Coast FIRE: How It Works and Who It’s Best For

Most people think early retirement means ramen noodles and a spreadsheet-induced migraine. Here is the plot twist, you can stop saving for retirement in your 30s or 40s and still retire on schedule if you hit one number early. That is Coast FIRE, and it is as much psychology as math.

Quick reality check. Money stress is the default setting. One widely cited report found that about 60 percent of Americans live paycheck to paycheck, which makes long-term saving feel like science fiction. Source, CNBC. Coast FIRE is an antidote that uses front-loaded investing and compound growth to put your future on autopilot.

What is Coast FIRE, exactly?

Coast FIRE is the point where your existing investments, without any new retirement contributions, are projected to grow to your Financial Independence number by your target retire age. You still work and cover your living expenses, you just stop feeding the retirement accounts once you hit your Coast number.- You are not withdrawing yet, that would be Barista FIRE or full FIRE.

- You are not “done,” you are on glide path. The market does the heavy lifting while you live your life, switch careers, start a business, take a lower-stress role, or simply buy back time.

If you want the full backdrop on withdrawal math, see our guide on the 4% rule.

Why early savings do the heavy lifting

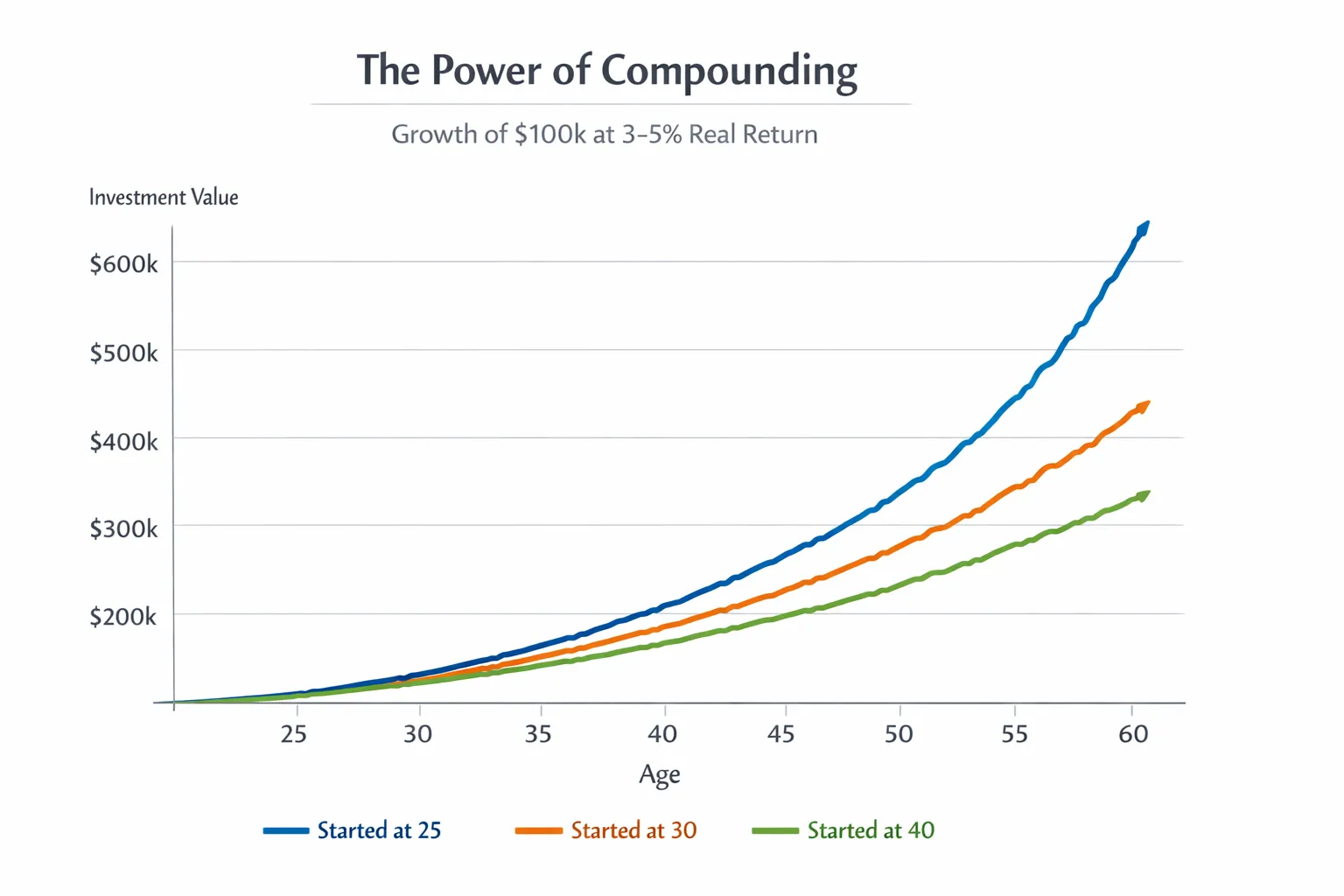

Compounding pays the people who show up early. A dollar invested in your 20s has decades to double, then double again. A dollar invested in your 40s is on a tight deadline.

