Budget Allocation 50/30/20: When It Works (and Fails)

The 50/30/20 rule is the budgeting equivalent of “just eat healthy.” Technically correct, emotionally satisfying, and wildly unhelpful the moment you walk into Costco hungry.

Still, budget allocation 50/30/20 has survived every personal finance trend cycle for a reason: it’s simple enough to use when your brain is fried, your kid is screaming, and your bank balance is doing that thing where it pretends rent isn’t coming.

But simplicity has a price. And in 2026, a lot of people are paying it.

According to CNBC, about 60% of Americans are living paycheck to paycheck and 61% are in credit card debt, with an average balance around $5,875. Only 45% report having an emergency fund, and many of those have under $5,000 saved (CNBC). In that environment, telling someone “just do 50/30/20” can be either a lifeline or a comedy sketch.

So let’s do the honest version: when 50/30/20 works, when it fails, and how to upgrade it without turning your life into a spreadsheet cult.

What the 50/30/20 rule actually means (and what it doesn’t)

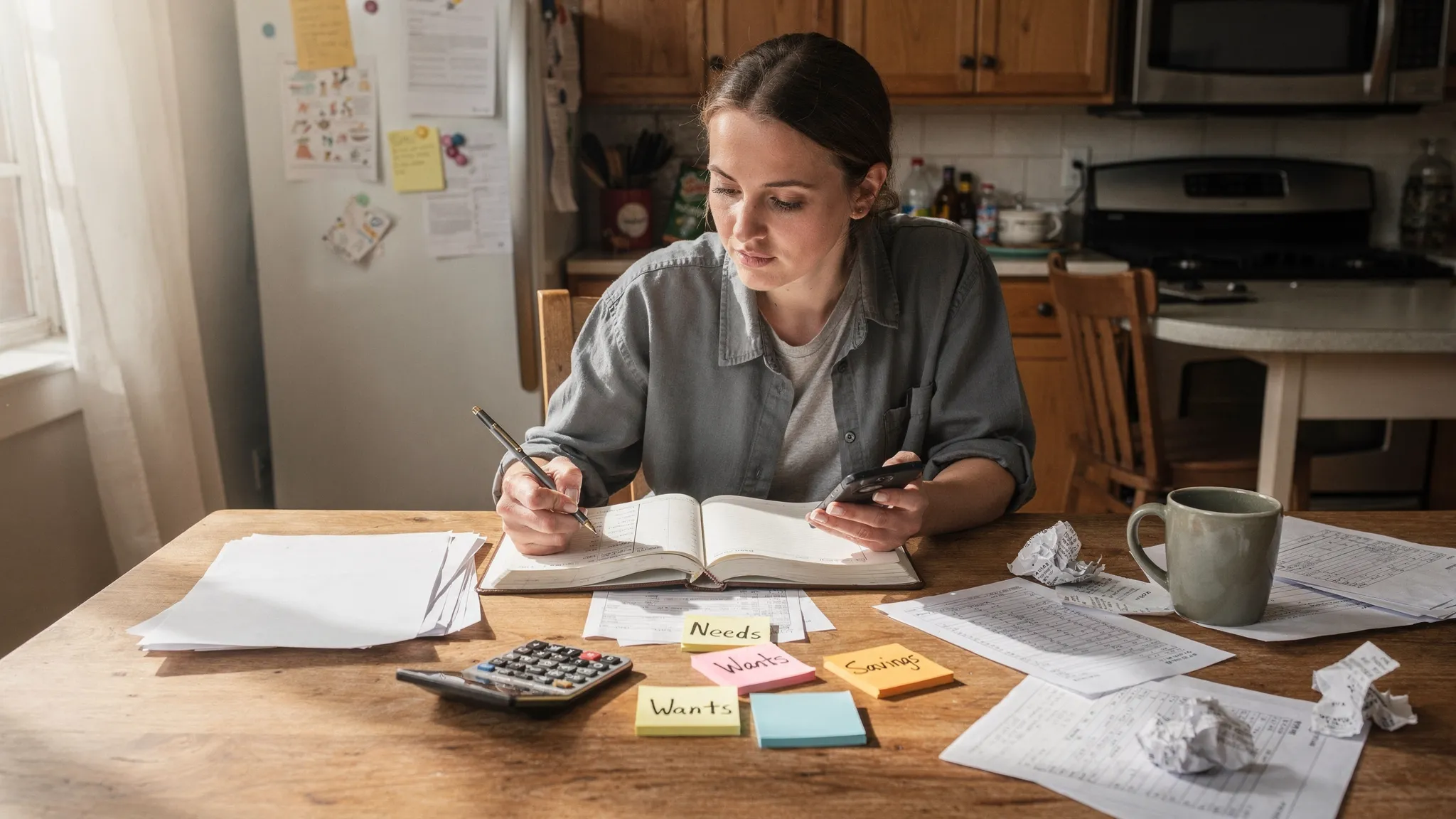

At its core:

