Net Worth Growth Strategies: The Boring Moves That Win

Net worth growth is aggressively unsexy.

It’s not “I bought an AI stock at the bottom” sexy. It’s not “I flipped a duplex on TikTok” sexy. It’s more like brushing your teeth, doing your taxes on time, and buying the same boring index funds while your group chat argues about crypto.

And yet, boring is exactly how most people actually win.

Here’s why this matters right now: according to a CNBC report, about 60% of Americans are living paycheck to paycheck, and 61% are in credit card debt. That’s not a “money knowledge” problem. That’s a “system” problem.

So let’s talk net worth growth strategies that work in real life, for real people, with real bills, real kids, real subscriptions, and real “why is my car making that noise” emergencies.

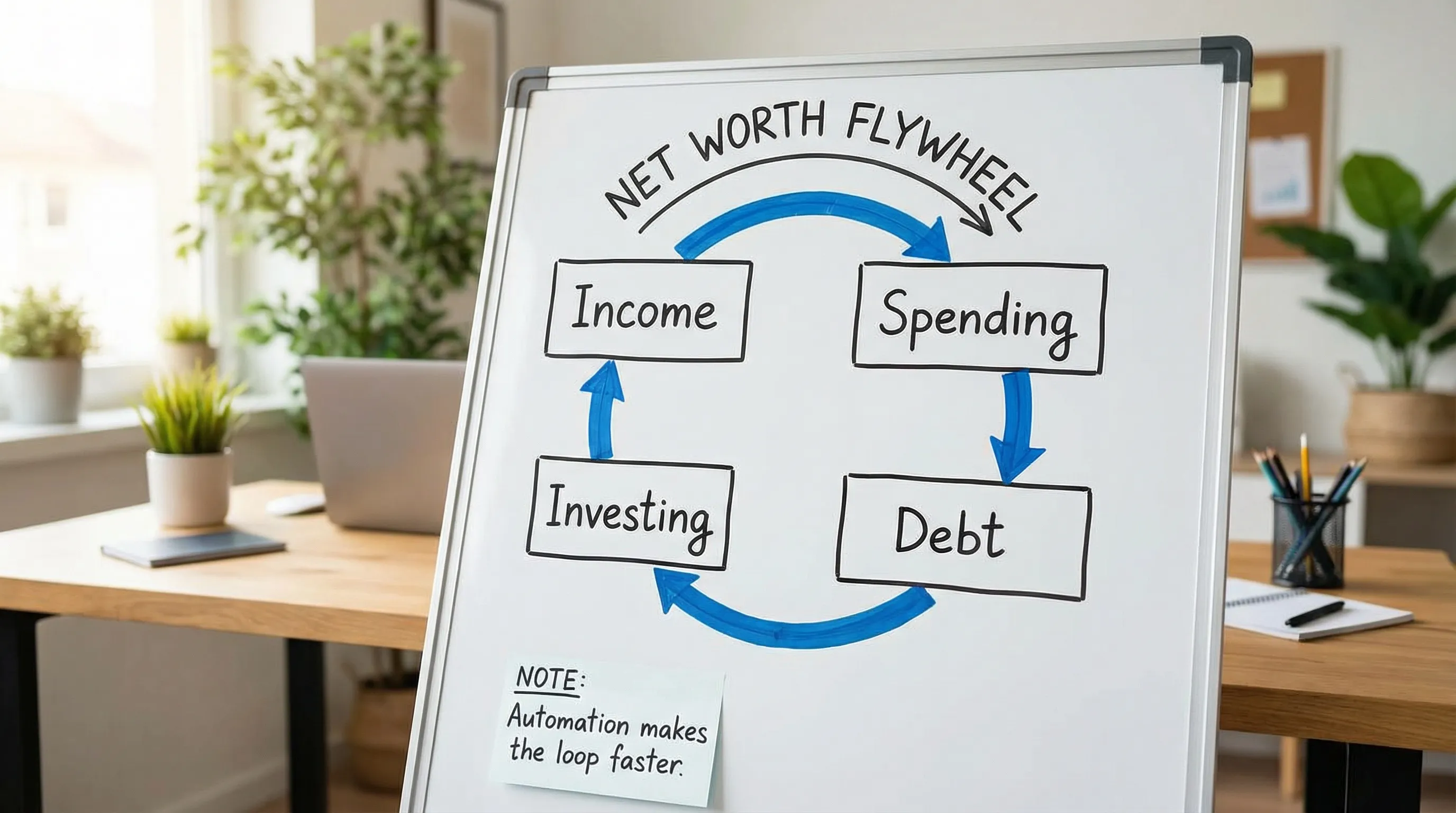

The net worth math (and the 4 levers you actually control)

Your net worth is simple:

Net worth = assets − liabilitiesThat’s it. No vibes. No manifestation. Just subtraction.

