How to Set Financial Goals 2026: Targets, Metrics, and Momentum

Your 2026 financial goals probably sound like this:

- “Save more.”

- “Pay off debt.”

- “Stop buying nonsense online at 11:47 pm.”

Classic. Vibes. Inspirational. Completely un-executable.

Meet Sarah. She starts January with a fresh notes-app manifesto: “This is my year.” By February, she’s accidentally subscribed to three streaming services she doesn’t remember choosing, her credit card bill looks like a CVS receipt, and her “goal” has become a mood.

And she’s not alone. A CNBC report citing a LendingClub survey found about 60% of Americans are living paycheck to paycheck. Translation: most people are doing financial parkour just to make rent, and “max out your Roth” sounds like a joke told by someone with a boat. (Source)

So let’s do this the adult way: targets, metrics, momentum. Not motivation. Not manifesting. Not a vision board with a Lambo.

The 2026 goal-setting truth nobody likes

A financial goal is not a sentence. It’s a system.

Most goals fail for one of three reasons:

1) No target (you can’t hit “more”).

2) Wrong metric (you track what’s easy, not what matters).

3) No momentum loop (you check in once a month, like it’s a dental cleaning).

Fix those three and you stop “trying to be good with money” and start running your money like a product. With KPIs. With feedback. With fewer surprises.

Quotable takeaway: If your goal can’t be measured, it’s not a goal, it’s a wish with good branding.

Step 1: Turn “goals” into targets using the OKR method (yes, like grown-ups)

OKRs are used by companies because they work. And your finances are basically a small, chaotic startup with one employee (you) and a lot of invoices.

- Objective: the “why” (plain English, slightly emotional)

- Key Results: the scoreboard (numbers that prove you won)

- Actions: the moves (habits, automations, constraints)

Here are examples that don’t waste your time:

| Objective (O) | Key Results (KR) | What you actually do weekly |

|---|---|---|

| Stop feeling financially fragile | Build cash buffer to 1 month of essentials, cut overdrafts to $0 | Weekly cash check, automate payday transfer |

| Kill high-interest debt | Pay off Card A, reduce total interest paid vs last year | Avalanche payments, freeze new card charges |

| Buy future freedom | Hit a 20% savings rate average for 6 months | Automate investing, cap “chaos categories” |

| Make money less annoying | Reduce uncategorized spending to under 2% | Use rules, review “Needs Review” bucket |

Notice what’s missing: “be better.”

Quotable takeaway: Your objective is the headline, your key results are the receipts.

Step 2: Pick metrics that actually move your life (not just your charts)

In 2026, you can track everything. That’s the problem.

You want a mix of:

- Lagging metrics: results (they change slowly, but they’re the truth)

- Leading metrics: behaviors (they change fast, and they cause the results)

If you only track lagging metrics, you learn too late. If you only track leading metrics, you feel productive while nothing improves.

