Budgeting for New Parents: Diapers, Debt, and Sanity

A baby doesn’t just steal your sleep.

It also moves into your budget, starts ordering things from Amazon at 2 a.m., and contributes exactly $0 to rent.

If you’re a new parent staring at your bank account like it’s a crime scene, you’re not alone. CNBC reported that around 60% of Americans are living paycheck to paycheck, and money stress is basically America’s second national language.

Now add diapers, childcare, medical bills, and a sudden obsession with “organic, non-toxic, Montessori-adjacent” everything. Congrats, you’ve unlocked Hard Mode.

Meet Jess and Malik. They had a “pretty solid” budget pre-baby. Then parental leave hit, income dipped, takeout spiked, and they discovered three new recurring charges:

- A diaper subscription they forgot they started.

- A “sleep sound” app they hate but fear canceling.

- Two streaming services, because 3 a.m. feeding sessions turn you into a content goblin.

Their problem wasn’t discipline. It was that their budget was still living in the Before Times.

Here’s how to rebuild a budget for new parents that covers diapers, debt, and sanity, without turning your relationship into a monthly spreadsheet cage match.

The three money shocks nobody warns you about

1) Your income can wobble (right when your expenses spike)

Parental leave, unpaid time off, reduced hours, childcare transitions, medical appointments. Even if you planned for it, cash flow gets weird.

And cash flow weirdness is where good budgets go to die.

One-liner to remember: Your paycheck didn’t get lazy, your life got expensive.2) Baby costs are not just “baby costs”

Yes, there’s the obvious stuff (diapers, formula, clothes). But the stealth category is “convenience spending,” because exhausted people will happily pay $18 to avoid one more decision.

This shows up as:

- Delivery fees

- Extra grocery runs

- Pharmacy runs for mystery baby needs

- “We deserve a treat” spending (you do, but you still need a lane for it)

3) Your brain is now running on 14% battery

Budgets fail when they require constant attention. New parenthood is the ultimate attention tax.

So the goal is not a perfect budget.

It’s a budget that still works when you’re holding a crying burrito human.

One-liner to remember: Willpower is not a financial plan, especially on four hours of sleep.The New Parent Budget Blueprint (simple, realistic, repeatable)

This is a “systems over vibes” approach. You’ll set up a few smart buckets, add guardrails, then let automation and quick check-ins do the heavy lifting.

Step 1: Build your “Post-Baby Baseline” from real data

Your first move is not guessing. It’s pulling your last 30 to 90 days of transactions and asking: what are we actually spending now?

If you’re using a modern tracker like FIYR, this is where it shines. You can see income, expenses, and category totals cleanly, then adjust as your routine changes.

Do one quick pass and label transactions into three groups:

- Old life (pre-baby habits that might be fading)

- New essentials (diapers, medical, childcare)

- New convenience (delivery, impulse buys, “please let this work” gadgets)

That third bucket is where budgets go to get mugged.

Step 2: Use categories that match your new reality (not your old spreadsheet)

Most new parents under-budget because their categories are too generic. “Baby” is not a category, it’s a universe.

Create categories that are emotionally obvious at a glance. If you have to debate where a transaction goes, your system is too fancy.

Here’s a clean starting point.

| Category group | What goes in it | Why it matters |

|---|---|---|

| Diapers + wipes | Diapers, wipes, diaper cream | Frequent, predictable, easy to track |

| Feeding | Formula, breastfeeding supplies, bottles, baby food | Can swing wildly month to month |

| Medical | Copays, prescriptions, therapy, OTC | Spiky costs that create “surprise” stress |

| Childcare | Daycare, nanny, babysitting | Often the biggest new line item |

| Baby gear | Stroller accessories, car seat upgrades, replacements | One-time costs that pretend to be “emergencies” |

| Convenience food | Delivery, premade meals, extra coffee | Exhaustion tax, budget needs a lane |

| Parent essentials | Postpartum needs, clothes, work return items | Often ignored, always real |

In FIYR, you can make custom categories and category groups, so you’re not trapped in someone else’s idea of what “family” spending looks like.