But growth happens through four levers:

- Cash flow (income minus spending): the fuel

- Savings rate: how much fuel you keep

- Returns (investing): the engine

- Interest rates (debt): the brake pedal you might be flooring by accident

Most people focus on the engine (returns) because it’s fun to argue about.

The real pros focus on fuel leaks and brake pedals. Because that’s where the easy wins live.

Quotable truth: You don’t need a hotter engine if your gas tank has holes.

Boring Move #1: Make your net worth number brutally honest

Meet “Kevin.” Kevin is a former Mint user who swears he’s doing fine. He invests. He budgets “kind of.” He checks his bank account like it’s a mood ring.

Then Kevin finally tracks everything and realizes:

- His “monthly spending” excludes the three annual bills that show up like jump scares

- His net worth ignores a lingering BNPL balance

- His “subscriptions” include an app he downloaded during the Obama administration

Kevin wasn’t broke. Kevin was under-informed.

This is the first boring move: turn on the lights.

The “Clean Net Worth” checklist (15 minutes)

You don’t need perfection, you need completeness.

- List core assets: cash, retirement, brokerage, home value (conservatively), vehicles (conservatively)

- List core liabilities: credit cards, student loans, car loans, mortgage, BNPL

- Add “forgotten but real” items: HSA, 529, old 401(k), TreasuryDirect, etc.

If you want the quick version, FIYR already has a walkthrough for the basics in How to Calculate Net Worth: A Simple Guide With Examples.

Here’s the part nobody talks about: most net worth “plateaus” are just missing data.

Where FIYR quietly helps

FIYR is built to keep the number honest by tracking assets, liabilities, income, expenses, and net worth in one place, with the kind of category control Mint never really nailed. Clean inputs, clean outputs, fewer financial fairy tales.

Boring Move #2: Stop negative compounding (aka kill high-interest debt)

Debt is not morally bad. It’s mathematically expensive.

If you’re carrying credit card debt at 20%+ APR (common in 2026 America), you’re not “behind.” You’re just investing in a guaranteed loss.

A simple priority rule

If a debt’s interest rate is higher than what you can reasonably earn after tax, after inflation, and after reality, pay it down aggressively.

This usually means:

- High-interest credit cards first

- Then other high-rate personal loans

- Then moderate-rate student loans (depends on rate and stability)

- Mortgage last (often), because it’s usually lower-rate and tax/behavior math gets nuanced

If you want a clean head-to-head method, FIYR has a full breakdown in Debt Payoff Smackdown: Snowball vs. Avalanche.

Quotable truth: Debt payoff is investing, it just comes with fewer screenshots.

Boring Move #3: Automate the “wealth deposit” like it’s a bill

The best net worth builders don’t “decide” to invest every month.

They make it the default.

The boring automation stack

Pick one step you can set once and benefit forever:

- Auto-transfer to savings the day after payday

- Auto-invest into a diversified fund (in retirement or brokerage)

- Auto-increase contributions whenever income rises

This is especially critical if your life comes with irregular income, toddlers, a busy season, or a nervous system held together by cold brew.

And yes, the first dollars should often go to any employer match available. If your employer offers matching, that’s not a “perk.” That’s a raise you’re refusing.

Where people mess this up: they automate everything except the part where money actually moves to “Future You.”

Quotable truth: If saving requires weekly heroism, it’s not a plan, it’s fan fiction.

Boring Move #4: Fix the Big Three (because lattes aren’t your problem)

You can absolutely cut small leaks. You should.

But net worth takes off when you address the Big Three:

- Housing

- Transportation

- Food (especially convenience food)

These are the categories that can swing your savings rate by 10 points without you becoming a monk.

Here’s what this looks like in practice.

The “One Change, Big Impact” table

These are examples, not commandments. The goal is to find one move that creates breathing room.

| Big lever | Example boring move | Why it works | What net worth hears |

|---|---|---|---|

| Housing | Refinance (if it makes sense), house-hack, negotiate rent, downsize, get roommates for a season | Housing is usually the biggest fixed cost | “More fuel every month” |

| Transportation | Keep the paid-off car longer, buy used, reduce insurance, stop upgrading like it’s a personality | Car payments quietly eat futures | “Less drag, more investing” |

| Food | Cap delivery, batch cook 2 meals/week, build a convenience budget (on purpose) | Convenience spending is the stealth tax of adulthood | “Same life, fewer leaks” |

Now the fun part: translating boring savings into net worth.

If you free up $500/month and invest it for 10 years at an assumed 7% average annual return, you end up with roughly $80k to $90k (ballpark, returns vary).

That’s not a latte.

That’s a car.

That’s “I can breathe.”

That’s “I have options.”