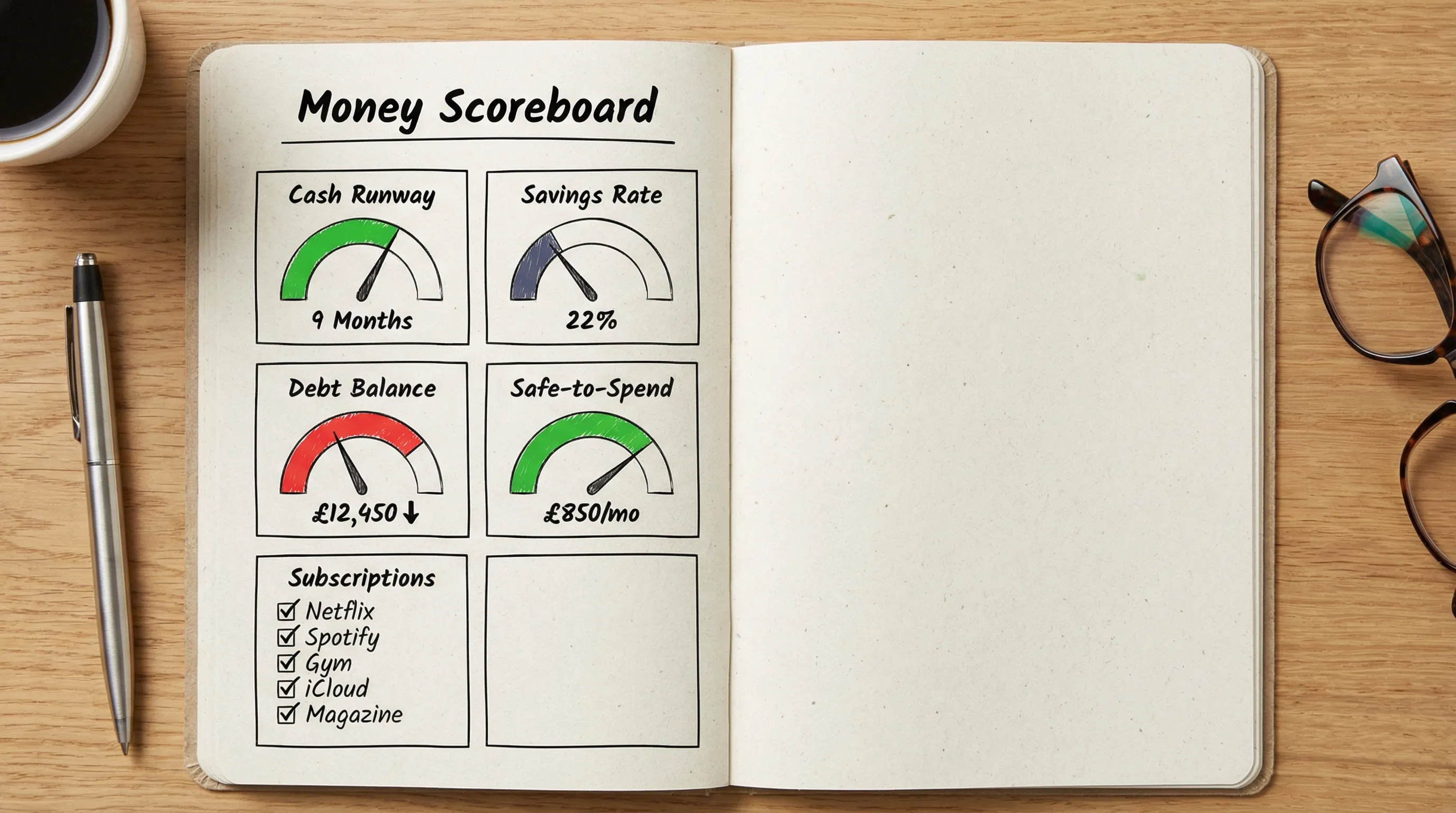

The “Money Scoreboard” (keep it simple, keep it ruthless)

Here’s a practical mix you can run all year without losing your mind.

| Metric | Type | Why it matters | How to measure it |

|---|---|---|---|

| Cash runway (months) | Lagging | Prevents panic, debt spirals, bad decisions | (Cash reserves) ÷ (monthly essentials) |

| Savings rate (%) | Lagging | Compresses your timeline to freedom | Savings ÷ take-home income |

| High-interest debt balance | Lagging | Interest is negative compounding, the evil twin | Total balances above your chosen APR threshold |

| Weekly safe-to-spend | Leading | Turns “budget” into a daily decision | Weekly allowance after bills, goals, and buffers |

| Subscription count and monthly total | Leading | Subscriptions multiply like rabbits | Count + total recurring charges |

Quotable takeaway: What gets tracked gets tamed. What gets ignored gets expensive.

Step 3: Set 2026 targets with stupid-simple math

Targets should be personal, but not random. So here are clean formulas and realistic ranges you can tailor.

Target A: Cash runway (because life loves plot twists)

Start with monthly essentials: housing, utilities, groceries, insurance, minimum debt payments, transportation.

- Starter target: 2 weeks of essentials

- Solid target: 1 month of essentials

- Stronger target: 3 months (especially for variable income)

Formula:

Cash runway (months) = Cash reserves ÷ Monthly essentialsIf your essentials are $3,500/month and you have $7,000 set aside, you have 2 months of runway.

This goal is underrated because it’s not sexy. Neither is oxygen. You still need it.

Target B: Savings rate (the FIRE-friendly metric that doesn’t care about your excuses)

If you’re pursuing FIRE (or just “retire without working until you die”), savings rate is a monster lever.

Quick conversion:

Monthly savings target ($) = Take-home pay × Target savings rateExample: $6,000 take-home

- 10% = $600/month

- 20% = $1,200/month

- 30% = $1,800/month

The magic is not the number, it’s the consistency. A boring 15% done for 12 months beats a heroic 40% done for 6 weeks.

Target C: Debt payoff (pick a line in the sand)

If you carry high-interest debt, your first 2026 “investment” is paying it off. That interest rate is a guaranteed return you don’t have to pray for.

Set a target like:

- Pay off one specific card

- Or reduce total high-interest balances by a fixed dollar amount

- Or set a “debt-free date” and work backward

Simple planning formula:

Months to payoff (rough) = Balance ÷ Monthly extra paymentNot perfect (interest exists), but good enough to design the plan.

Target D: Net worth change (focus on delta, not ego)

Net worth targets can get weird fast because markets move and your brain turns it into self-worth.

Instead, aim for net worth delta, driven by what you control:

Net worth delta ≈ (Annual savings) − (Debt reduction) + (Market movement)You don’t control market movement. You control your cash flow, debt drag, and consistency.

Quotable takeaway: Your targets should be math, not astrology.

