How to Stop Impulse Spending: A Behavioral Reset for 2026

Impulse spending in 2026 isn’t a “discipline problem.” It’s a product feature.

Your phone is a casino that fits in your pocket, your checkout button is basically a trapdoor, and your favorite brands have more data on your dopamine than your doctor has on your blood pressure.

Meanwhile, about 60% of Americans say they’re living paycheck to paycheck, and a lot of us are trying to build wealth on top of a financial floor made of Jell-O. That’s not a moral failure. That’s just math plus modern life.

So let’s fix it with something stronger than “just try harder.”

This is a simple behavioral reset built on three steps:

- Awareness (see the pattern)

- Friction (slow the click)

- Replacement habits (swap the dopamine source)

And yes, we’re doing the 24-Hour Rule, because the only thing more expensive than impulse spending is pretending it’s “self care.”

The difference between impulse spending and emotional spending (so you don’t treat the wrong disease)

Impulse spending is fast. It’s reflexive. It’s “I didn’t plan this, but it’s in my cart now.”

Emotional spending is mood-driven. Impulse spending is cue-driven.

This matters because the fix is different.

- Emotional spending often needs emotional tools (stress relief, coping strategies, therapy, sleep, boundaries).

- Impulse spending needs environment design (speed bumps, defaults, rules, better triggers).

If you’ve ever said, “I’m not even sad, why did I buy that,” welcome. You’re in the right room.

