Why People Fail at Saving (It’s Not Laziness, It’s Systems)

If your savings account balance has been stuck in a Groundhog Day loop, you’re not “bad with money.” You’re running a broken system.

And most people are.

We’ve turned saving into a personality test ("I’m just not disciplined"), even though modern money is designed like a casino with better lighting. Tap-to-pay, one-click checkout, invisible subscriptions, and credit that shows up faster than your Amazon package. Saving never stood a chance.

Meet Jordan.

Jordan makes decent money. Not hedge-fund money, but “I should be fine” money. Yet by day 24 of every month, Jordan is doing the ancient budgeting ritual known as moving money from Savings back to Checking while whispering, ‘I’ll put it back next month.’

Jordan isn’t lazy. Jordan’s system is.

The uncomfortable data: this isn’t a “you” problem

According to CNBC (citing a Payroll.org survey), 60% of Americans are living paycheck to paycheck. Add in the emotional toll and it gets spicier: 70% are stressed about finances, only 45% say they have an emergency fund, and 61% carry credit card debt, owing $5,875 on average. Some people are even going deeper every month.

That’s not “people forgot to brew coffee at home.” That’s a structural problem.

Here’s the point: saving fails when it’s treated as a mood, not a machine.

If you want saving to work, build a system that assumes:

- You will get tired.

- You will have chaotic weeks.

- You will forget annual bills.

- Your brain will rationalize nonsense at 11:47 pm.

Design for reality, not for your Best Self on January 1.

Source: CNBC coverage on paycheck-to-paycheck and financial stress.

Why people fail at saving (it’s not laziness, it’s these system failures)

You don’t need more motivation. You need fewer traps.

1) You’re trying to “save what’s left”

This is the classic failure mode: you pay rent, you live your life, you hope something remains, and you call that “saving.”

That’s not a plan. That’s a scavenger hunt.

System fix: flip the order.- Save first (automation).

- Spend what remains (constraints).

If saving is optional, it becomes negotiable. Your brain is an elite negotiator.

Memorable truth: If saving is the last bill you pay, it’s the first bill you skip.

2) Your cash flow timing is a mess (even if your budget looks fine)

People love monthly budgets. Bills love showing up on random Tuesdays.

A budget can be “correct” and still fail because your checking account hits zero at the wrong moment. Timing destroys savings.

System fix: build a paycheck-to-bills map.- List bill due dates.

- Align them with paydays.

- Create a buffer so the calendar stops bullying you.

This is where tracking matters. If you don’t know what’s coming, you’re not budgeting, you’re guessing.

Quotable line: Most “overspending” is just bad timing wearing a trench coat.

3) You keep getting ambushed by “true expenses”

Car insurance. Holidays. School fees. Annual subscriptions. Medical deductibles. Flights for weddings you “totally forgot about.”

None of these are emergencies. They’re predictable. They just aren’t monthly.

So people treat them like surprises, then “temporarily” stop saving.

System fix: turn ambush bills into monthly line items.Use the simplest formula in personal finance:

Monthly sinking fund = Total cost ÷ Months until dueThat’s it. That’s the whole spell.

When you do this, saving stops feeling like deprivation and starts feeling like not getting punched in the face.

Memorable truth: Your budget isn’t broken, your calendar is.

4) Subscriptions are eating your savings in $14.99 bites

This is the financial equivalent of gaining weight “somehow” while drinking three sodas a day.

Subscriptions are tiny, recurring, and emotionally invisible. The perfect predator.

You don’t need to cancel everything and live like a monk. You need visibility and a cap.

System fix: create a “Subscription Budget” category and make it fight for survival.- Put every recurring charge in one place.

- Set a monthly cap.

- Use a simple rule: if something enters, something leaves.

If you want saving to work, you have to stop bleeding.

One-liner: You can’t out-save a thousand paper cuts.

5) Your categories are lying to you

If half your spending is categorized as “Shopping,” your data is basically fan fiction.