- 50% Needs: housing, utilities, groceries, insurance, minimum debt payments, basic transportation

- 30% Wants: dining out, travel, shopping, entertainment, subscriptions that are not essential

- 20% Savings and debt payoff: emergency fund, retirement contributions, extra payments above minimums, investing

Two important clarifications people skip (then wonder why it “doesn’t work”):

1) It’s usually based on after-tax income

Most versions assume net pay (what actually lands in your account), not gross salary. If you’re budgeting off gross while payroll taxes and benefits quietly body-slam your paycheck, your percentages will feel cursed.

2) It’s a diagnostic, not a religion

50/30/20 is less “the right way” and more “a quick financial X-ray.” It tells you where your money is leaning, and where it’s breaking your spine.

Quotable truth: A budget rule is a tool. The moment it becomes a personality, it stops working.

Why 50/30/20 became famous (it’s not because math is sexy)

People love 50/30/20 because it does three things well:

- It reduces decision fatigue. You don’t have to argue with yourself about every line item.

- It gives you permission to enjoy money (the 30% wants bucket is basically “spend without spiraling”).

- It creates a built-in savings floor for people who otherwise “save whatever’s left” (aka: nothing).

Meet Marcus.

Marcus is a former Mint user. He downloads a modern tracker, feels responsible for 48 hours, then goes right back to vibes-based spending. When he finally tries 50/30/20, he’s shocked: he’s not “bad with money,” he’s just running a subscription museum and calling it entertainment.

That’s where 50/30/20 shines: it makes the invisible obvious.

Here’s the part nobody talks about: obvious doesn’t always mean fixable.

When budget allocation 50/30/20 works beautifully

50/30/20 works best when your life has three qualities: stable income, reasonable fixed costs, and no urgent financial fires.

It works if you have stable income and predictable bills

If you’re W-2, paid consistently, and your core expenses don’t swing like a crypto chart, 50/30/20 is a clean starting structure.

It works if your “needs” are actually near 50%

That typically means:

- Housing is not consuming your entire existence

- You’re not supporting multiple dependents on one income

- You’re not juggling high-interest debt minimums that eat the savings bucket alive

It works if your goal is “control and progress,” not “FIRE in 7 years”

If you’re building the habit of saving and paying yourself first, 20% is a strong target. For many households, getting to 20% is already elite.

To make it concrete, here’s what the rule looks like in dollars.

| Net monthly income | 50% Needs | 30% Wants | 20% Savings/debt payoff |

|---|---|---|---|

| $3,000 | $1,500 | $900 | $600 |

| $5,000 | $2,500 | $1,500 | $1,000 |

| $8,000 | $4,000 | $2,400 | $1,600 |

If those numbers feel plausible, congrats, 50/30/20 might fit your life instead of fighting it.

Quotable truth: A good budget feels like guardrails, not handcuffs.

Where 50/30/20 fails (and why it’s not your fault)

Let’s talk about the three failure modes. Not “oops I bought a latte” failures. Structural failures.

Failure #1: Your needs are not 50%, they’re 70%+

This is the most common reason people “can’t budget.” Not because they’re irresponsible, but because the math is ugly.

If your needs are 65% to 80%, your 30% wants bucket becomes mythical. Like Bigfoot. Everyone talks about it, nobody’s seen it.

Common causes:

- High housing costs (rent or mortgage)

- Childcare (the most expensive subscription you cannot cancel)

- Medical expenses

- Car payments + insurance spikes

- Student loans and minimum debt payments

What to do instead:

- Use 50/30/20 as a diagnostic, then adopt a transitional split like 65/20/15 or 70/15/15.

- Focus on stability first (emergency fund + killing high-interest debt), then widen “wants” later.

Quotable truth: You can’t “budget harder” out of a housing crisis.

