How to Reduce Expenses by 20 Percent Without Feeling Poor

Most people don’t need “discipline.” They need receipts.

Because the uncomfortable truth is this: you can feel broke while spending like a small nation-state.

And if you want to reduce expenses by 20 percent without feeling poor, you don’t need to move into a yurt and learn to love lentils. You need two things:

- A clean picture of where your money is actually going (not where you think it’s going).

- A system that cuts the low-joy spending first, and locks in the wins.

Also, you’re not imagining the stress. According to a CNBC report, 60% of Americans live paycheck to paycheck, around 70% feel stressed about money, and 61% carry credit card debt with an average balance of $5,875. That’s not “bad at budgeting.” That’s modern life with subscription creep and inflation seasoning your bank account like a brisket.

Here’s the game plan.

Step 0: What “20%” actually means (and why it feels impossible)

Cutting 20% sounds like a motivational poster until you do the math.

Meet Jordan. Normal person. Normal chaos.

- Take-home pay: $5,000/month

- Expenses: $4,700/month

- “Savings”: $300/month (aka “whatever’s left after life happens”)

A 20% expense reduction is $940/month. That’s not “skip one latte.” That’s “find a new rent payment hiding in your current lifestyle.”

Here’s the part nobody talks about: 20% is rarely one giant cut. It’s usually a stack of medium wins that don’t ruin your day.

| Target | If your monthly spending is… | 20% reduction equals… |

|---|---|---|

| Small win | $3,000 | $600/month |

| Solid | $4,000 | $800/month |

| Serious | $5,000 | $1,000/month |

| “Okay, we’re doing this” | $6,000 | $1,200/month |

The goal isn’t deprivation. The goal is reallocating: less money to “meh,” more money to your goals, your peace, and your future self.

Memorable takeaway: You don’t need to feel poor. You need to stop funding stuff you don’t even like.

