What Is a Good Savings Rate? Real Benchmarks

You’re asking “what is a good savings rate?” like it’s a universal truth, right up there with gravity and “don’t microwave aluminum.”

It’s not.

A “good” savings rate depends on what you’re trying to do: survive, stabilize, get out of debt, buy back your time, or go full FIRE and retire while your coworkers are still arguing about Slack emojis.

But here’s the uncomfortable part nobody wants to admit:

Most people don’t even know their real savings rate.

They feel like they’re saving (because the checking account balance didn’t hit zero), while the data says otherwise. A CNBC report cited that around 60% of Americans are living paycheck to paycheck, and 61% are in credit card debt. That’s not “bad at math.” That’s “the system is sticky, and money leaks are sneaky.”

Let’s fix the confusion with real benchmarks, a simple framework, and a way to pick a target that actually matches your life.

First: what “savings rate” even means (because people count it like calories)

At its simplest:

Savings rate = (money you kept) / (money you earned)The chaos starts when we argue about what counts as “kept” and what counts as “earned.” (Congrats, you have officially entered personal finance discourse hell.)

Here are the two definitions that matter in real life.

| Savings rate type | Simple formula | Best for | What it captures (and misses) |

|---|---|---|---|

| Cash-flow savings rate | (Income - Expenses) / Income | Everyday budgeting, building an emergency fund, stopping overspending | Captures your monthly reality. Misses employer match unless it hits your accounts. |

| FIRE-style savings rate | (Savings + investments contributions) / Income | Planning for financial independence, optimizing contributions | Captures intentional “future you” funding. Can get messy with pretax deductions and irregular income. |

If you’re a normal human trying to stop your finances from doing parkour every month, cash-flow savings rate is the cleanest starting point.

And if you’re chasing FIRE, you eventually want the second view too, but only after your tracking is accurate. Garbage in, fake confidence out.

The national “benchmark” is… not inspiring

If you want a reality check, the U.S. personal saving rate (macro data) has often been in the single digits in recent years (with spikes during unusual periods). The Bureau of Economic Analysis tracks it monthly in Table 2.1.

Translation: if you’re saving 15% consistently, you’re already playing a different sport than most of America.

Your savings rate isn’t a morality score, but it is a directional signal.