This is where saving dies quietly.

Because when you can’t see what’s happening, you can’t fix it. And when you can’t fix it, you default to shame. Then you quit.

System fix: create decision-grade categories.Examples that actually help:

- Convenience Food (the “I’m too tired to cook” tax)

- Subscriptions

- Fees + Interest (aka “I paid for nothing”)

- Amazon Needs vs Amazon Wants

If you’re coming from Mint, you probably remember the vibe: decent overview, messy categorization, lots of “close enough.” In 2026, close enough is expensive.

Quotable line: If your categories are vague, your decisions will be vague.

6) You don’t have an emergency fund, so every hiccup becomes debt

No buffer means every unexpected expense becomes a credit card swipe.

Then saving feels impossible because you’re trying to sprint with a backpack full of rocks.

And yes, many people are stuck here because incomes are tight and costs are high. That’s real.

But even then, the right system changes outcomes because it creates stability first.

System fix: build a starter buffer before you chase big goals.- Start with a small “shock absorber” fund (even $500 to $1,000 helps).

- Then build toward 1 month of expenses.

- Then 3 to 6 months, depending on risk and income stability.

Memorable truth: You can’t save for the future if the present keeps lighting fires.

7) You aren’t tracking the one number that makes saving addictive

Saving needs a scoreboard. Humans change behavior when they can see it.

A vague goal like “save more” is motivational until it meets real life.

System fix: track savings rate (and watch it like a hawk).Simple version:

Savings rate = (Income − Spending) ÷ IncomeIf you want FIRE (Financial Independence, Retire Early), this metric is the steering wheel. Not your investment picks. Not your hot take on the Fed.

Quotable line: What gets tracked gets improved. What stays fuzzy stays broke.