- Invest 100,000 at age 30 and let it grow at a 4 percent real return, roughly inflation-adjusted, until 60. You get about 324,000.

- Invest that same 100,000 at age 40 to 60 at 4 percent real. You get about 219,000.

Same money, different start date, six figures of difference. Early dollars are louder than late dollars.

The math, a dead-simple Coast FIRE calculation

Here is the clean version. Your FI number is your expected annual spending in retirement times 25, which mirrors a 4 percent withdrawal rate in today’s dollars. Your Coast number is the amount you need invested today so that, with no new contributions, you land on your FI number by your chosen retire age.

- FI number, spending × 25

- Coast number today, FI number ÷ (1 + r)^n

Where r is your assumed real return, and n is years until retirement. Real means after inflation, so the dollars make sense in today’s terms.

Walk-through example

- Age, 30

- Target retire age, 60, so n = 30 years

- Planned spending in retirement, 40,000 per year

- FI number, 40,000 × 25 = 1,000,000

- Assume 4 percent real return

- Coast number today, 1,000,000 ÷ 1.04^30 ≈ 1,000,000 ÷ 3.243 ≈ 308,000

Translation, if a 30-year-old already has about 308,000 invested, they could set retirement contributions to zero, keep covering their living costs with work, and still arrive around 1 million at 60 in today’s dollars. No heroics required, just time.

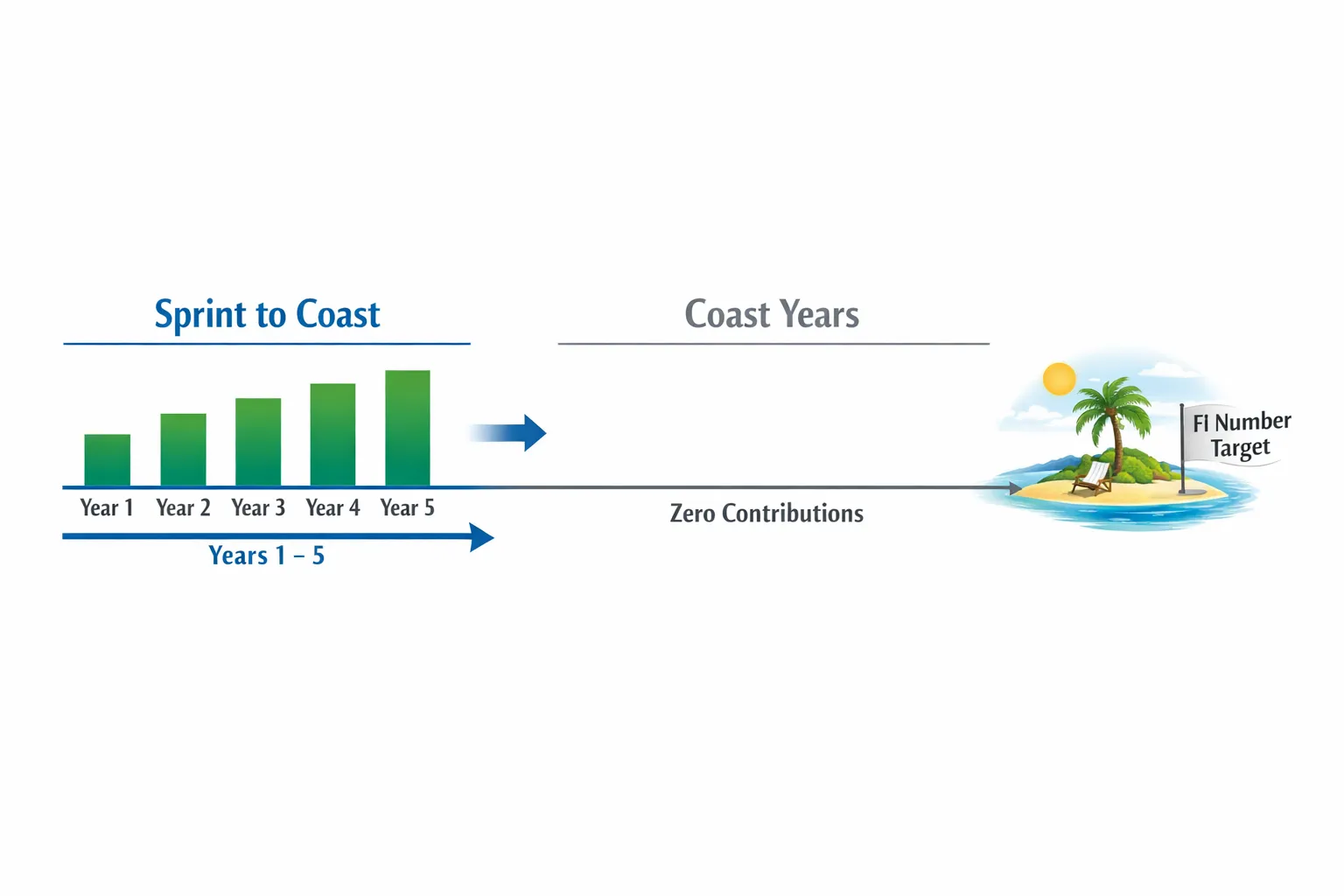

Here is the part nobody talks about, if you are not at your Coast number yet, you can set a Coast date. You aim to hit your Coast balance in a few years, then stop contributing.