So what is a good savings rate? Real-world benchmarks that actually help

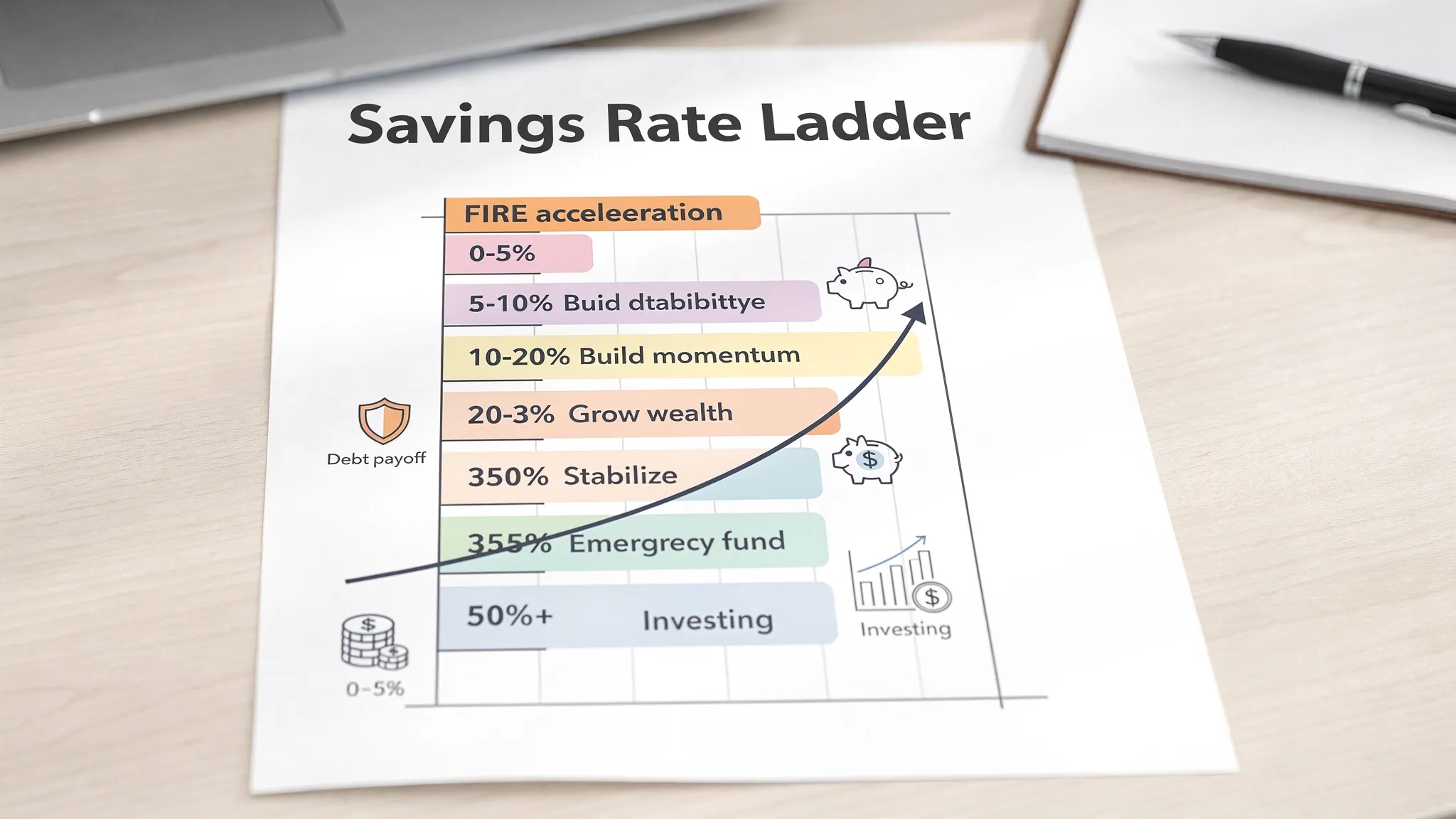

Let’s stop pretending there’s one magic number. Instead, use a ladder.

The Savings Rate Ladder (practical, not preachy)

| Savings rate | What it usually means | The honest next move |

|---|---|---|

| 0% to 5% | You’re treading water, or one “surprise” expense away from debt | Build a starter buffer, kill obvious leaks, reduce volatility |

| 5% to 10% | You’re stable-ish, but progress is slow | Automate savings, tighten categories, get subscription visibility |

| 10% to 20% | You’re doing what mainstream advice calls “responsible” | Increase retirement contributions, reduce big fixed costs |

| 20% to 35% | You’re building real wealth momentum | Systemize lifestyle creep defense, optimize taxes and investing |

| 35% to 50% | You’re in FIRE acceleration territory | Keep lifestyle steady, scale income, avoid burnout decisions |

| 50%+ | You’re either high-income, aggressively minimalist, or both | Make sure you’re not accidentally making life smaller than you want |

A good savings rate is the one that matches your mission.

If your mission is “retire early,” 10% is polite but not powerful. If your mission is “stop panic-charging car repairs,” 10% might be heroic.

Benchmarks by goal: what you’re trying to buy is time

Different goals, different “good.”

If your goal is basic stability

A good target: 5% to 10%

This isn’t sexy. It’s foundational. It’s “my life has fewer financial jump scares.”

Stability looks like:

- A starter emergency fund

- No missed payments

- A month that doesn’t require financial improvisation

If you’re still paying interest to exist, your savings rate goal is less about investing and more about getting oxygen.

If your goal is “normal retirement” (not early)

Two common benchmarks show up again and again:

- 15% of income toward retirement is a widely cited rule of thumb from Fidelity (retirement savings guidance varies by situation, but this is a common starting point). See Fidelity’s retirement rules of thumb.

- The classic 50/30/20 budget implies 20% toward savings and debt paydown.

A good target: 15% to 20%

That range is basically “I’m building future options while still living in the present.” Balanced, boring, effective.

If your goal is FIRE (financial independence, retire early)

A good target: 25%+, with many FIRE-focused households pushing 35% to 50%.

Why so high? Because FIRE isn’t “retire someday.” It’s “compress the timeline.” The lever is savings rate.

But here’s the twist: people chase a high savings rate while their tracking is sloppy. That’s like bragging about your bench press while standing on a trampoline.

Benchmarks by life stage (because a 24-year-old and a new parent are not the same species)

Here’s a more human set of targets.

| Life situation | A “good” savings rate target | Why |

|---|---|---|

| Student / first job / low cash cushion | 5% to 10% | Build the habit and a buffer before optimizing |

| Young professional with stable income | 10% to 20% | Strong base, room to grow without misery |

| Family with childcare and high fixed costs | 10% to 15% (then climb) | Consistency matters more than perfection |

| Paying off high-interest debt | “Positive and rising” | Debt payoff is a form of saving, prioritize stopping interest bleeding |

| High income, high expenses (classic lifestyle creep zone) | 20% to 35% | You can do it, if you stop upgrading everything |

| FIRE-focused household | 35% to 50%+ | Aggressive timeline compression |

| Freelancer / irregular income | Target a floor (10%+) + buffers | Stability beats volatility, then you scale |

The point is not to compare yourself to a Reddit spreadsheet warrior living on lentils.

The point is to set a target that moves you forward in your constraints.

The three ways people accidentally lie to themselves about savings rate

Meet Daniel.