Failure #2: You don’t agree on what’s a need vs a want

This is where budgets go to die.

One person says “gym membership is health.” The other says “your gym is called ‘the sidewalk.’” Someone calls DoorDash a need because they had a long day. Someone calls a $900 car payment a need because “reliability.”

Pro tip: the categories aren’t moral. They’re functional.

A clean way to define it:

- Needs: spending that keeps you housed, fed, insured, employed, and compliant with your minimum obligations

- Wants: spending that improves lifestyle but can be reduced without immediate fallout

If you want to end the debate fast, use this litmus test:

If you lost your income tomorrow, would you still pay it in a bare-bones survival month?If yes, needs. If no, wants.

And then things get interesting, because some “needs” are negotiable long-term. Housing is a need, a penthouse is not.

Failure #3: 20% savings is either too low or totally unrealistic

This rule assumes your financial priorities are “save a bit, live a bit.” Great for many people.

But two groups break the model:

#### Group A: People in high-interest debt

If you’re paying 18% to 29% APR on credit cards, the 20% bucket may need to be much bigger, at least temporarily. Minimum payments belong in “needs,” but the extra payoff belongs in the 20% bucket. If the debt is severe, the real split might look like 55/15/30 for a season.

#### Group B: FIRE people (hi, you’re among friends)

If you’re chasing financial independence, 20% savings is often “normal retirement pace,” not early retirement pace.

If you want the aggressive version, the lever that matters most is savings rate. If you want the deeper math and timelines, read FIYR’s guide on why savings rate is the fast track to freedom: Savings Rate for FIRE: The Fastest Path to Freedom.

Quotable truth: 50/30/20 is training wheels. FIRE is riding downhill with no hands.

The 50/30/20 stress test (2 minutes, zero drama)

Before you adopt the rule, run this quick test using your last full month (or a 3-month average if your spending swings).

Step 1: Calculate your net monthly income

Use what actually hit your checking account.

Step 2: Sort your spending into Needs, Wants, and Savings/Debt

Be honest. If you label everything “need,” the budget becomes fan fiction.

Step 3: Compare your real percentages

If you’re close to 50/30/20, you can use the rule as-is.

If you’re not close, you didn’t fail. You just learned what your life costs.

Here’s a simple interpretation table.

| If your reality looks like… | What it usually means | Better move |

|---|---|---|

| Needs 45% to 55% | Healthy fixed-cost base | Run classic 50/30/20 |

| Needs 56% to 65% | Tight fixed costs, little flex | Use 60/25/15 or 65/20/15 |

| Needs 66%+ | Structural squeeze | Stabilize, cut big costs, boost income |

| Wants 35%+ | Lifestyle creep or leaks | Cap categories, subscription audit |

| Savings under 10% | No margin, high stress risk | Build starter emergency fund first |

How to make 50/30/20 work in real life (without becoming a budgeting monk)

This is where most articles get weirdly motivational. Let’s stay practical.

1) Start with a “truth month,” not a “perfect month”

Pick a normal month. Track everything. No self-punishment.

If you’re using FIYR, this is where it’s built to help: income and expense tracking, clean categories, and rules that stop your data from turning into spaghetti.

If you’re coming from Mint, Monarch Money, Copilot, Rocket Money, or Quicken, the key is the same: your budget is only as smart as your categorization is accurate.

2) Define your needs with one boring but powerful rule

Needs are bills you would keep paying during a financial emergency.This avoids the classic “my $280 monthly skincare routine is self-care and therefore a need” debate. (It might be self-care. It is not a need. Sorry.)

3) Convert the 30% wants bucket into a “no-guilt cap”

The wants bucket is not permission to spend mindlessly. It’s permission to spend intentionally.

A simple approach:

- Set one cap for “Fun Money” (dining out, entertainment, shopping)

- Keep one separate cap for “Experiences” (travel, events)

In FIYR, you can do this cleanly with custom categories and category groups, so your “wants” don’t hide inside a generic “Lifestyle” blob.

Quotable truth: The point of a budget isn’t to stop spending, it’s to stop regretting.

4) Make the 20% bucket automatic, or it won’t happen

If savings relies on willpower, it dies on Wednesday.

Automate the 20% bucket like it’s a bill:

- Retirement contributions

- Emergency fund transfers

- Extra debt payments

- Brokerage auto-investing

Then track it as a metric, not a feeling. FIYR’s savings rate calculator and net worth tracking are basically the scoreboard your brain needs.

