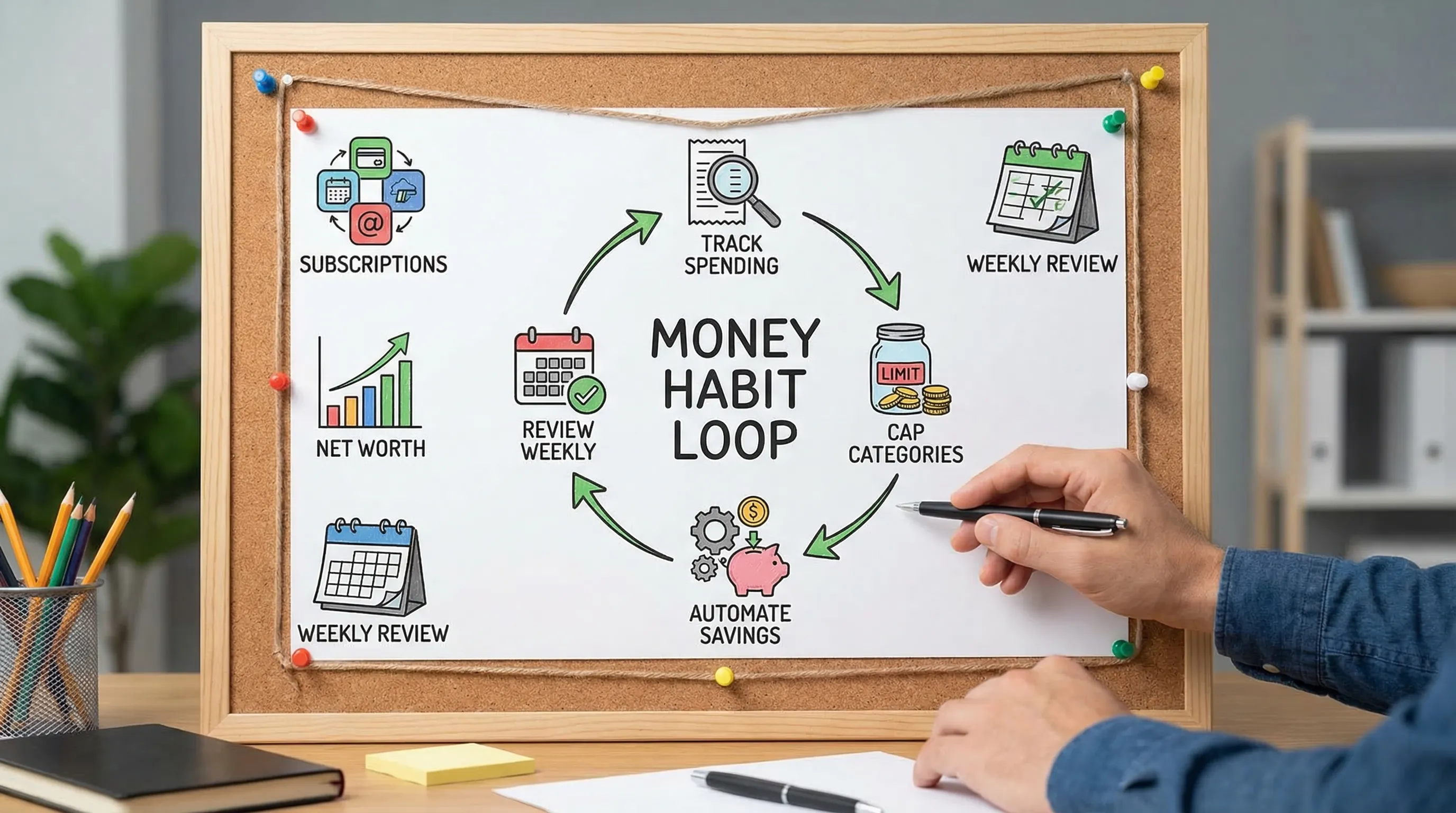

Habit #1: Keep a “Money Scoreboard” (because vibes are not a metric)

If you only track one thing, track net worth. If you track three things, track what actually drives it.