Daniel proudly told his friends he saves “like 30%.” He said it with the energy of a man who had transcended capitalism.

Then he actually tracked everything for a month.

- He forgot the annual car insurance renewal.

- He ignored the streaming subscriptions multiplying like rabbits.

- He counted a credit card payment as an “expense” and also counted the purchases, double-counting spending.

Daniel’s real savings rate: 11%.

Still decent. Just… not the financial superhero origin story he was pitching.

Here are the most common savings-rate distortions:

1) You’re not tracking subscriptions and recurring charges

Recurring charges are the cockroaches of personal finance: they survive everything and come out at night.

If you don’t have clear subscription tracking, your savings rate is basically vibes.

2) Your categories are messy (so your numbers are fiction)

If “Amazon” is a category, you don’t have a budget. You have a confession booth.

Clean categories and consistent rules matter because your savings rate is downstream of your spending data.

3) Irregular income makes your “monthly” savings rate look drunk

Freelancers and commission earners often “save” 40% one month and -10% the next. That’s not a personality flaw. That’s math.

You need averaging and buffers, not guilt.

How to choose your personal “good” savings rate in 10 minutes

Use this simple decision framework.

Step 1: Pick the mission (one sentence)

Examples:

- “I want a $5,000 emergency fund in 12 months.”

- “I want to max my employer match and stop using credit cards as a float.”

- “I want to hit FI in 12 to 15 years.”

If your mission is fuzzy, your savings rate target will be fantasy.

Step 2: Set a floor, a target, and a stretch

This prevents the all-or-nothing spiral.

- Floor: the minimum you can hit even in a rough month

- Target: what you can hit with normal discipline

- Stretch: what you can hit when life is calm and you’re focused

A realistic example:

- Floor: 8%

- Target: 15%

- Stretch: 22%

Consistency beats occasional greatness. Your savings rate should not swing like a crypto chart.

Step 3: Convert the target into a monthly number

If your take-home income is $6,000 and your target savings rate is 15%:

Monthly savings target = $6,000 × 0.15 = $900Now it’s not a philosophy. It’s a number you can actually execute.

How to increase your savings rate (without turning into a joyless monk)

You don’t need 47 micro-optimizations. You need a system that hits the big levers.

Lever 1: Find the leaks (small stuff, but it adds up)

This is where subscription creep, impulse buys, and “treat yourself” culture do their dirty work.

A practical weekly habit:

- Review the last 7 days of transactions

- Flag anything that surprised you

- Set one rule for next week (a cap, a swap, or a delay rule)

The win is not perfection. The win is that your spending stops being a mystery novel.

Lever 2: Cut one big fixed cost (the adult move)

If you want a meaningful savings rate jump, look at:

- Housing

- Transportation

- Insurance

- Childcare (harder to change, but still worth auditing)

One renegotiation or one lifestyle choice here can outperform months of skipping lattes. (Lattes are innocent. Your car payment is the villain.)

Lever 3: Capture income growth before it becomes lifestyle

Raises are where savings rates go to die.

A simple rule: when income goes up, redirect part of the increase automatically. If you want a structure, FIYR’s blog has discussed “raise rules” like a 70/20/10 style split in other contexts, but the concept is universal: pre-decide where the money goes so you don’t accidentally spend it.

Your future self should get paid first, not whatever ad follows you around the internet.

Make this easier with tracking that doesn’t fight you (the FIYR angle)

Savings rate advice is cheap. Execution is the expensive part.

This is where a modern money tracker earns its keep.

With FIYR, you can make savings rate tracking less like guesswork and more like a dashboard for your life:

- Track income and expenses in one place (so your savings rate is calculated from reality, not hope)

- Use custom categories and category groups (so “shopping” isn’t hiding inside “misc” like a financial jump scare)

- Set automatic transaction rules to keep categorization clean over time

- Turn on subscription tracking to see recurring charges before they quietly eat your margin

- Watch net worth alongside savings rate (because saving is good, but building assets is the point)

- Connect savings behavior to a FIRE date calculator (if you’re aiming for early retirement)

- Use goal tracking with safe-to-spend to avoid the classic “I saved, but then I overspent” loop

If you want the deeper math and setup, FIYR has a dedicated guide on savings rate calculation and a practical push on how to boost your savings rate without making your life miserable.

The takeaway: the best savings rate is the one you can measure cleanly and repeat.

The punchline (and the truth)

A good savings rate is not a flex. It’s not a personality. It’s not a TikTok identity.

It’s a tool.

- If you’re at 5%, you’re building stability.

- If you’re at 15%, you’re building a future.

- If you’re at 35%+, you’re buying back years of your life.

Pick the benchmark that matches your mission, track it like you mean it, and let your savings rate quietly become the most powerful number in your finances.

Because the real win isn’t a perfect percentage.

It’s waking up one day and realizing money stopped being the boss.