Spending Trends by Age: What Your 20s, 30s, 40s Reveal

If you think your spending “matures” with age, I have a gently used Peloton to sell you.

Your spending doesn’t grow up. It just changes outfits.

In your 20s it’s brunch, Ubers, and “networking” (read: $18 cocktails). In your 30s it’s daycare, a mortgage, and the kind of Target runs that qualify as small-business procurement. In your 40s it’s home repairs, healthcare creep, and realizing your parents’ finances are now… also your problem.

That’s why spending trends by age matter. Not because we’re judging, but because your budget is basically a time machine. It tells you where your life is headed before your calendar does.

Here’s what your 20s, 30s, and 40s reveal, and how to use the pattern to get richer faster (without living like a monk).

The uncomfortable truth: most people don’t have a spending problem, they have a “life stage” problem

Meet Jordan, 27. Solid job. “Pretty responsible.” Former Mint user who migrated to a modern tracker because Mint-style categories kept lumping everything into nonsense like “Shopping.”

Jordan finally looks at the last 90 days of transactions and says the sentence every adult eventually says:

“I don’t even remember buying this.”

Food delivery shows up like a recurring tax. Subscriptions multiply like gremlins. And the real kicker, Jordan is not alone.

- A CNBC report cited a survey showing around 60% of Americans are living paycheck to paycheck, and 70% are stressed about money. Not because they’re dumb, but because modern spending is designed to be invisible and frictionless. (CNBC)

Now zoom out.

The U.S. Bureau of Labor Statistics’ Consumer Expenditure Survey has been showing the same broad arc for years: spending typically rises from early adulthood, often peaks in midlife (roughly the 45 to 54 range), then declines as households shrink and priorities shift. (BLS Consumer Expenditures)

Translation: you’re not “bad with money.” You’re just living through the expensive decades.

And then things get interesting.

The 3 forces that change spending as you age (more than “discipline” ever will)

1) Fixed costs solidify

Your 20s are flexible. Roommates, used furniture, renegotiable everything.

Your 30s and 40s are when life gets “optimized,” and your cost structure locks in. Mortgage, cars, insurance, childcare, subscriptions you forgot you had, hello.

Fixed costs don’t just reduce cash, they reduce options.2) Time becomes the real currency

Convenience spending is the silent killer of wealth.

When you’re slammed, you don’t “decide” to overspend. You outsource decisions:

- Delivery instead of groceries

- Uber instead of a plan

- Paying for speed because you can’t pay with time

3) Dependents enter the chat

Kids, partners, parents, pets with premium food preferences. Your spending stops being about you, and starts being about managing a tiny economy.