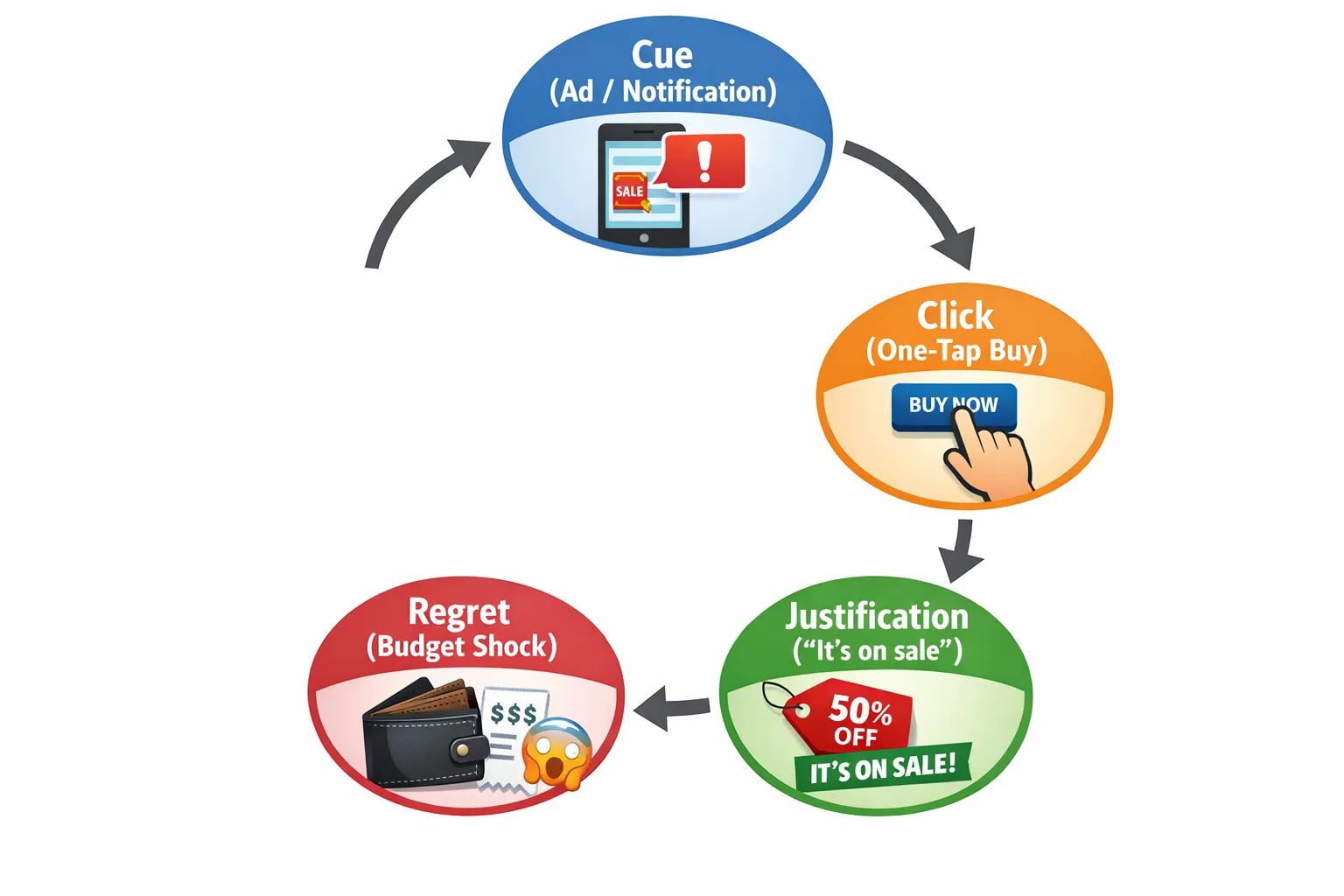

Here’s the part nobody talks about: impulse spending is often your brain responding perfectly to a system designed to exploit it.

A quick story: “I swear it was on sale”

Meet Alex. Solid job. Wants to do FIRE “eventually.” Has a 401(k). Uses a budgeting app (or used to, until Mint vanished like your free trial after day 6).

Alex’s problem wasn’t big purchases. It was the tiny “harmless” ones:

- The $18 lunch because “I didn’t pack anything.”

- The $37 “daily deal” gadget that becomes a junk drawer resident.

- The $9.99 subscription that “might be useful.”

Nothing individually catastrophic.

But the monthly total? Not cute.

Alex finally pulled transaction data and discovered the truth: the budget didn’t have leaks, it had a sprinkler system.

That’s impulse spending: death by a thousand dopamine pings.

The 2026 impulse spending engine (what you’re actually up against)

Impulse spending habits thrive in three conditions:

1) Zero friction checkout

One-click buying is convenient the same way a waterslide is convenient. You don’t “decide” to slide. You just commit your entire body to gravity.

2) Algorithmic temptation

Your feeds are not neutral. They are personalized persuasion machines.

3) Money fog

When you don’t have clean visibility, you can’t feel the impact. That’s how you end up thinking you’re “basically fine” while your credit card balance is writing fan fiction.

CNBC reports that many Americans are stressed about finances, and a meaningful share carry credit card debt, with some going deeper month after month (source). This isn’t just vibes. It’s structural.

Now the fix.

The Behavioral Reset: awareness → friction → replacement

Step 1: Awareness, spot the pattern (not the shame)

Impulse spending doesn’t respond to guilt. Guilt is just expensive entertainment.

Awareness means you can answer one question with accuracy:

“What exactly keeps hijacking my money?”#### The 7-day “Impulse Snapshot”

For the next 7 days, track these three things for every unplanned purchase:

- What it was (item or merchant)

- When it happened (time and day)

- Why now (the cue, not your life story)

Common cues look like:

| Cue type | What it looks like in real life | What to track |

|---|---|---|

| Convenience cue | “I’m already here, might as well…” | Location-based merchants, quick stops |

| Scarcity cue | “Limited drop” or “sale ends tonight” | Promo emails, TikTok Shop, flash sales |

| Boredom cue | Scroll, add to cart, repeat | Late-night transactions, weekend spikes |

| Bundle cue | “Free shipping over $50” | Cart inflation purchases |

| Identity cue | “This is the new me” purchases | New hobby spends, wardrobe overhauls |

The goal is not to become a monk. The goal is to become a detective.

#### Make your spending data snitch (in a helpful way)

This is where a modern tracker earns its keep.

