FATFIRE Explained: What It Really Means and Whether It Fits Your Goals

Most people hear FATFIRE and picture a yacht named Compound Interest. Reality check, it looks a lot more like first-class optionality than first-class tickets. If regular FIRE buys your time back, FATFIRE buys your time plus margin. You stop asking, can we afford it, and start asking, do we want it.

Here is the part nobody explains clearly. The meaning of FATFIRE is not private jets. It is funding an above-average lifestyle entirely from your investments, usually six-figure annual spending, without needing a paycheck.

What FATFIRE really means

Plain English definition: FATFIRE is financial independence at a higher lifestyle level. You cover comfortable to luxurious annual spending from your portfolio, not from work. In practice, that typically means annual spending of roughly 120,000 to 300,000 dollars or more for a household, after tax, adjusting higher in expensive cities and lower in cheaper ones.

A quick sanity frame:

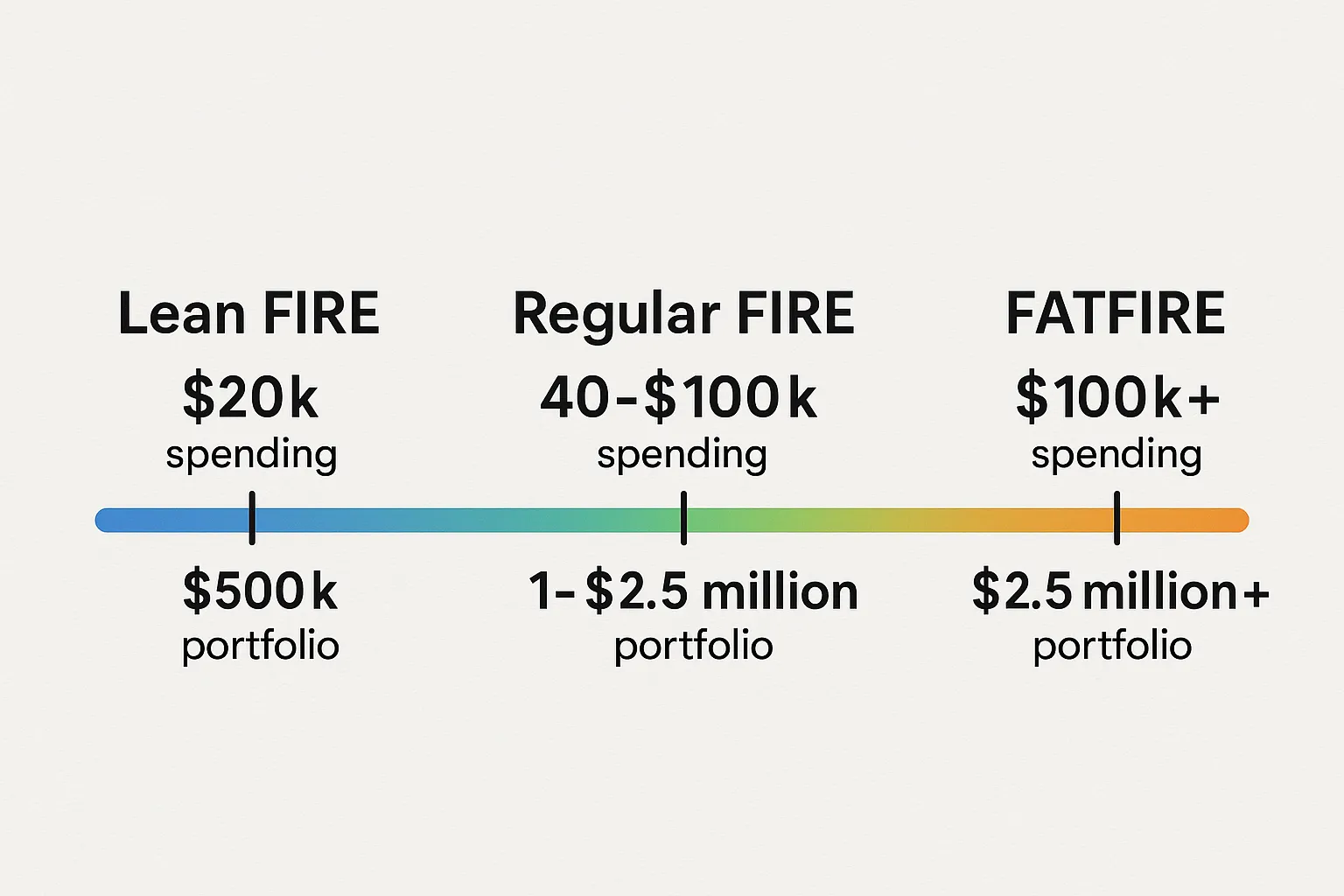

- Lean FIRE, minimal and optimized spending, often 25,000 to 40,000 dollars per year.

- Regular FIRE, middle-class comfort, often 40,000 to 100,000 dollars per year.

- FATFIRE, upgraded comfort and choice, often 120,000 to 300,000 dollars plus per year.

None of these are commandments. They are ranges. Your version depends on location, family size, tastes, and what you call a great Tuesday.

