How to Retire 15 Years Earlier: The Simple Math No One Tells You

Most people think retiring early is about finding a hot stock or striking it rich with a side hustle. Cute. The real unlock is a boring fraction: your savings rate. Change that percentage, and you change your retirement age. Not in theory, in calendar years.

Here’s the part nobody tells you: a 10 point bump in savings rate can cut 10 to 15 years off your timeline. That is not motivational poster math. That is compounding, contributions, and a smaller target working in your favor at the same time.

The uncomfortable truth: retire earlier by shrinking the target and feeding the engine

Early retirement is a two-gear machine.

- Gear 1, your savings rate, increases the dollars you invest every month.

- Gear 2, your spending level, sets your target. Lower annual spending means a smaller financial independence number.

That double effect is why small changes move big dates. Most of us are stuck because the machine is pointed the wrong way. Nearly 60 percent of Americans still live paycheck to paycheck and 61 percent carry credit card debt, averaging about $5,875 owed. That is a tough starting line, but it also proves the leverage lives in the gap between what you earn and what you keep. Source: CNBC.

The simple FIRE-number walkthrough

Your FI number is the nest egg that can safely fund your annual spending forever.

- Step 1, tally annual spending. This is the non-negotiable floor of your lifestyle.

- Step 2, pick a conservative withdrawal rate. Many planners use 4 percent as a starting point. See our guide on the 4 percent rule for nuance.

- Step 3, FI number = annual spending divided by withdrawal rate.

Examples:

- Spend 40,000 per year, 4 percent rule. FI number about 1,000,000.

- Spend 60,000 per year. FI number about 1,500,000.

- Spend 120,000 per year. FI number about 3,000,000.

One-liner you will never forget: every 1 dollar you cut from your annual spending lowers your FI target by about 25 dollars. Cancel a 30 dollar per month subscription, that is 360 dollars per year, and you just shrank your FI number by about 9,000 dollars. That is not a latte, that is an entire chunk of retirement bought back.

The math nobody explains in plain English

Let’s define savings rate as the percent of your take-home pay you save or invest for the long-term. If you save 25 percent, you spend 75 percent. Your FI target is 25 times that annual spending, and your contributions are the 25 percent you invest each year.