A simple scoreboard turns “I think we’re fine?” into “I know exactly what’s happening.”

| Scoreboard item | What it tells you | Why it improves financial success | How often to check |

|---|---|---|---|

| Safe-to-spend | What you can spend without detonating bills and goals | Prevents accidental overspending (the most common kind) | Weekly |

| Savings rate | How fast you’re buying your freedom | Small % changes can mean years off your FI timeline | Monthly |

| Subscription total | Your monthly “silent spend” | Recurring charges are the sneakiest lifestyle creep | Monthly |

| High-interest debt trend | Whether interest is eating your future | Debt is negative compounding, it’s impressively rude | Monthly |

| Net worth trend | Your real financial progress | Keeps you focused on outcomes, not budget theater | Monthly |

If you’re FIRE-minded, this scoreboard is basically your cockpit.

Light FIYR tie-in: FIYR is built for this style of tracking, with net worth, subscription tracking, savings rate, and a safe-to-spend balance so your money decisions stop being interpretive dance.

Quotable truth: If you don’t measure it, you’re not managing it, you’re guessing with confidence.

Habit #2: Do a 15-minute weekly money check-in (the habit that makes all other habits stick)

Most people “budget” once a month, like it’s a dental cleaning. Then life happens, Target happens, and the budget becomes historical fiction.

A weekly check-in fixes that.

The 15-minute script (steal this)

- Minute 1 to 3: Look at the last 7 days of transactions. If anything looks weird, label it.

- Minute 4 to 8: Check your safe-to-spend. If it’s low, pick one lever (pause dining out, slow Amazon, cancel a subscription).

- Minute 9 to 12: Move money once (to savings, sinking funds, or debt). One action, not ten.

- Minute 13 to 15: Decide one micro-rule for next week (example: “No delivery apps on weekdays”).

This habit works because it creates fast feedback. You stop discovering problems after the credit card statement arrives wearing clown makeup.

If you want a deeper system, FIYR has a great companion read on the weekly ritual in Why You’re Overspending (And the One Habit That Could Save You $50,000).

Quotable truth: A budget you don’t review is just a wish with formatting.

Habit #3: Automate “Future You” first (because willpower has a bedtime)

People love advice like “just save more.” Cool. And just be taller.

The habit that actually works is: pay yourself first, automatically, right after payday.

The simplest automation ladder

Set these in order:

- A small automatic transfer to emergency savings

- A retirement/investing auto-contribution (401(k), IRA, taxable, as appropriate)

- A bills buffer (so due dates don’t bully you)

If you get paid irregularly, automation still works, it just needs a baseline. FIYR covers the approach in Variable Income Budgeting: A System for Feast-or-Famine Paychecks.

Light FIYR tie-in: FIYR helps because you can track income and expenses, see the real leftover cash, and set goal tracking so automation isn’t “set it and pray.”

Quotable truth: If saving is optional, it becomes fictional.

Habit #4: Use guardrails, not guilt (caps beat lectures)

Most budgets fail because they try to micromanage everything. That’s adorable. You have a life.

Instead, cap the chaos categories. The ones where spending can silently triple:

- Dining out

- “Shopping” (aka modern therapy)

- Convenience spending (delivery, rideshares)

- Entertainment

Your goal is not deprivation. Your goal is friction and visibility.

A practical guardrail setup

Pick 2 to 4 categories and set monthly caps that are realistic, not aspirational.

Then add one rule for when you hit the cap:

- You pause spending

- Or you move money from a lower-priority category

- Or you decide consciously, “I’m breaking the cap, and I’m fine with it”

That last one is key. You’re not failing, you’re choosing.

Light FIYR tie-in: FIYR’s dynamic budgets, custom categories, and safe-to-spend make caps feel like bumpers on a bowling lane, not handcuffs.

If you want the clean setup, grab Custom Budget Setup in 30 Minutes: A Clean, Flexible System.

Quotable truth: You don’t need a perfect budget. You need speed bumps in the right neighborhoods.

Habit #5: Make “surprise bills” illegal with sinking funds

Your car registration is not a surprise. Your annual insurance premium is not a surprise. Your holiday spending is not a surprise.

They’re predictable. They’re just not monthly. Which is why they keep showing up like uninvited guests.

Sinking funds fix this by monthly-izing real life.