In FIYR, you can make awareness easier by:

- Creating a custom category or category group like “Impulse” or “Unplanned”

- Using labels (example: “Late Night Scroll,” “Target Run,” “TikTok Made Me”) so you can see patterns, not just totals

- Setting transaction rules to automatically tag common merchants where impulse buys happen

When your data is clean, your decisions get mean (in a good way).

Quotable truth: If you can’t see it, you can’t stop it.Step 2: Friction, make buying slightly annoying again

Impulse spending dies when you add time and effort.

Not a lot. Just enough to interrupt the autopilot.

Think of friction like putting your wallet on a high shelf. You can still reach it, but now your brain has time to ask, “Do I really want this, or am I just bored?”

#### Your 2026 Friction Menu (pick 2, not 12)

You don’t need a total lifestyle overhaul. You need two speed bumps that actually stick.

Friction option A: Remove saved cards from shopping appsMake your future self type numbers like it’s 2009.

Friction option B: Turn off shopping notifications and promo emailsYour inbox is not a mall. Unsubscribe like it’s cardio.

Friction option C: Add a category cap for your biggest impulse zoneNot “spend less.” A real cap.

Friction option D: Create an “impulse allowance” line itemYes, permission. With a fence.

Because the most dangerous budget is the one that pretends you’re a robot.

The 24-Hour Rule Guide (the one you’ll actually use)

The 24-Hour Rule is not about deprivation. It’s about delayed consent.

You can buy the thing. Just not right now.

#### Set your threshold

Pick a number that creates pause without being ridiculous:

- $25 if your leaks are death-by-Amazon

- $50 if you’re a “little treat” professional

- $100 if you mostly impulse-buy “adult toys” (headphones, kitchen gadgets, “productivity” gear)

Write it down. The rule is only real if it’s explicit.

#### Define what’s exempt

Exemptions keep the rule from collapsing on day three.

Common exemptions:

- Groceries within your weekly plan

- Required household items you already budgeted for

- Replacements for true necessities (example: your charger died, not “I want a MagSafe aesthetic moment”)

#### The 24-hour script (use this verbatim)

When you want to buy something:

- “If I still want this tomorrow, I can buy it.”

- “If this is truly a good deal, there will be another good deal.”

- “I don’t need to decide now. I need to decide well.”

Your brain will complain. That’s fine. Your brain also thinks a second dessert is “basically wellness.”

#### The 3-question test (tomorrow)

After 24 hours, ask:

- Would I buy this at full price?

- Where will it live in my life, physically or digitally?

- What am I not funding if I fund this? (Debt payoff, emergency fund, investing, your FIRE date)

If you pass, buy it guilt-free. If you fail, you just bought yourself something better: control.

#### Make it automatic with a “Wish List” holding zone

Instead of relying on memory (a known liar), create a single place to park impulses.

- Notes app folder

- A “Wishlist” cart you don’t check out

- A spreadsheet if you’re the kind of person who enjoys suffering

Bonus move: in FIYR, label the purchase before you buy it (example: “Wishlist 24H”). If you later buy it, you can measure how many impulses survived the delay.

Quotable truth: A 24-hour delay turns “need” into “nice idea.”Step 3: Replacement habits, feed the craving without feeding your cart

Here’s where most people faceplant: they try to remove spending without replacing the feeling.

Impulse spending often delivers:

- Novelty

- Control

- Reward

- Relief from boredom

So you need replacement behaviors that hit the same psychological buttons, with less financial damage.

#### The Replacement Habit Library (steal these)

Match the replacement to the cue.

If the cue is boredom (scrolling):Do a 5-minute “dopamine swap.”

- Walk outside and listen to one song

- 20 pushups or a short stretch

- Text a friend a meme (free entertainment is still entertainment)

Turn buying into researching.

- Add it to the wishlist

- Set a price alert

- Read one negative review on purpose

Buy the behavior first.

- Want to be a runner? Run 3 times before buying the $180 shoes.

- Want to be a home chef? Cook 5 meals before buying the $300 pan.

Do the “equal and opposite deposit.”

- If you buy the $40 thing, transfer $40 to savings

- Or invest $40

This works because it satisfies the reward craving while building momentum toward the life you actually want.