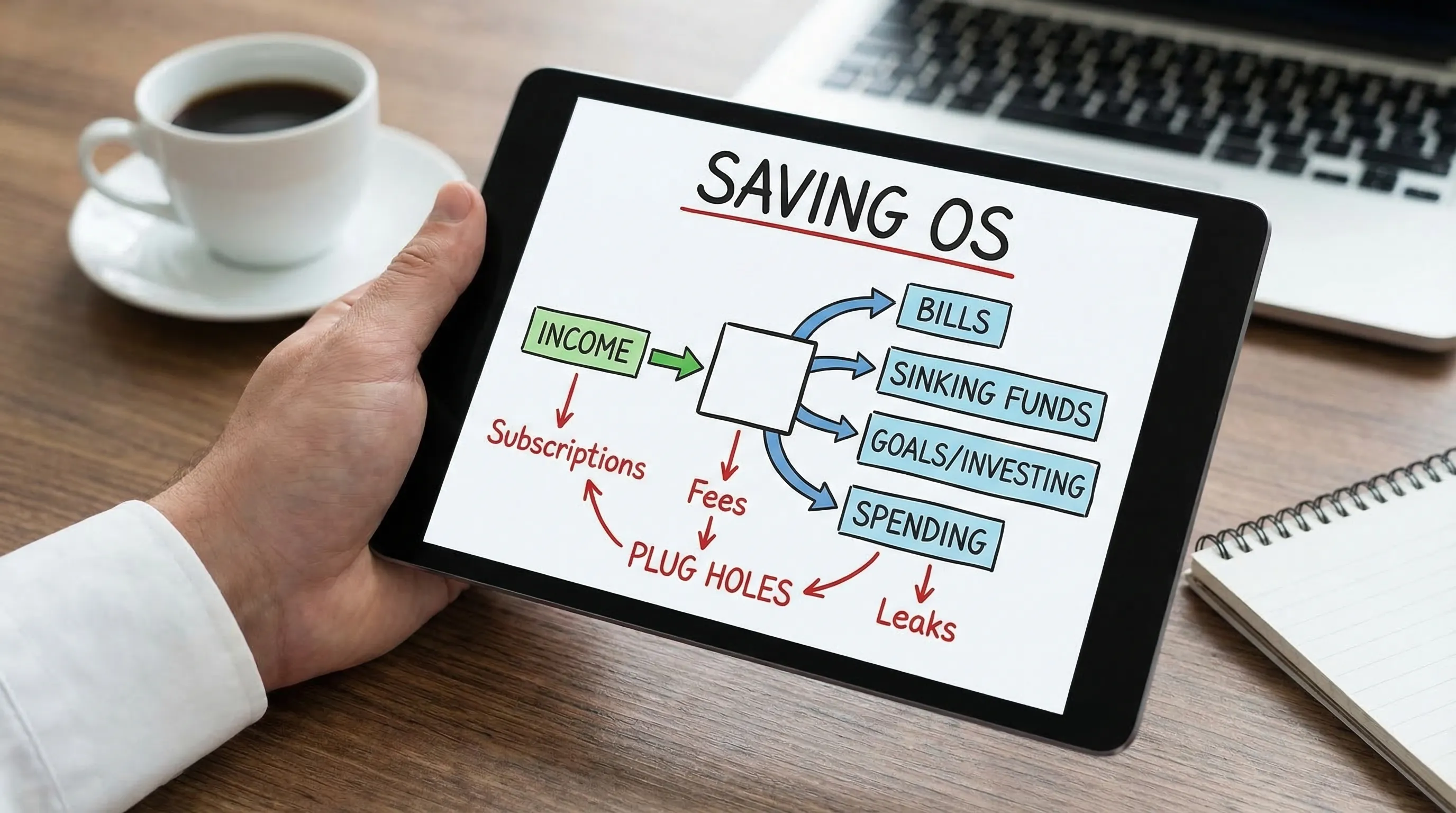

The “Saving OS”: a system that works even when you’re tired

This is the part nobody talks about: saving isn’t one habit. It’s a workflow.

Here’s a simple operating system you can set up in about 60 to 90 minutes, then maintain in 15 minutes a week.

Step 1: Define your three buckets (and stop overcomplicating it)

- Floor: non-negotiable bills (housing, utilities, insurance, minimum debt payments)

- Flex: variable life (groceries, gas, eating out, fun)

- Future: saving, investing, sinking funds, extra debt payoff

If you only do one thing, do this. It creates structure without turning your life into a spreadsheet cosplay.

Step 2: Build a “Bills Before Thrills” transfer sequence

Make saving automatic and boring. Boring is elite.

A practical sequence:

- Payday hits

- Transfers happen within 24 hours

- Flex spending is what’s left

This is where apps beat willpower. A modern tracker helps you see whether the transfers are realistic and whether Flex is silently ballooning.

Step 3: Create sinking funds for the top 5 “ambush” categories

Start with the stuff that predictably wrecks people:

- Car repair and maintenance

- Medical out-of-pocket

- Gifts and holidays

- Annual subscriptions (or annual insurance premiums)

- Travel (because life happens)

Sinking funds are not cute. They are the difference between “minor inconvenience” and “new credit card balance.”

Step 4: Put subscriptions on trial

Do a monthly subscription review and ask two savage questions:

- “Would I buy this again today at full price?”

- “If I removed this, would my life get worse… or just slightly quieter?”

Then cap the category.

Step 5: Make your data clean enough to trust

Clean data is not a “nice to have.” It is the foundation of saving.

This is why people quit: they track for two weeks, the categories are wrong, the numbers feel fake, and they go back to vibes.

A better approach:

- Use custom categories that reflect your reality.

- Use transaction rules so the same merchants get categorized correctly every time.

- Use labels for one-off events (example: “New York Trip 2026”) so your monthly budget doesn’t look like it got hit by a bus.

This is the kind of thing FIYR is built for: flexible categories, rules-based automation, subscription tracking, savings rate, net worth, and FIRE projections in one place. Less “budgeting theater,” more control.