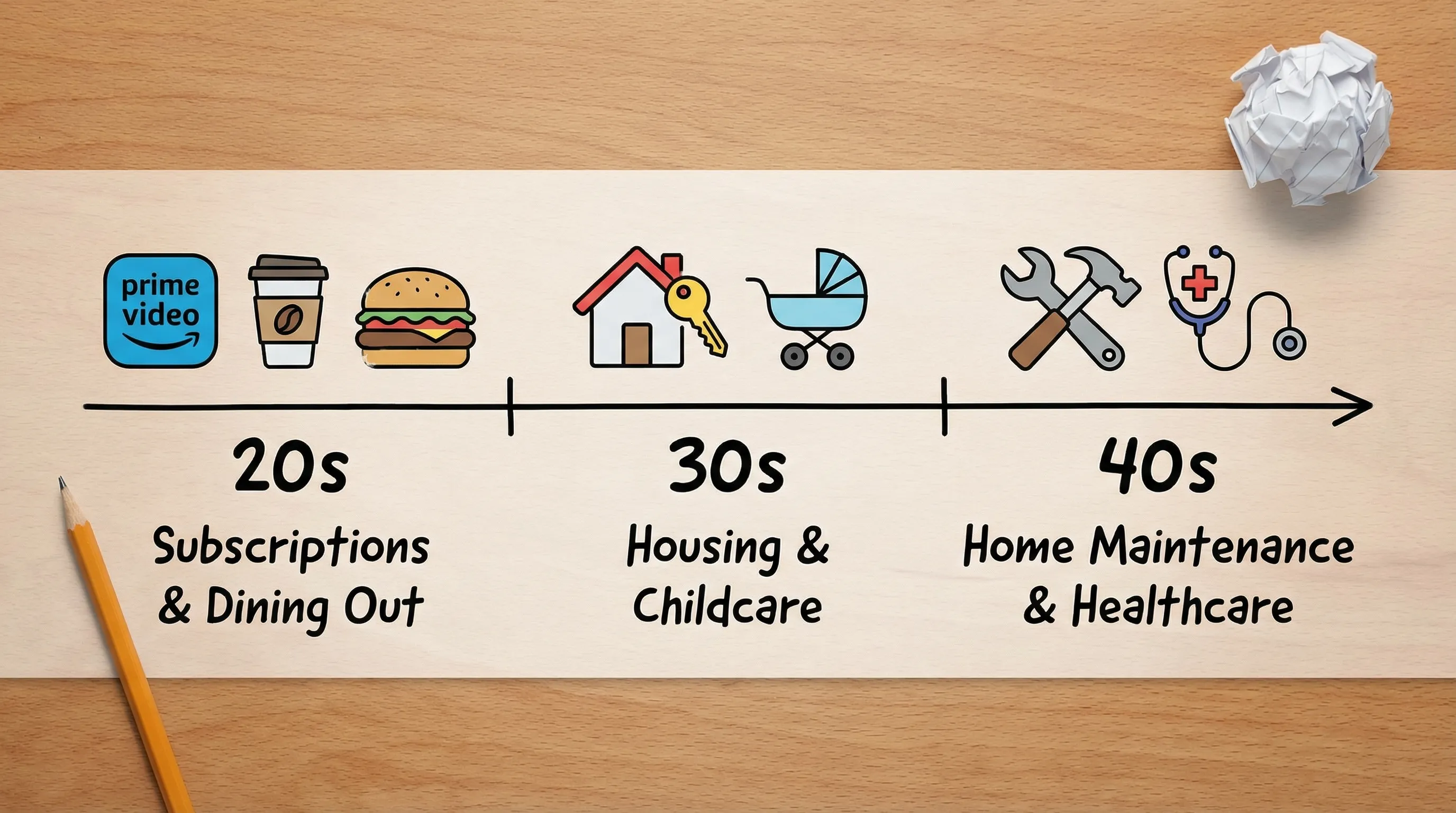

Your budget becomes a family operating system, whether you installed one or not.Your 20s: experimenting, earning, and accidentally subscribing to 14 different versions of yourself

Your 20s are financially chaotic for a reason. Income is usually lower, career is still forming, and your life changes fast.

Common 20s spending signatures:

- Housing is often a big chunk, but shared

- Transportation is unstable (car? no car? car that dies emotionally every winter?)

- “Lifestyle” spending is spiky (travel, dating, weekends that look like a Coachella sponsorship)

- Debt payments show up early (student loans, credit cards, the “I was building credit” era)

Here’s the part nobody talks about: your 20s budget isn’t about being frugal. It’s about building clean data and a simple system.

The 20s trap: confusing “I can afford it” with “I should normalize it”

That new paycheck hits and suddenly $9 lattes feel like a human right.

But the real issue is not the latte. It’s the pattern.

If you don’t set rules in your 20s, your 30s will set them for you (and your 30s rules are named “daycare” and “interest rates”).

20s playbook: build your “adult baseline” in 30 minutes

Do this once, then update monthly.

- Track the last 60 to 90 days of spending.

- Create a small set of categories you can actually maintain (8 to 12 is plenty).

- Add one “Truth Serum” category for impulse spending you want to see clearly (food delivery, bars, random Amazon).

- Set one cap that protects your future self (a savings goal, debt payoff target, or investing auto-transfer).

This is where a flexible tracker helps. FIYR is built for this kind of reality-based setup, with custom categories, transaction rules, and clean spending views that don’t pretend your life fits into 12 default buckets from 2009.

In your 20s, the goal is not perfection. It’s visibility.

Your 30s: the decade where you start paying for “stability” (and it is not cheap)

Your 30s are where spending gets serious. Not because you “got worse,” but because you started buying the big stuff.

Common 30s spending signatures:

- Housing jumps (rent upgrades, buying a home, higher utilities)

- Childcare becomes a second rent in many households

- Transportation costs stabilize (often two cars, higher insurance)

- Home-related spending appears (repairs, furniture, tools you swear you’ll use)

- Convenience spending rises because everyone is tired

The 30s trap: letting fixed costs eat your savings rate alive

People chase “adult milestones” and accidentally build a budget with no oxygen.

A bigger place, a nicer car, a few subscriptions, a couple of impulse upgrades… and suddenly you’re doing well on paper and broke in practice.

This is where savings rate becomes the scoreboard. If you’re pursuing FIRE, it’s not a cute metric, it’s the whole game.

30s playbook: the Fixed Cost Pressure Test

Once a month, calculate this:

Fixed Cost Ratio = (housing + transportation + insurance + debt minimums + childcare) ÷ take-home payIf that number is suffocating your ability to save, you don’t need “motivation.” You need to renegotiate your structure.

Practical moves that actually work in your 30s:

- Convert irregular expenses into sinking funds (car repairs, holidays, back-to-school, annual insurance).

- Label life events so you can see the real cost of decisions (example: “Baby Year 1” or “House Project Spring”).

- Use category caps that flex without breaking (your spending is seasonal, your budget should be too).

FIYR makes this easier because you can tag transactions with labels, automate messy merchants with transaction rules, and track goals with a safe-to-spend balance so you stop guessing. Guessing is expensive.