Quotable truth: Don’t delete the craving, redirect it.

The 2026 Impulse Reset Plan (simple, repeatable, not cringe)

Week 1: Awareness week (no behavior changes required)

Your job is to observe, not “be good.”

- Tag unplanned spending as it happens

- Add a label for the cue (bored, sale, convenience, identity)

- At the end of the week, identify your top two impulse merchants or categories

This week is about building truth. Truth is the beginning of freedom, and also the beginning of “wow, I spend a lot at that one place.”

Week 2: Add two frictions

Pick two from the friction menu and commit.

Make one digital (cards removed, notifications off) and one financial (cap or allowance).

If you want a tool-assisted version, FIYR makes this smoother because you can:

- Set custom categories and category groups that reflect your real temptations

- Use transaction rules to keep impulse merchants categorized consistently

- Watch your safe-to-spend and category balances without mental math

Week 3: Install replacement habits (one per cue)

For each of your top cues, choose one replacement habit. You’re building reflexes.

Example pairing:

| Your top cue | Your replacement habit |

|---|---|

| Late-night scroll | 5-minute walk + wishlist (no checkout) |

| Flash sales | Price alert + read one negative review |

| “I deserve it” | Equal and opposite deposit |

Week 4: Tie it to something bigger than willpower

Impulse spending gets weaker when it’s forced to compete with a goal you care about.

Track one of these:

- Savings rate

- Debt payoff progress

- Net worth trend

- Your projected FIRE timeline

Because nothing kills a random purchase faster than realizing it’s borrowing against your future freedom.

Quotable truth: Your cart has a vote, but your goals should have veto power.How FIYR fits in (without turning your life into a spreadsheet cult)

Impulse control is easier when your money system is:

- Accurate (transactions are categorized cleanly)

- Fast (you can check the real damage in seconds)

- Flexible (your categories match your actual life)

FIYR helps you run this reset in a practical way by giving you:

- A full spending tracker with customizable categories

- Rules to auto-catch common impulse merchants

- Labels for experiments like “24-Hour Rule” or “No-Scroll Week”

- Subscription tracking so your “tiny purchases” don’t quietly become monthly taxes

- Savings rate and FIRE projections so you can connect today’s restraint to tomorrow’s options

Not as a guilt machine. As a scoreboard.

Frequently Asked Questions

Does the 24-Hour Rule actually work for impulse spending? Yes, because impulse spending relies on urgency. A 24-hour delay breaks the urgency spell and forces your brain to re-evaluate with less emotional and algorithmic pressure. What if I forget what I wanted to buy after 24 hours? Congratulations, you just discovered the difference between a “need” and a “moment.” Use a wishlist holding zone so you don’t rely on memory. Should I use a strict no-spend challenge instead? Short no-spend challenges can be useful, but they often snap back. The awareness → friction → replacement model is designed to be sustainable, not heroic. How do I stop impulse spending online specifically? Remove saved payment methods, kill shopping notifications, unsubscribe from promo emails, and use the 24-Hour Rule with a wishlist. Online impulse spending thrives on speed, so slow it down. Can tracking really change impulse spending habits? Yes, because visibility changes behavior. When you can clearly see where impulse spending shows up (merchants, times, categories), you can target fixes instead of relying on vague willpower.Your next move: run the reset, then make it stupidly easy to maintain

Impulse spending doesn’t require a new personality. It requires a better system.

If you want the simple version, start tonight:

- Track unplanned purchases for 7 days

- Pick two frictions

- Use the 24-Hour Rule for anything over your threshold

Then let your money tracker do what it’s supposed to do: reduce chaos.

FIYR is built for this kind of real-world behavior change, with clean spending tracking, flexible categories, rules, labels, subscription visibility, and FIRE-focused insights that connect today’s choices to long-term freedom. Check out FIYR at blog.fiyr.app and explore more systems like this in the Financial Independence and Early Retirement archive.

Because the goal isn’t to “stop spending.”

The goal is to stop spending like your phone is driving.