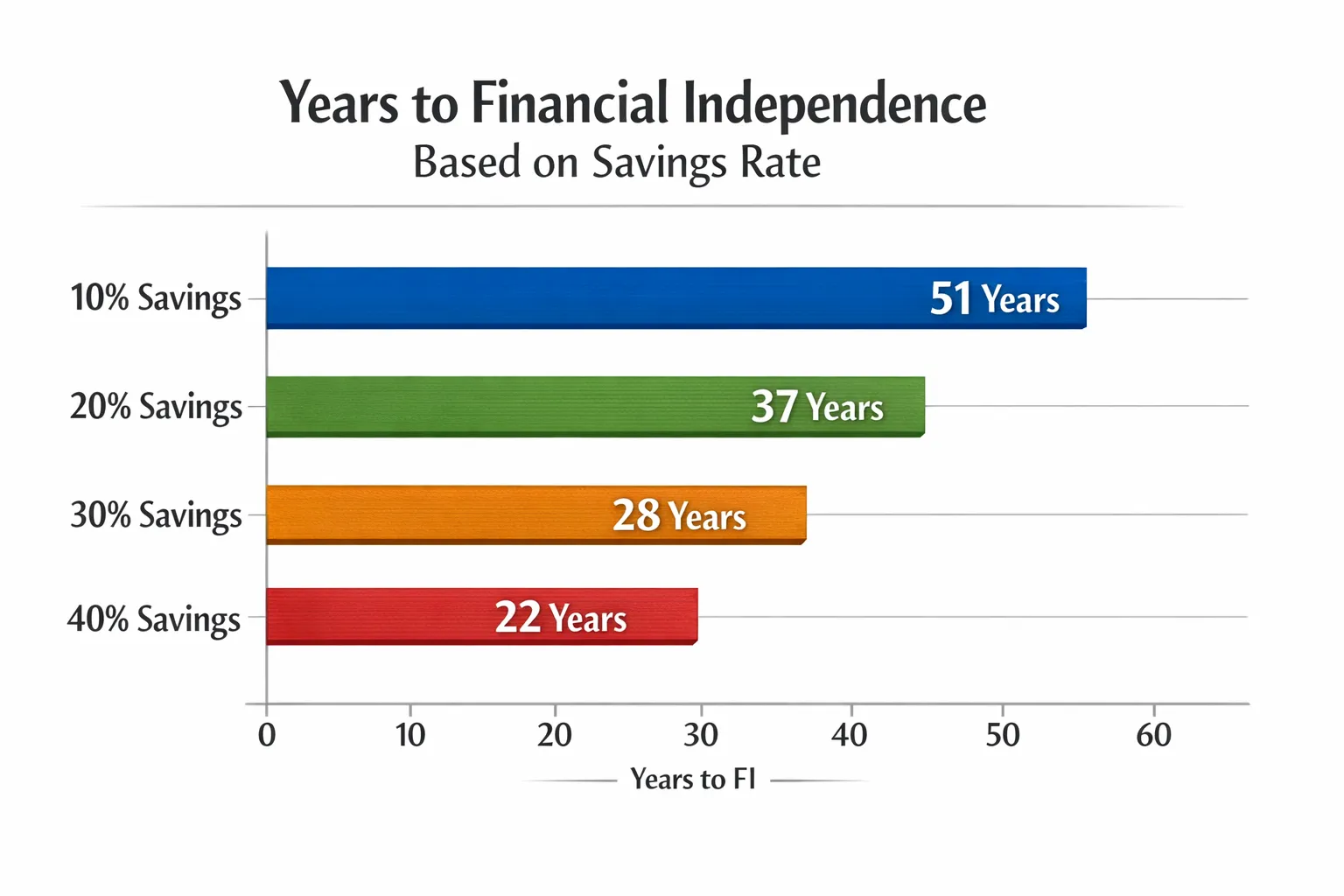

Assume your investments earn 5 percent after inflation over the long run, which is a reasonable real return for a stock-heavy portfolio. Using that, here is a rough map from savings rate to years to FI if you are starting near zero:

| Savings rate | Approx years to FI |

|---|---|

| 10% | 51 |

| 15% | 43 |

| 20% | 37 |

| 25% | 32 |

| 30% | 28 |

| 35% | 25 |

| 40% | 22 |

| 50% | 17 |

| 60% | 12 |

| 70% | 9 |

Assumptions: 5 percent real return, 4 percent withdrawal rule, steady savings rate. Reality will wobble year to year, but the direction is right.

Translation you can use: as savings rate rises, you save more and need less. That is why the curve bends so sharply.

Three short timelines that cut real years

We will keep this painfully simple and brutally realistic. Ages are examples. Plug in your own.

1) 10 percent to 20 percent savings rate

- Timeline drop: about 51 years to about 37 years. You just bought back roughly 14 years.

- Story: Meet Devon, 35, saving 10 percent on 80,000 take-home. After a six-month sprint to kill high-APR debt, renegotiate car insurance, and split rent with a roommate, Devon hits 20 percent. Result: Devon’s retirement age moves from late 80s to early 70s. That is not magic. That is math.

2) 15 percent to 25 percent

- Timeline drop: about 43 years to about 32 years. You just bought back roughly 11 years.

- Story: Aisha, 30, takes home 75,000. At 15 percent she invests about 11,250 per year, spends 63,750, and her FI number sits near 1.59 million. She nudges to 25 percent by rolling off a car lease, trimming subscriptions, and capturing a raise without inflating lifestyle. Now she invests 18,750 per year, spends 56,250, and her FI number shrinks to about 1.41 million. Contributions up, target down. Timeline drops by a decade.

3) 30 percent to 40 percent

- Timeline drop: about 28 years to about 22 years. That is about 6 years gained.

- Story: Jordan and Mia, 28, already live pretty lean. They unlock 40 percent through one big move, a housing change, and one small one, selling the second car. Six years may not sound wild until you realize that is two presidential terms or your kid’s entire K-6. They just moved a whole life chapter forward.

Here is the punchline: you do not have to become a monk. You have to widen the gap between what comes in and what goes out, then let compounding do the heavy lifting.

Compounding and contributions, the power couple

Two truths that will save you a decade:

- Investing early matters more than investing perfectly. An extra 500 dollars per month invested for 20 years grows to roughly 200,000 in today’s dollars at 5 percent real. That is one pay-yourself-first transfer away.

- Cutting recurring expenses beats cutting one-time splurges. A permanent 300 dollar per month reduction lowers your FI number by roughly 90,000 and increases contributions by 3,600 per year. That is a two-for-one that compounds.

If your budget has more leaks than a 2003 Civic, you will feel this next line: compounding cannot save what you do not invest.

The 10-point plan to add 10 points to your savings rate

This is a 90-day sprint. No gurus. No 47-tab spreadsheet. Just a system.

1) Calculate your baseline

- Savings rate s = annual long-term savings divided by annual take-home pay. Count 401k, IRAs, brokerage contributions, HSA invested dollars, principal payments on 0 percent loans you plan to keep. Do not count transfers you later spend.