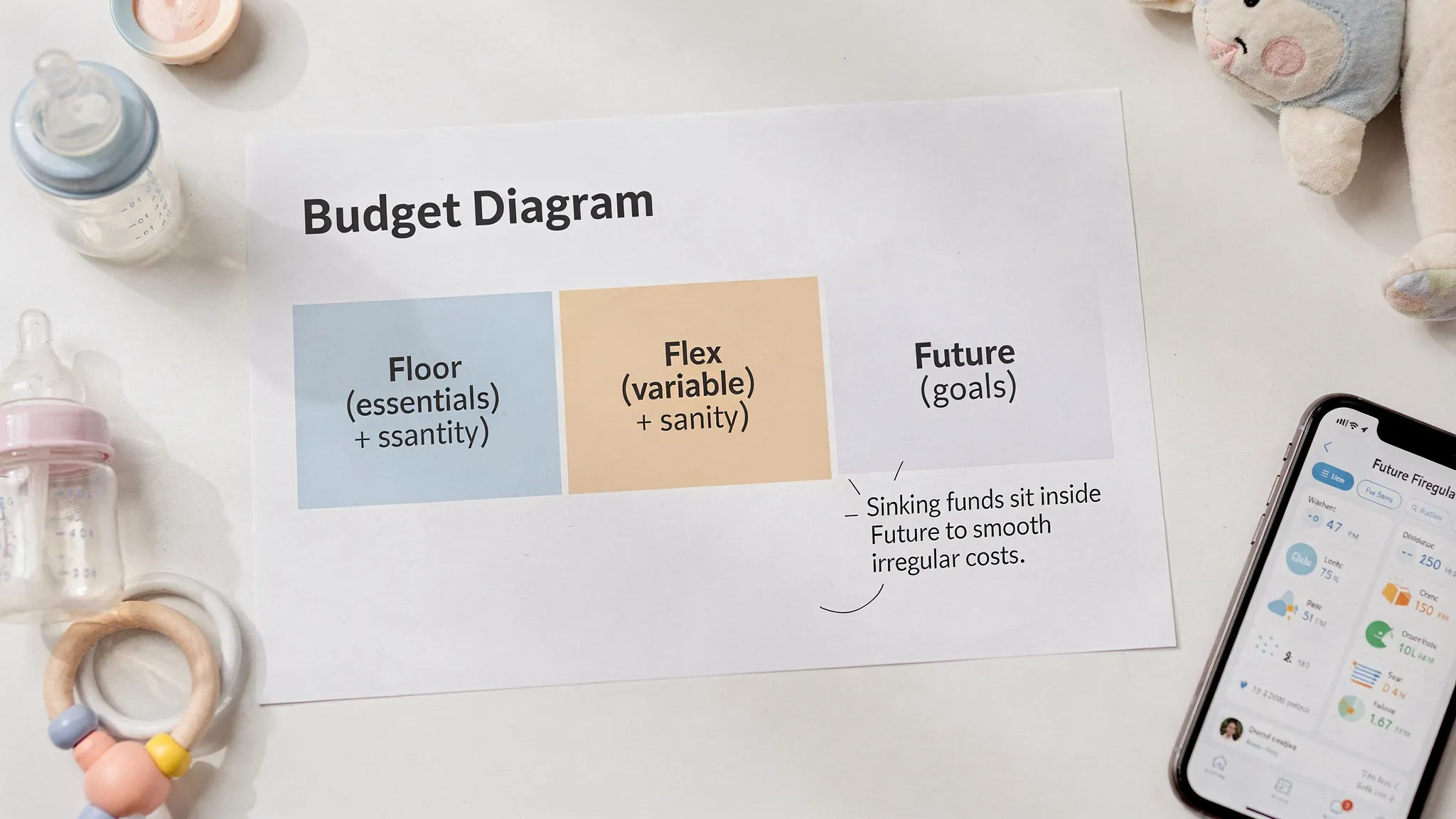

One-liner to remember: The right category names reduce guilt and increase clarity.Step 3: Switch to a “Floor, Flex, Future” budget (because babies hate spreadsheets)

New parent budgets fail when they’re too rigid. You need a budget that bends.

Use three layers:

#### The Floor (non-negotiables)

This is survival. Bills, groceries, minimum debt payments, insurance, diapers, basic transport.

If income dips (leave, job change, childcare shock), you protect the Floor first.

#### The Flex (variable essentials + sanity spending)

This includes groceries (beyond basics), convenience food, kid stuff that fluctuates, small fun.

Flex is where you add caps so spending doesn’t quietly expand like a gas.

#### The Future (goals)

Emergency fund, debt payoff beyond minimums, investing, sinking funds, FIRE goals.

If you’re FIRE-minded, the Future bucket is your identity. You don’t need to max everything right now, but you do need to keep the habit alive.

If you want a deeper version of this flexible approach, FIYR has a full guide on building budgets that don’t snap under pressure in Flexible Budgeting: Build a System That Bends.

One-liner to remember: Babies are variable, your system shouldn’t be brittle.Step 4: Do the parental leave math (without getting fancy)

Here’s the only formula you need:

Leave Buffer Target = (Monthly Floor Expenses × months of leave) + medical bufferThe medical buffer is personal, but if you’re in the U.S., “random medical bills” is basically a subscription you didn’t ask for.

If you haven’t built this yet, don’t spiral. Start with something.

A solid next step is building or rebuilding your emergency fund using a structured plan like Building Your Emergency Fund: The Ultimate Safety Net.

Step 5: Add sinking funds for the stuff that is predictable (but never feels predictable)

New parents get wrecked by “non-monthly monthly” expenses. Stuff that happens every few months, then shows up like a jump scare.

Examples:

- Daycare deposit and registration fees

- Annual subscriptions (hello, photo storage)

- Car seat replacements or upgrades

- Travel to see family

- Holiday gifting (yes, even when you swear you’ll keep it small)

Create a sinking fund category for each. Contribute monthly. Let time do its job.

In FIYR, you can track these as goals (and keep a safe-to-spend balance that reflects reality, not optimism).