The “fixed cost trap” and how to escape it

If 50% needs feels impossible, the usual culprit is fixed costs.

Fixed costs are the financial equivalent of adopting a tiger. Sure, it’s cool. But now you have to feed it every month.

Here are the big ones that move the needle:

- Housing

- Car payment + insurance

- Childcare

- Debt minimums

If you want to get back toward 50/30/20, you don’t nickel-and-dime your way there. You renegotiate the big stuff.

That can mean:

- House hack, downsize, get roommates, refinance (if rates and eligibility allow)

- Sell the expensive car (yes, even if it has “heated everything”)

- Re-shop insurance

- Rebuild debt strategy (snowball or avalanche, pick your poison)

For debt payoff strategy details, FIYR has a strong breakdown here: Debt Payoff Smackdown: Snowball vs. Avalanche.

50/30/20 variants that actually make sense

If the classic rule doesn’t fit, don’t abandon structure. Adjust the structure.

Here are common variants that map to real life:

60/20/20 (HCOL training wheels)

Use when housing or childcare pushes needs above 50%, but you can still save meaningfully.

70/15/15 (stability mode)

Use when money is tight and the goal is to stop the bleeding, build a small emergency fund, and avoid new debt.

If you need a full emergency fund playbook, FIYR’s guide is solid: Building Your Emergency Fund: The Ultimate Safety Net.

50/20/30 (FIRE-ish, without going full hermit)

Same as classic, but you deliberately shrink wants and boost saving.

55/15/30 (debt annihilation sprint)

Use when high-interest debt is the emergency. This is not forever. It’s a season.

Quotable truth: Your budget should change as your life changes. That’s not inconsistency, that’s competence.

The most common 50/30/20 mistake: ignoring “true expenses”

True expenses are non-monthly costs that show up like surprise villains:

- Car repairs

- Annual subscriptions

- Holidays

- Travel to weddings (because love is real and plane tickets are criminal)

If you don’t plan for these, your budget looks great until it doesn’t.

The fix is simple: build sinking funds.

Where do they go in 50/30/20?

- If it’s a predictable obligation (insurance premiums, annual fees), treat it like needs.

- If it’s a choice (vacation fund), treat it like wants.

- If it’s future-focused (emergency fund, investing), treat it like savings.

In FIYR, you can create dedicated categories (and even label big goals like “Italy Trip 2026”) so you see the full cost of a life choice before it happens, not after.

Make it stick: a simple weekly rhythm (10 minutes)

50/30/20 fails when it becomes a monthly surprise. The fix is not more tracking. It’s a tiny rhythm.

Once a week:

- Check your “wants” spend vs the cap

- Scan for any new recurring charges (subscription creep is undefeated)

- Make one adjustment for the next 7 days

If subscriptions are your Achilles heel, this pairs well with a dedicated subscription workflow. FIYR has a full guide here: Best Apps to Manage Subscription Renewals.

Quotable truth: Budgets don’t fail from one big purchase, they fail from 47 tiny ones you stopped noticing.

A practical way to run 50/30/20 inside a modern tracker (without losing your mind)

If you want 50/30/20 to feel easy, your tool has to do three jobs:

1) Track spending accurately (no mystery “Transfers” bucket swallowing your truth)

2) Make categories customizable (your life is not a default template)

3) Help you see progress (net worth, savings rate, goals)

That’s the lane FIYR is built for: a modern alternative to Mint, Monarch Money, Copilot, Rocket Money, and Quicken, with budgeting flexibility plus FIRE-friendly metrics.

A clean FIYR setup for 50/30/20 looks like this:

- Create three category groups: Needs, Wants, Savings/Debt

- Map categories into the right group (yes, you have to decide if streaming is a want)

- Use transaction rules to auto-sort repeat merchants

- Track subscriptions so recurring charges stop freeloading

- Watch savings rate and net worth like a grown-up scoreboard

The bottom line

Budget allocation 50/30/20 works when your needs are reasonable, your income is stable, and your goal is balanced progress. It fails when fixed costs crush you, debt demands a bigger share, or you’re aiming for FIRE speed.Use it like a compass, not a cage.

Start with the rule. Measure reality. Then customize the split to match your actual life, not your aspirational Pinterest life.

Because the real flex is not following 50/30/20 perfectly.

The real flex is knowing exactly where your money goes, and making it go where you want.