2) Set a target and a timer

- Add 10 points to your current rate. Give yourself 90 days to lock it in.

3) Attack the Big Three first

- Housing. Aim for 25 to 30 percent of take-home. Levers include negotiating rent at renewal, moving one zip code over, or house hacking one room. One creative housing move often does more than 30 small cuts.

- Transportation. Drive your existing car longer, refinance high-APR loans, or go down one car if you can. Cars are stealth wealth killers because they combine depreciation, insurance, gas, and maintenance.

- Food. Set a weekly cap, not a vibe. Groceries plus restaurants together. Batch-cook two dinners, meal-prep one lunch, and budget guilt-free dining within the cap.

4) Close the subscription loop

- Write down every recurring charge. Kill the 30 to 70 dollar zombies you forgot about. Remember, every 30 dollars per month you cancel cuts your FI number by about 9,000.

5) Monetize the calendar, not just the paycheck

- Negotiate your raise with receipts. List measurable wins, ask for a specific number, and pre-commit to bigger outcomes. Then lock at least half of any raise into auto-savings on day one.

6) Automate the new savings rate

- Move the money the day you get paid. Increase your 401k percent, auto-transfer to IRA or brokerage, and treat it like rent. If you see it, you will spend it.

7) Pick boring, low-cost investments

- Broad index funds win most long games. For a starter blueprint, see our index fund guide.

8) Build a safety buffer

- Keep 3 to 6 months of essential expenses in cash. See our emergency fund guide. Security keeps you from selling at the worst time.

9) Install anti-creep guardrails

- Freeze lifestyle inflation for 60 days after any raise. Cap categories. Use a 24 to 72 hour delay on non-essentials. More on this in our lifestyle creep playbook.

10) Review weekly, adjust monthly

- Fifteen minutes on Sunday. Scan spending, confirm transfers, tag irregulars, and move on with your life.

Oh, and this is all easier if your tools work for you. FIYR tracks income, expenses, and subscriptions in one place, calculates savings rate, and projects your FIRE date so you can see the decade you just bought back. Use labels like New York Trip 2025 to see the full cost of a plan, and dynamic budgets with safe-to-spend so today’s choices match tomorrow’s goals.

A quick, concrete example you can copy

Let’s say your take-home is 6,250 per month, 75,000 per year.

- At 15 percent savings. You invest 11,250 per year, spend 63,750, FI number about 1.59 million, years to FI about 43.

- At 25 percent savings. You invest 18,750 per year, spend 56,250, FI number about 1.41 million, years to FI about 32.

Move one percentage point per week for 10 weeks. Each week, lock in one small change. Renegotiate one bill. Cancel one subscription. Add one percent to 401k. Batch-cook one meal. Sell one unused item. Repeat. Ten weeks later, your savings rate is up 10 points and your retirement is a decade closer. Systems beat sprints.

The psychology that keeps the math honest

If you try to white-knuckle this, you will burn out. Instead:

- Identity first. You are the kind of person who pays yourself before you pay your bills. See our saving psychology guide.

- Default to automation. If it is not automated, it is optional. If it is optional, it is toast by the 20th of the month.

- Design friction. Make spending slightly annoying and saving instant. Put your brokerage app on the home screen and your shopping apps in a folder called Not Today.

Risk, reality, and guardrails

- Markets. Some decades are kinder than others. The 4 percent rule is a planning starting point, not a guarantee. We explain the nuance here: Unlocking the 4 percent rule.

- Taxes and benefits. Optimize accounts before chasing yield. Employer match, HSA, IRA, taxable investing, in that order for most people. See our advanced tactics in Maximize Retirement.

- Debt. High-APR debt is a hair-on-fire emergency. Pay it before trying to out-invest it.

What to do next, today

- Write down your monthly take-home and last 12 months of spending. No judgment, just data.

- Compute your savings rate. If you are under 15 percent, aim for 25 percent. If you are at 25 percent, gun for 35 to 40 percent.

- Pick one big lever this month housing, car, or recurring bills and one small lever weekly.

- Automate the new percentage on payday. Then let compounding do what compounding does.

Your budget should not swing like a crypto chart. It should glide like a train on a schedule. Build the schedule, ride the rails.

A last thought for the skeptics: retiring 15 years earlier is not about perfection. It is about the math of a wider gap, sustained by a system you can live with. Make the gap boringly large and the calendar does the flexing for you.

P.S. If you want a scoreboard that shows your savings rate, FIRE date, and safe-to-spend in one place, FIYR was built for this. But whether you use FIYR, a spreadsheet, or a notebook taped to your fridge, the simple math above is the engine. Turn it on and do not turn it off.