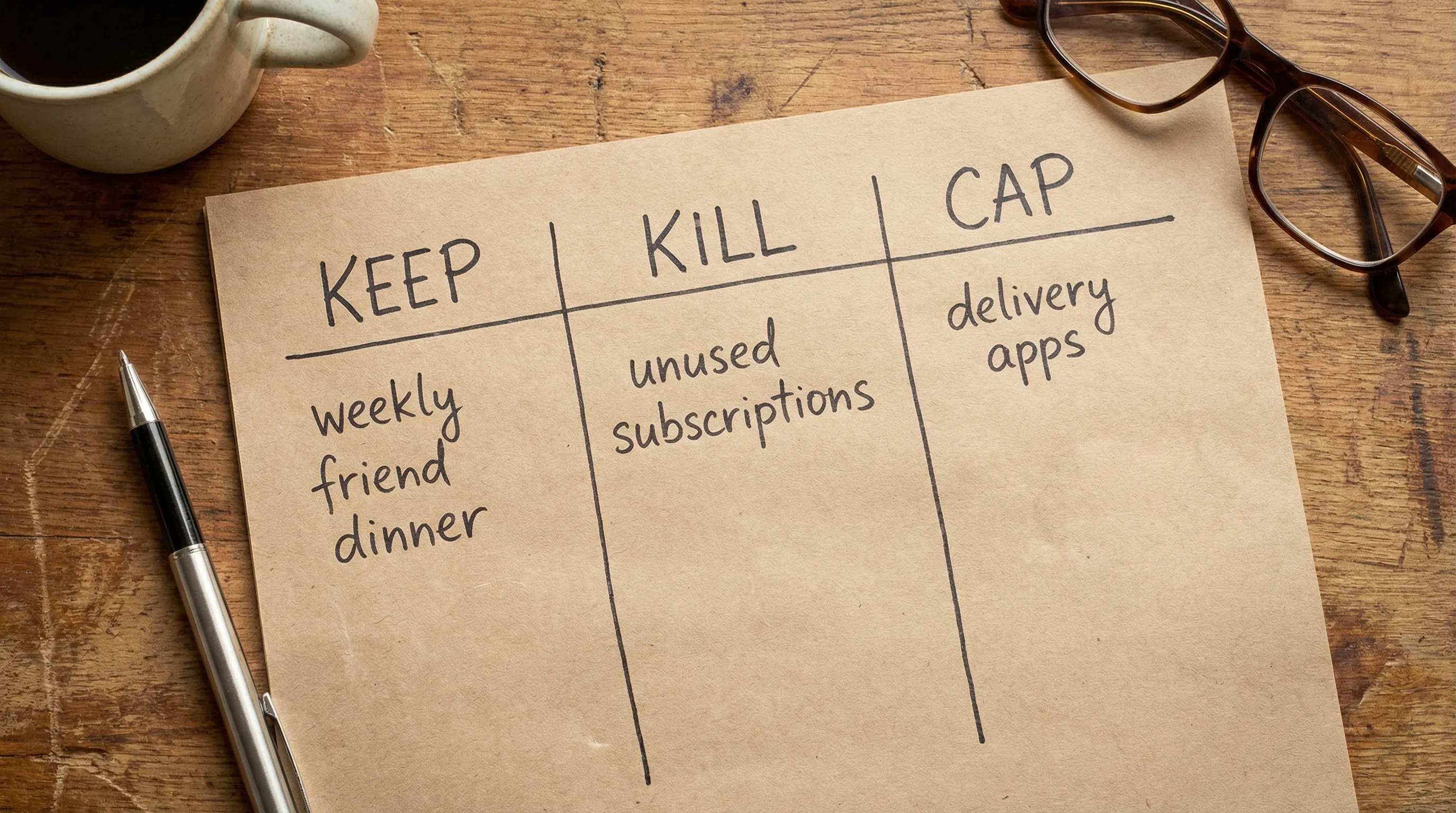

The “Keep, Kill, Cap” framework (aka cutting without sadness)

If you cut randomly, you’ll feel punished. If you cut strategically, you’ll feel powerful.

Use this simple filter for every spending category:

- Keep: High joy, high value, or genuinely life-supporting.

- Kill: Low joy, low value, mostly habit, mostly convenience.

- Cap: You like it, but it loves to quietly multiply.

Your “Keep” categories are how you avoid feeling poor.

Jordan’s Keep list might be:

- Gym membership (because mental health is not optional)

- One weekly dinner with friends

- Travel fund (because life is not a spreadsheet)

Then Jordan kills or caps the boring villains.

Your 15-minute setup

Pull your last 30 to 60 days of transactions and do a fast classification pass. If you use a modern tracker (like FIYR), this is easier because you can clean categories, create labels (like “NYC Trip 2025”), and stop lying to yourself with one giant “Shopping” bucket.

If you’re coming from Mint, or you’re comparing tools like Monarch, Copilot, Rocket Money, or Quicken, the point is the same: your categories must map to decisions.

If you want a clean tracking setup, start with Automatic Expense Tracking: Set It Up Once, Benefit Forever.

Where the easiest 20% usually hides (hint: it’s not your toothpaste)

There are two ways to cut spending:

- Small cuts everywhere (annoying, fragile, high willpower)

- Medium cuts in the biggest buckets (boring, effective, repeatable)

We’re doing #2.

Lever 1: Housing, the main character of your budget

If you want a 20% cut, your fixed costs need to feel a little bit of heat.

No, you don’t need to live under a bridge. But housing is often your biggest line item, which makes it the highest-leverage place to negotiate, restructure, or rethink.

Try one of these:

- Renegotiate at renewal: Ask for a longer lease term in exchange for a lower monthly rate. Worst case, they say no and you still live there.

- Rent-competition audit: Pull 3 comps in your area. If you’re paying above market, you have leverage.

- House-hack lite: Short-term roommate, travel nurse rental, or renting parking/storage if allowed.

- Refinance or recast (homeowners): Not always attractive in 2026 rate reality, but worth checking if your situation changed.

Quick script (edit to fit your personality):

“I’d like to renew, but the new rate is above what I’m seeing for comparable units. If I sign for 12 to 18 months, can we adjust the rent to $X? I’m a low-maintenance tenant and I pay on time.”

Memorable takeaway: Housing isn’t sacred. It’s negotiable, adjustable, or replaceable.

Lever 2: Transportation, aka the “I deserve this” tax

Cars are emotional support animals with APRs.

Transportation cuts that don’t feel like poverty:

- Insurance re-quote: People overpay for inertia. Get competing quotes. Raise deductibles if your emergency fund can handle it.

- Drive less on purpose: Bundle errands. Fewer trips = fewer impulse stops.

- Downgrade the payment, not your dignity: If you’re financing a car that eats your cash flow, a boring used car can buy back years of freedom.

- Kill rideshare drift: Cap it. Rideshare is a convenience tool, not a personality.

If you’re paying interest on a car and carrying credit card debt, you’re not “building a life.” You’re running a donation program to lenders.

Lever 3: Food, the sneakiest lifestyle creep

Groceries went up, sure. But the real villain is the “I’m tired” economy.

The goal isn’t ramen. The goal is a default plan that reduces decision fatigue.

Try this trio:

- Two home-cooked anchor dinners per week you can make on autopilot.

- One convenience allowance (delivery or takeout) that is planned, not guilt-driven.

- A grocery rule: If it goes bad before you eat it, stop buying it.

Capping convenience spending is basically buying back your own money from the algorithm.

Memorable takeaway: You don’t have a food budget problem. You have a “what’s the plan at 6:17 pm” problem.

The invisible 20%: subscriptions, fees, and financial “dust”

This is where money disappears quietly, like a magician who only steals from you.

Subscription creep (aka “Who signed me up for this?”)

Most people don’t cancel subscriptions. They “mean to.” For six months. Then they die with three streaming services and a meditation app they used once while spiraling.

Do a 30-minute audit:

- Identify every recurring charge.

- Sort into Keep, Rotate, Cancel.

- Set a hard monthly cap.