In your 30s, you’re not budgeting for fun. You’re budgeting for survival with better lighting.Your 40s: peak earnings, peak responsibilities, peak “wait, how is the roof leaking?”

If your 20s were experimentation and your 30s were structure, your 40s are often the squeeze.

Many households hit higher income years in their 40s, but also stack responsibilities:

- Bigger homes or long-term mortgages

- Teen expenses (food bills that look like catering invoices)

- Aging parents and family support

- Higher healthcare costs

- Major home maintenance (HVAC, roof, appliances doing their scheduled meltdown)

The 40s trap: lifestyle creep dressed up as “we deserve it”

You probably do deserve nice things. That’s not the point.

The point is that lifestyle creep is quiet. It doesn’t announce itself. It just becomes your new normal, and your FIRE date quietly moves out of state.

This is where tracking net worth and savings rate together becomes powerful.

- Spending tracking tells you what your life costs.

- Net worth tracking tells you whether your life is building wealth or consuming it.

If you want one “adult” money move for your 40s, it’s this: treat your savings rate like a non-negotiable bill.

40s playbook: the “Keep My Future” rule

Pick one number that you protect no matter what.

Examples:

- A monthly investing contribution

- A minimum savings rate

- A debt payoff target

Then build everything else around it.

This is also where FIRE-focused tooling matters. FIYR’s savings rate tracking, net worth view, and FIRE date calculator turn your 40s into a strategy decade, not a vibes decade.

In your 40s, the flex isn’t spending more. It’s needing less to be free.The pattern in one table (so you can stop moralizing and start planning)

Age-based spending trends are averages, not destiny, but the “default storyline” is pretty consistent.

| Age decade | Spending tends to shift toward | Common money mistake | The smartest counter-move |

|---|---|---|---|

| 20s | Convenience, social life, moving costs, subscriptions, early debt | Not noticing small recurring leaks (because “it’s only $12”) | Build clean categories, automate rules, do a monthly subscription audit |

| 30s | Housing upgrades, childcare, transportation, home setup, insurance | Locking in fixed costs before income is truly stable | Run a Fixed Cost Pressure Test, build sinking funds, protect savings rate |

| 40s | Home maintenance, healthcare, family support, lifestyle upgrades | Lifestyle creep that slowly extends your working years | Track savings rate + net worth, label big life projects, keep one protected goal |

Your age doesn’t determine your outcome.

Your system does.

The 4 metrics that make spending trends useful (instead of just interesting)

You don’t need 37 charts. You need a small scoreboard you can actually look at.

| Metric | What it tells you | Why it matters for FIRE |

|---|---|---|

| Savings rate | How much of your income you keep | It compresses your timeline more than stock-picking ever will |

| Fixed cost ratio | How “locked in” your life is | High fixed costs reduce flexibility and raise risk |

| Subscription load | How much you’re paying for set-it-and-forget-it life | Recurring charges are stealth inflation |

| Net worth trend | Whether you’re building wealth or treading water | It shows if your behavior is compounding or just coping |

If you’ve ever thought “I make decent money, why do I feel broke?”, this scoreboard will answer that in under 10 minutes.

A repeatable system: the Age-Stage Spend Audit (quarterly, 45 minutes)

This is the practical part. The part where your future self stops sending you passive-aggressive mental emails.

Step 1: Pull your last 90 days

Not last month. Last 90 days. One month lies. Three months tells the truth.

Step 2: Label your life events

Add labels for anything “not normal.”

- Travel

- Moving

- Medical

- New baby

- Home project

- Wedding

This prevents the classic mistake of thinking your lifestyle “changed” when you just had a weird month.

Step 3: Pick one leak and one lever

One leak (something to reduce) and one lever (something to increase).

Leak ideas:

- Subscriptions you forgot

- Food delivery creep

- Random shopping category bloat

Lever ideas:

- Automatic investing

- Debt payoff boost

- A fixed cost renegotiation (insurance, phone plan, car payment)

Step 4: Install one rule

Rules beat willpower. Every time.

Examples:

- “No new subscriptions without canceling one.”

- “Food delivery is capped at $X per week.”

- “Raises are split: some lifestyle, some savings.”

If you’re using FIYR, this is where custom categories, automatic transaction rules, subscription tracking, and goal tracking with safe-to-spend turn the audit from “I should do that” into “it’s already handled.”

Budgets don’t fail because people are weak. They fail because the system is optional.Final takeaway: your decade doesn’t decide your wealth, your defaults do

Your 20s teach you what you value.

Your 30s force you to choose what you’ll prioritize.

Your 40s ask the big question: are you buying freedom, or renting a lifestyle?

Spending trends by age are just the map. The win is building a tracking and budgeting system that updates as your life evolves.

Because the goal isn’t to be perfect.

The goal is to be awake.

And nothing scares a leaky budget more than an awake adult with clean data.