The tiny math that changes everything

Monthly sinking fund amount = total cost ÷ months until dueDo that for 3 to 5 big “lumpy” expenses and your financial stress drops fast.

If you need a full walkthrough, FIYR already has the playbook: Sinking Funds Guide: Stop Getting Blindsided by Bills.

Quotable truth: Adults don’t have surprise bills. They have underfunded predictables.

Habit #6: Run a monthly “subscription and fees” audit (because recurring charges are tiny vampires)

Subscriptions are the perfect modern business model:

- Low enough that you ignore it

- Recurring enough that it compounds into pain

- Annoying enough to cancel that you “do it later”

And later becomes never.

The monthly audit (10 minutes)

- Sort by merchant and look for anything recurring

- Cancel what you don’t actively use

- Downgrade what you use casually

- Put a cap on total subscriptions (one number, not vibes)

Need the step-by-step? Use Reduce Subscriptions in 2026: A 30-Minute Cleanup Plan.

Light FIYR tie-in: FIYR’s subscription tracking makes this habit easier because you can actually see the recurring charges instead of playing “Where’s Waldo” with your bank statement.

Quotable truth: The easiest money to save is the money you forgot you were spending.

Habit #7: Treat income like a strategy, not a hope

Yes, spending matters. But at a certain point, you can only cut so much before your life starts feeling like a canceled Netflix show.

Financially successful people build at least one intentional income lever:

- A raise plan

- A better job plan

- A monetizable skill plan

- A side income plan

The “One Skill, One Quarter” rule

Every 90 days, pick one skill that increases your earning power and put it on the calendar.

Not “learn AI.” That’s not a skill, that’s a press release.

Pick something concrete:

- Negotiation

- SQL

- Paid media

- Customer success

- Sales

- A certificate that your industry actually rewards

Then track the result like an adult:

- Income per month

- Savings rate impact

- Net worth trend

Light FIYR tie-in: FIYR helps here because income growth is only exciting if it converts into higher savings rate, goal progress, and a sooner FIRE date, not just higher DoorDash throughput.

Quotable truth: Cutting expenses is defense. Income is offense. You need both to win.

The 30-minute reset: install these habits this week

If you want momentum fast, do this in one sitting:

- Pull your last 30 days of transactions and identify your top 3 spending categories

- Set 2 category caps (the chaos categories)

- Create 2 sinking funds (car + holidays is a classic combo)

- Cancel 1 subscription

- Set 1 automatic transfer on payday (even $25 is a start)

- Schedule your weekly 15-minute money check-in

If you’re a former Mint user or you’ve tried Monarch, Copilot, Rocket Money, or Quicken and still felt like the numbers were fuzzy, your next move is not more “tips.” It’s a cleaner system.

FIYR was built to make this stuff less annoying: flexible budgeting, customizable categories, transaction rules, subscription tracking, net worth tracking, savings rate, and FIRE-focused projections, in one place.

Frequently Asked Questions

What are the most important habits that improve financial success? The highest-leverage habits are tracking a simple money scoreboard, doing a weekly 15-minute check-in, automating savings on payday, and capping chaos spending categories. How do I build financial habits if I’m living paycheck to paycheck? Start with visibility and one move: track spending weekly, cancel one recurring charge, and automate a small transfer ($10 to $50) to create a starter buffer. Is skipping lattes ever useful? Only if “lattes” is code for “I spend $400 a month on stuff I don’t care about.” The win is intentionality, not punishment. How often should I review my budget? Weekly for quick course corrections, monthly for a deeper review of savings rate, subscriptions, and progress toward goals. What should I track if I’m focused on FIRE? Savings rate, monthly spending (burn), net worth, and a projected FI date based on real data, not optimistic guesses.Ready to make this automatic (instead of aspirational)?

You can do all of this in a notebook, a spreadsheet, or your head, if you enjoy pain.

Or you can use a system designed for modern money chaos.

If you want a cleaner, more flexible alternative to Mint and legacy-style tools, explore the FIYR playbooks and setup guides here:

- Best Mint Alternative 2026: The Tools Worth Switching To

- Simple Budgeting App: Less Work, More Control

- Monthly Net Worth Tracking: The 10-Minute Ritual That Works

Because “financial success” isn’t a personality trait. It’s a repeatable set of habits, run on a schedule.