Step 6: Install one weekly ritual (15 minutes, no drama)

Pick a day. Set a timer. Do this:

- Review transactions that need categorizing

- Check subscription charges

- Compare actual spending vs your Flex cap

- Move any leftover Flex into Future (yes, weekly)

It’s not about perfection. It’s about not letting the month get away from you.

One-liner: Your money doesn’t need more rules, it needs a meeting.

A practical cheat sheet: failures, fixes, and the tool support that helps

Here’s the map from “why is saving impossible?” to “oh, that’s the lever.”

| Why saving fails | What it looks like in real life | System fix | How FIYR helps (naturally) |

|---|---|---|---|

| Saving is residual | “I’ll save whatever’s left” (spoiler: nothing) | Automate saving first | Track cash flow, budgets, goals, safe-to-spend |

| Cash flow timing mismatch | Low balances right before due dates | Payday-to-bills mapping + buffer | Income/expense tracking, budget guardrails |

| True expenses ignored | Random big months, savings gets raided | Sinking funds formula | Custom categories/groups and goal tracking |

| Subscription creep | “How am I paying for 12 apps?” | Subscription cap + monthly review | Subscription tracking and recurring charge visibility |

| Category fog | Everything is “Shopping” or “Misc” | Decision-grade categories + labels | Custom categories, labels, transaction rules |

| No emergency buffer | Every surprise becomes debt | Starter fund, then runway | Net worth tracking (assets + liabilities) |

| No feedback loop | No idea if progress is real | Track savings rate weekly | Savings rate calculator + FIRE date projection |

Quick story: the “I make good money” trap

I once worked with a guy who insisted he didn’t need budgeting because he “made enough.”

Then he actually tracked.

Turns out he had:

- Three streaming services

- Two “premium” news subscriptions

- A gym membership he hadn’t visited since the Obama administration

- And a recurring charge for a meditation app he opened only when he was stressed about money

Poetry.

When he finally grouped subscriptions into one category and put a cap on it, he freed up a few hundred bucks a month without touching rent or groceries.

He didn’t become a new person. He just stopped letting autopay freeload.

Memorable truth: Your income isn’t the problem. Your defaults are.

For goal math: use calculators, not hope

If you’re saving for a specific target (a debt payoff date, a down payment, a retirement milestone), do the math once so your brain can stop improvising.

If you want a lightweight set of free calculators, My Paisa HQ’s finance calculators are a handy toolbox, especially for goal-based SIP style planning and other scenarios.

Then bring that number back into your system as a monthly transfer, not a “someday” intention.

Frequently Asked Questions

Why do people fail at saving even with a good income? Good income often increases convenience spending, subscription creep, and lifestyle upgrades. Without a system (automation, caps, tracking), savings becomes residual and disappears. What’s the fastest way to start saving if I’m living paycheck to paycheck? Start with a starter buffer (even $500), track expenses for visibility, cut recurring leaks first, then automate a small savings transfer that grows over time. Should I pay off debt or save first? If you have high-interest debt, prioritize minimum emergency cash (a small buffer) plus aggressive debt payoff. The buffer prevents new debt when life happens. How do I save with irregular income? Use an income floor (a conservative monthly baseline), build a buffer during high months, and automate transfers based on that baseline instead of guessing each month. What’s the best metric to track for saving progress? Savings rate. It connects your daily spending to your long-term goals, including FIRE. Tracking it weekly keeps you honest without obsessing over every latte.Build the system, then let it run

You don’t need a monk mindset. You need a money system that works when you’re busy, stressed, and one “free trial” away from chaos.

If you want an easier way to run this without spreadsheets and manual cleanup, FIYR brings the pieces together: spending tracking, customizable categories, transaction rules, subscription visibility, net worth tracking, savings rate, and FIRE-focused projections.

Set it up once. Then let your system do what motivation never does: show up every day.