One-liner to remember: If it happens every year, it’s not a surprise, it’s a subscription with bad branding.Diapers, debt, and the “don’t ruin your life” order of operations

New parenthood is where debt can quietly metastasize. Especially credit cards, because they make every emergency feel “manageable,” right up until the APR kicks you in the teeth.

Per the same CNBC coverage, 61% of Americans are in credit card debt, and the average balance cited was $5,875. That’s not a moral failing. That’s the cost of modern life plus frictionless spending.

Here’s a practical priority order for new parents:

1) Keep cash flow stable

Autopay minimums. Avoid late fees. Stop the bleeding.

2) Get one small win (for momentum)

Pick one annoying balance and attack it for psychological relief. If you want the full strategic breakdown, FIYR covers the tradeoffs in Debt Payoff Smackdown: Snowball vs. Avalanche.

3) Then go full “math mode”

Once you have traction, focus extra payments where interest is highest, especially on credit cards.

4) Keep the FIRE habit alive (even if you downshift)

If you’re investing, consider maintaining at least the employer match if you have one (if applicable). The point is continuity.

One-liner to remember: Your baby doesn’t need you to be perfect, they need you to be solvent.The sanity system: make money decisions smaller and more frequent

Most budgets fail because people do one giant, painful monthly meeting that feels like a performance review.

Instead, do a tiny weekly check-in.

Call it the Stroller Walk Money Huddle:

- 10 minutes

- Same day each week

- Phones out, zero judgment

- One goal: stay aware

What you check:

- Safe-to-spend (what’s actually left)

- Top 3 categories this week

- Any weird subscriptions or duplicate charges

- One tiny action (cancel, cap, move $25 to a goal)

FIYR makes this easier because it’s built for quick visibility: spending totals, subscriptions, budgets, and savings rate, all in one place (without the legacy-tool clutter of old-school software).

One-liner to remember: Small money meetings prevent big money fights.The “New Parent Subscription Audit” (yes, you have more than you think)

New parents are prime targets for subscription creep. You start one free trial because you’re desperate, and two months later you’re paying for an app that shushes your phone.

Do a 15-minute audit:

- Find every recurring charge

- Cancel anything that solves a problem you no longer have

- Downgrade anything you’re “not using but might”

If you want a deeper playbook, see Best Apps to Manage Subscription Renewals.

In FIYR, subscription tracking helps you catch these before they become permanent residents in your budget.

One-liner to remember: Subscriptions are just tiny debts with better PR.

How FIYR fits into budgeting for new parents (without turning it into homework)

If you used Mint back in the day, you know the vibe: fine for a snapshot, not great for a life change.

New parenthood is the ultimate life change.

FIYR is useful here because it’s not just “a budget.” It’s a money operating system:

- Spending tracking so you can see the real post-baby baseline

- Custom categories so “Diapers + Wipes” isn’t stuck inside “Other” like a tax audit waiting to happen

- Automatic transaction rules so recurring baby expenses categorize themselves

- Subscription tracking because you will forget what you signed up for

- Net worth and liabilities tracking so debt and progress are visible, not vibes

- Savings rate + FIRE projections so you can see the impact of childcare years, then plan around it

And yes, it’s a modern alternative to Mint, Monarch Money, Copilot, Rocket Money, and Quicken, especially if you want flexibility and FIRE-friendly insight without drowning in menus.

One-liner to remember: The goal is less tracking time, and more control.Frequently Asked Questions

How much should I budget for a new baby each month? It varies wildly by feeding choices, childcare, and healthcare, but the better approach is to build categories (diapers, feeding, medical, childcare, gear, convenience) and then measure your real spending for 30 to 90 days. Your first budget should describe reality, not your hopes. How do we budget during parental leave with reduced income? Build a “Floor” budget first, then temporarily shrink Flex, and set a clear buffer target using: (Monthly Floor Expenses × months of leave) + a medical buffer. If you’re short, prioritize cash flow stability, then rebuild savings when income normalizes. What’s the best way to handle childcare costs in a budget? Treat childcare like housing: it’s a fixed, major line item that drives everything else. Set it as a dedicated category, plan for deposits and fee changes with a sinking fund, and revisit your overall savings rate so your long-term goals stay grounded. Should we pause investing or debt payoff when the baby arrives? Don’t use a baby as an excuse to ignore math, but also don’t pretend you’re a robot. Avoid high-interest debt growth, keep minimums on everything, and maintain at least one “Future” habit (even if smaller) so you don’t lose momentum. How do we avoid money fights as new parents? Make it boring. Do a 10-minute weekly check-in, agree on a couple category caps, and give each parent a small guilt-free personal spending lane. Predictability reduces conflict more than perfection ever will. ---Build a budget that survives the newborn phase

If your finances feel messier than your sleep schedule, you don’t need a stricter personality. You need a system that matches your life.

FIYR helps you track spending, set flexible budgets, catch subscriptions, and see your savings rate and net worth in one place, so you can stay on track without turning money into a second job.

Try it as your modern budgeting alternative to Mint, Monarch, Copilot, Rocket Money, or Quicken, and make “adulting with a baby” slightly less unhinged.

Get started here: FIYR