If you want a full workflow, use Reduce Subscriptions in 2026: A 30-Minute Cleanup Plan or the deeper playbook Subscription Overload Solutions: Cut the Noise, Keep the Joy.

In FIYR, subscription tracking helps you spot the repeat offenders so you’re not playing detective with your own bank statement.

Fees and interest, the “anti-wealth” category

Fees are the most insulting expense because they buy you nothing except regret.

Common leaks to hunt:

| Leak | What it looks like | Fix that doesn’t hurt |

|---|---|---|

| Credit card interest | Carrying a balance “for a bit” | Shift to a payoff plan, cut spending to stop new debt first |

| Bank fees | Monthly maintenance, overdrafts | Switch account type, set alerts, keep a buffer |

| Late fees | Forgetting due dates | Autopay minimums, calendar reminders |

| “Convenience” charges | Delivery, ticketing, rush shipping | Cap it, batch purchases, default to slow shipping |

If you’re paying high-interest debt, the best expense reduction is often a payoff strategy. (It’s hard to build wealth when your APR is speedrunning your paycheck.)

The real trick: don’t just cut, lock it in

Most budgets fail because they’re a vibe, not a system.

You cut a few things, you feel proud, you relax, and then a random Tuesday happens and you’re back to spending like you’re being audited by your future self.

To reduce expenses by 20 percent and keep them down, you need a firewall.

The 20% Firewall (simple, slightly ruthless)

Rule 1: Set caps on your “Cap” categories.Not “spend less.” A number. A guardrail.

Rule 2: Route the savings automatically.If you don’t move the money, it will mysteriously become “fun money” because your checking account is basically a yes-man.

Rule 3: Weekly review, 15 minutes, no drama.This is where you catch drift early. It’s easier to correct a small leak than to rebuild a ship.

If you want the “why budgets fail” diagnosis (and the fix), read Why Budgets Fail (And How to Fix Yours in 2026).

How FIYR makes the firewall easier (without turning into your boss)

The faster you can see reality, the less you need willpower.

FIYR helps by:

- Tracking income and expenses in one place

- Letting you create custom categories that match your real decisions

- Using transaction rules so categorization doesn’t become a second job

- Highlighting subscriptions so recurring charges don’t hide

- Showing your savings rate, net worth, and FIRE trajectory so you remember why you’re doing this

It’s a modern alternative to Mint-style budgeting, but with more flexibility and less “why is this categorized as Pets?” energy.

If you’re rebuilding your setup from scratch, Custom Budget Setup in 30 Minutes pairs well with this whole 20% mission.

A 7-day sprint to cut 20% (without turning into a spreadsheet goblin)

This is intentionally fast. Momentum matters.

- Day 1: Baseline reality. Pull the last 30 to 90 days of spending. No shame, just data.

- Day 2: Keep, Kill, Cap. Protect 2 to 3 Keep categories, pick 3 Kill targets, cap 2 categories that creep.

- Day 3: Subscription sweep. Cancel or rotate at least 2 recurring charges.

- Day 4: Negotiate one bill. Internet, insurance, phone plan, anything with a customer service line.

- Day 5: Convenience cap. Set one rule for delivery, rideshare, or impulse spending.

- Day 6: Lock the savings. Auto-transfer the difference the day after payday.

- Day 7: Install the weekly review. Put it on your calendar. Make it boring. Boring is undefeated.

Memorable takeaway: Your goal is not a perfect month. Your goal is a repeatable month.

Frequently Asked Questions

Is it realistic to reduce expenses by 20 percent quickly? Yes, if your spending has obvious leaks (subscriptions, fees, convenience spend) or big negotiables (insurance, housing, car). If your budget is already tight, you may need a longer runway or an income boost alongside cuts. What if cutting expenses makes me feel deprived? You’re probably cutting randomly. Protect 2 to 3 “Keep” categories that make life feel good, then cut low-joy spending hard. Deprivation usually comes from killing joy, not killing waste. What expenses should I cut first to hit 20%? Start with recurring waste and big levers: subscriptions, insurance, transportation, housing, and convenience food. Small cuts everywhere tend to fail because they rely on constant restraint. How do I make sure the savings don’t disappear? Automate the win. Set category caps, then route the saved amount into a goal or savings account automatically right after payday. If it stays in checking, it will get adopted by your next impulse purchase. Do I need a budgeting app to do this? No, but it helps. The fastest path is clean tracking, clear categories, and a weekly review rhythm. Tools like FIYR make that process less manual and more consistent, especially if you’re coming from Mint or juggling multiple accounts.Your next move (because motivation is cute, systems are better)

If you want to reduce expenses by 20 percent without feeling poor, stop aiming for “frugal.” Aim for intentional.

Track the truth, protect what you love, cut what you don’t, and automate the difference.

When you’re ready to make this easier (and less manual), explore FIYR on the blog and start with the tracking foundation: Automatic Expense Tracking: Set It Up Once, Benefit Forever.

Because the fastest way to feel richer isn’t earning more. It’s stopping the silent spending you don’t even remember agreeing to.