Boring Move #5: Increase income, but do it like a grown-up

There are two ways to grow net worth:

- Spend less than you earn

- Earn more than you spend

One of these scales better.

Spending cuts have a floor. Income has (for many careers) a much higher ceiling.

A realistic income-growth playbook

This is not “start a dropshipping empire.” This is “make more money with fewer delusions.”

- Ask for the raise with receipts: track wins, quantify impact, set the meeting

- Switch jobs strategically: the market often pays more for new hires than loyalty

- Skill-stack: add one high-leverage skill (analytics, sales, automation, project leadership)

- Add a boring side income: consulting, freelancing, seasonal work, niche services

If your income is irregular (freelancers, creators, commission folks), your strategy is the same but your system needs smoothing. Start with Budgeting With Irregular Income: A Practical System That Actually Works.

Quotable truth: Your paycheck is the seed capital for your freedom. Treat it like it matters.

Boring Move #6: Prevent lifestyle creep with one rule (and a little shame)

Lifestyle creep is when your spending grows to match your income, like it has a personal vendetta.

You get a raise. Then you “deserve” upgrades. Then you’re somehow still stressed.

A clean anti-creep rule:

When income goes up, automatically divert 50% of the increase to investing or debt payoff for 6 months.Not forever. Just long enough to lock in progress before your brain starts pricing in a new normal.

If you want a deeper playbook, FIYR has it covered in How to Avoid Lifestyle Creep in 2026 (And Start Saving More).

Quotable truth: Lifestyle creep is inflation you personally subscribed to.

The “Boring Wins” system: weekly, monthly, quarterly

Net worth growth is not one giant decision. It’s a rhythm.

And the rhythm needs to be simple enough that you can do it during a busy week, not just during your annual “I’m getting my life together” mood.

Weekly (15 minutes): the Money Pulse Check

- Review your top spending categories

- Confirm bills and subscriptions did what they always do (and didn’t multiply)

- Tag any weird spending with a label like “Trip,” “Car Repair,” or “Life Happened” so your budget doesn’t gaslight you later

Monthly (30 minutes): the Net Worth Close

- Reconcile any “Needs Review” transactions

- Update key balances (or verify synced data)

- Check: did your net worth increase because you saved/invested, or just because markets went up?

Quarterly (45 minutes): the Boring Growth Audit

- Raise one cap, lower one cap (based on reality)

- Increase one automation (savings, investing, debt payoff)

- Kill one recurring expense you do not love

How FIYR makes boring net worth growth way easier

Most apps are good at showing you charts. Fewer are good at helping you run a system.

FIYR is designed for people who want net worth growth without turning their life into a spreadsheet cosplay. In practice, that means:

- Net worth tracking that includes both assets and liabilities

- Income and expense tracking with clean category control

- Custom categories, labels, and category groups so your data matches your life (not the other way around)

- Automatic transaction rules to keep tracking from becoming a second job

- Subscription tracking to catch the creeping monthly nonsense

- Savings rate tracking and FIRE projections so net worth connects to a real timeline

- Goal tracking with a safe-to-spend number so you can make decisions without guessing

And if you are a former Mint user, this is the vibe shift: less “generic defaults,” more “tell the truth, then build the plan.”

Frequently Asked Questions

What are the best net worth growth strategies if I’m starting from scratch? Start with accurate tracking, a starter emergency fund, high-interest debt payoff, and one automated savings or investing transfer. The first win is control. Should I invest or pay off debt first to grow net worth faster? If the debt is high-interest (often credit cards), paying it off is usually the best guaranteed return you can get. Moderate or low-interest debt can be more situational. How often should I track net worth? Monthly is the sweet spot for most people. Weekly is overkill and turns normal volatility into emotional damage. Why is my net worth not growing even though I’m saving? Common causes include missing liabilities, irregular “true expenses,” lifestyle creep, or savings sitting in cash instead of being invested (based on your risk tolerance and timeline). Does net worth include my house? It can, but be conservative. Use a realistic estimate and remember to subtract the mortgage. Net worth is a planning tool, not a bragging contest. What’s the fastest way to increase net worth in a year? For many households: stop negative compounding (high-interest debt), reduce one big fixed cost, and automate investing so progress happens without willpower.Your move: pick one boring strategy and make it automatic

If you try to do all of this at once, you will do none of it, then blame “discipline,” then download another app, then repeat.

Instead, pick one boring move that wins:

- Automate a weekly transfer

- Kill a high-interest balance

- Cut one fixed cost

- Audit subscriptions

- Run a monthly net worth close

Then make it easier to repeat.

If you want a clean way to track net worth, spending, subscriptions, savings rate, and your path to FIRE without living inside a spreadsheet, try FIYR: https://blog.fiyr.app.

Because the truth is simple: boring money moves aren’t boring when they buy you your life back.