- Same person, has 120,000 today, wants to hit Coast by 35.

- At 35, the years to 60 drop to 25, so the required Coast-at-35 balance is 1,000,000 ÷ 1.04^25 ≈ 375,000.

- Required annual contribution for 5 years, about 42,300 per year, roughly 3,525 per month, at 4 percent real.

That is a sprint, then a lifetime jog.

Pro tip, model a range of real returns, 3 to 5 percent is a practical band. Lower returns mean a higher Coast number, higher returns mean a lower Coast number. We show both in the scenarios below.

Sample Coast FIRE scenarios

All examples use the 4 percent rule for the FI number and a 4 percent real return for the Coast number, rounded.

| Scenario | Age now | Annual spend today | Target retire age | Years to go | FI number, 25× spend | Coast number now, 4% real |

|---|---|---|---|---|---|---|

| Early starter | 25 | 36,000 | 60 | 35 | 900,000 | 228,000 |

| Solid saver | 30 | 40,000 | 60 | 30 | 1,000,000 | 308,000 |

| Mid-career | 35 | 50,000 | 60 | 25 | 1,250,000 | 469,000 |

| Late pivot | 45 | 60,000 | 60 | 15 | 1,500,000 | 833,000 |

Sensitivity for the 30-year-old example, Coast number today for different real returns:

- 3 percent real, about 412,000

- 4 percent real, about 308,000

- 5 percent real, about 231,000

Key takeaway, the earlier you start and the lower your planned spend, the more attainable Coast FIRE becomes.

Who Coast FIRE is best for

- People in their 20s or early 30s who can front-load savings for 3 to 7 years, then coast.

- Career switchers who want freedom to take a lower-paying, higher-purpose job later.

- Parents who want to free up cash flow during the kid-heavy years without sacrificing retirement.

- Entrepreneurs who want to reduce fixed savings obligations while they build a business.

- Anyone who prefers long-term peace over short-term flex, the quiet power crowd.

Who it is not ideal for, people starting very late with high planned spending, or those who cannot cover living expenses without dipping into investments yet. If you want partial withdrawals earlier, read our guide to Barista FIRE.

Risks, myths, and guardrails

- Markets can underperform, use conservative assumptions and add a margin of safety, 10 to 30 percent buffer above your Coast number helps.

- Lifestyle creep is the silent killer, if spending rises, your FI number goes up and your coast plan breaks. Keep a lid on fixed costs.

- Employer match is real money, even if you coast, consider at least contributing to capture free match.

- Healthcare and taxes still matter, build those into your cash-flow plan.

- You still need an emergency fund, see our emergency fund guide so you do not raid investments when life happens.

Quote it, front-load the pain, back-load the freedom.

A five-step system to reach Coast FIRE

- Define your target spend in retirement, start with your current annual spend, subtract work-only costs, then sanity check against your desired lifestyle.

- Pick a target retire age, 55, 60, or 65, earlier targets mean higher Coast numbers.

- Choose a conservative real return assumption, plan with 3 to 4 percent real. This keeps your math in today’s dollars.

- Do the math, FI number = spend × 25. Coast number today = FI number ÷ (1 + r)^n. If you want to hit Coast by a future date, compute the required balance for that date, then solve for annual contributions:

PMT ≈ [FV − PV × (1 + r)^n] × r ÷ [(1 + r)^n − 1]

- Automate a 3 to 7 year sprint, push contributions to hit your Coast date, then pivot to maintenance mode where work covers living costs and investments coast.

Make it easier with FIYR, the modern FIRE-friendly tracker

Coast FIRE is simple in theory, but the execution lives or dies on your system. FIYR keeps the numbers honest and the habits light.

- Track income, expenses, and your true savings rate automatically, then route cash to the Coast sprint. See our guide on boosting your savings rate.

- Build customizable budgets with smart caps and a dynamic safe-to-spend balance so your month does not swing like a crypto chart.

- Set a labeled goal, Coast Fund, and monitor progress with net worth tracking and FIRE projections.

- Use subscription tracking to claw back cash from sneaky renewals, if you want specific tools, we reviewed the best apps to manage subscriptions, and FIYR bakes this into your budget.

- Model alternatives, Lean versus Fat versus Barista, start with our Lean vs Fat FIRE comparison to see how lifestyle choices move your Coast number.

Light pitch, heavy relief. FIYR is designed for people who want not just a budget, but mastery of their financial life.

The bottom line

Coast FIRE is financial aikido, you use the market’s momentum to do most of the work. Front-load your investing, hit your Coast number, then redirect energy to the life you actually want. The earlier you start, the less heroic you need to be. That is not lazy, that is leverage.

If you can sprint for a few years, you can coast for decades. Your future self will send a thank you note, probably from a weekday afternoon with no meetings.