Step 4: Build momentum with a cadence (the part that makes goals real)

Motivation is a liar. Cadence is a professional.

Here’s the momentum loop that works in real life, even if you have kids, deadlines, or a brain that turns to mush after 8 pm.

Weekly (12 minutes): the “Money Standup”

Do this once a week, same day, same time. No drama.

- Check safe-to-spend for the next 7 days

- Review top 5 spending categories (not all of them, you’re not an accountant)

- Scan subscriptions or recurring charges for anything suspicious

- Make one adjustment (cap a category, move money to a goal, cancel one thing)

The goal is not perfection. The goal is staying awake at the wheel.

Monthly (25 minutes): close the month like a CFO

Once a month, do a clean “close.”

- Confirm big bills posted correctly

- Reconcile debt balances (credit cards, loans)

- Update net worth values you track manually

- Decide one move for next month (one, not twelve)

Quarterly (45 minutes): reset targets, not your personality

Every quarter:

- Raise targets that are too easy

- Rebuild targets that were fantasy

- Adjust for life changes (new job, new rent, new baby, new “why is my car making that sound”)

Quotable takeaway: Goals don’t need more intensity, they need more check-ins.

Step 5: Make it easier with automation (because you have a life)

The dirty secret of personal finance is that most people don’t fail because they’re lazy. They fail because their system requires daily willpower and perfect memory.

Automation is how you win while being human.

What to automate first

Focus on the stuff that silently ruins progress:

- Transaction categorization so your data isn’t a swamp

- Recurring bills and subscriptions so they stop sneaking around

- Goal funding (payday transfers) so saving happens before spending

This is where a modern tracker matters. Former Mint users learned the hard way: “free” often means “fragile.”

With FIYR, the idea is straightforward: connect your accounts, track income and expenses, use custom categories and transaction rules to keep data clean, then watch your metrics like savings rate and net worth without doing spreadsheet cosplay.

Quotable takeaway: If your system needs daily heroics, it will die the first time life gets busy.

A quick 2026 template: your “one-page money plan”

Copy this into a note, a doc, or the back of an envelope you’ll lose in a week.

1) My 2026 objective (one sentence)

Example: “Build stability and buy freedom by controlling cash flow and eliminating debt.”

2) My three key results (numbers)

Pick three, max. More than that and you’re just collecting quests.

- Cash runway: ____ months by ____

- Savings rate: ____% average by ____

- High-interest debt: $____ by ____

3) My two guardrails (rules)

Examples:

- Subscription cap: $____/month

- Convenience spending cap (delivery, rides, impulse buys): $____/week

4) My weekly cadence

“Every Sunday at 5 pm, I do a 12-minute Money Standup.”

That’s it. Boring. Effective. The whole point.

Bonus: If you need an income goal, make it specific (and not cringe)

A lot of people set savings goals without an income plan. That’s like trying to win a race while refusing to use your legs.

If you’re self-employed, a creator, or just tired of your paycheck doing the bare minimum, set an income target like:

- “Add $500/month in predictable side income by June.”

- “Increase my average monthly income floor to $X by Q3.”

One real-world path some people take is reselling liquidation inventory. If you go that route, you’d look for reputable sources of truckloads or overstock inventory like bulk pallets for sale and then treat it like a business, track costs, shipping, and profit like an adult.

Not a get-rich-quick scheme. A spreadsheet-and-sweat scheme. Much less glamorous, much more real.

Quotable takeaway: Cutting expenses is powerful, but adding income is often faster and way less emotionally exhausting.

Frequently Asked Questions

How many financial goals should I set for 2026? Three key results is the sweet spot. One is too few (life has multiple fronts), five is too many (you will forget them by February). What’s the best metric to track weekly? Safe-to-spend. It converts your long-term plan into a short-term decision, which is where money actually gets spent. Should I focus on savings or debt payoff first? If you have high-interest debt, prioritize it while still building a small cash buffer so you don’t keep swiping the card during emergencies. How do I set targets if my income is irregular? Use an income floor (a conservative monthly baseline), build a buffer, and set targets based on averages, not your best month. Do I need a budgeting app to do this? You need accurate data and a review cadence. An app just makes it dramatically easier to track, categorize, and see progress without manual busywork.Ready to make 2026 the year your goals stop being vibes?

If you’re serious about targets, metrics, and momentum, your next step is boring in the best way: get clean data and a simple scoreboard you’ll actually look at.

FIYR was built for exactly that, a modern alternative to Mint, Monarch, Copilot, Rocket Money, and Quicken that focuses on flexible budgeting, spending tracking, net worth, savings rate, subscriptions, and FIRE-focused insights.

Set it up once, automate the noise (categories, rules, recurring charges), then run the weekly standup. Your future self doesn’t need a motivational speech. They need a system.

Check out FIYR at https://blog.fiyr.app and start turning 2026 goals into measurable wins.