Why FATFIRE is even a conversation

The contrast is stark. Around 60 percent of Americans still live paycheck to paycheck and only 45 percent report having an emergency fund, according to reporting summarized by CNBC in late 2023. Three in five carry credit card debt, with an average balance near 5,875 dollars, and many go deeper each month. When the median household income sits near the mid 70,000s, per the U.S. Census Bureau, wanting a six-figure retirement spend can sound delusional. It is not delusion. It is math plus strategy.

When you define the lifestyle and price it accurately, the path gets less mysterious. Not easy, but clear.

How much money you need for FATFIRE

Use the same framework as standard FIRE, just with larger numbers. The classic Rule of 25, withdraw about 4 percent of your portfolio per year, is a starting point, not a law. If you want a deeper dive on safe withdrawal math and the Trinity Study, read our guide to the 4 percent rule at Unlocking the 4% Rule.

- FI number, quick calc: annual spending multiplied by 25. That assumes a 4 percent withdrawal.

- Build a safety margin: consider 3.5 percent if you want extra resilience or expect high healthcare costs. That is spending multiplied by 28 to 30.

- Taxes matter: if most of your money sits in pre-tax accounts, gross up for the taxes due on withdrawals.

Example targets:

- Spend 160,000 dollars per year, FI number about 4.0 to 4.8 million dollars (4 percent to 3.3 percent).

- Spend 220,000 dollars per year, FI number about 5.5 to 6.9 million dollars.

- Spend 300,000 dollars per year, FI number about 7.5 to 9.0 million dollars.

Translation, FATFIRE typically requires a portfolio in the mid 7 figures. The good news is that the levers are the same ones you already know, savings rate, investment returns, and time. The better news is that high earners can compress the timeline dramatically with tax strategy and aggressive savings.

What lifestyle does FATFIRE actually buy

Think comfort, health, and freedom of choice, not gold-plated doorknobs.

- Housing in a desirable neighborhood, owning or renting without stretching.

- Robust healthcare and proactive care, especially pre-Medicare.

- Frequent travel without playing the points Tetris every single time.

- Quality experiences for kids or grandkids, camps, lessons, trips.

- Margin for hobbies that cost real money, cycling gear, sailing, aviation lessons, a project car.

Meet Maya and Eric. Two kids, Austin area, both worked in tech. They spend about 180,000 dollars per year. Their Tuesdays include school drop-off, a long workout, a late lunch date, and a 3-hour work block on a passion project that may or may not make money. That is FATFIRE in the wild. Not flashy. Just decisive.

Simple FATFIRE budget examples

These are illustrative, not prescriptive. Taxes shown are the estimated taxes on withdrawals to fund the spending. Your tax picture can differ a lot.

| Scenario | After-tax annual spending | Est. taxes on withdrawals | Pre-tax withdrawals | Portfolio target at 4% | Portfolio target at 3.5% |

|---|---|---|---|---|---|

| HCOL city comfort, think SF, NYC, coastal | 220,000 | 30,000 | 250,000 | 6.25M | 7.14M |

| MCOL suburb, think Austin, Raleigh, Denver metro | 160,000 | 20,000 | 180,000 | 4.50M | 5.14M |

| LCOL or geo-arb, think Boise, Tulsa, or part-time abroad | 130,000 | 15,000 | 145,000 | 3.63M | 4.14M |

A closer look at the MCOL example, annual, rough but realistic:

- Housing, 48,000 dollars

- Healthcare premiums plus out-of-pocket, 18,000 dollars

- Food and dining, 24,000 dollars

- Travel, 24,000 dollars

- Transportation, maintenance, insurance, 10,000 dollars

- Kids, education, activities, 12,000 dollars

- Fitness, hobbies, memberships, 6,000 dollars

- Giving and gifts, 8,000 dollars

- Everything else, phones, internet, utilities, clothes, 10,000 dollars

- Total after-tax spend, 160,000 dollars

If your eyebrows just went up at healthcare, welcome to America. Price it honestly.

FATFIRE vs FIRE vs Lean FIRE, side by side

| Style | Typical annual spend | Portfolio, 4% rule | Lifestyle snapshot | Who it fits |

|---|---|---|---|---|

| Lean FIRE | 25k to 40k | 625k to 1.0M | Minimalist, optimized housing, heavy DIY, tight travel | Solo optimizers, geo-arb lovers, low-cost cities |

| Regular FIRE | 40k to 100k | 1.0M to 2.5M | Solid middle-class comfort, smart travel, measured splurges | Broad middle, families in MCOL markets |

| FATFIRE | 120k to 300k plus | 3.0M to 7.5M plus | High comfort, better neighborhoods, robust healthcare, big travel | High earners, business owners, dual-income pros |

If you love the idea of margin, experiences, and saying yes to big memories without spreadsheet guilt, FATFIRE might be your lane. If the numbers feel like overkill, regular FIRE is already life-changing. For a deeper compare of Lean versus Fat, we break it down here, Lean FIRE vs Fat FIRE.

Pros, cons, and tradeoffs that actually matter

Pros:

- Optionality, fewer money-driven compromises on where you live, how you spend time, and when you help others.

- Resilience, higher budget means more buffer for healthcare, housing surprises, and inflation shocks.

- Identity freedom, separate money from meaning so your work becomes choice, consulting, mentoring, creating.

Cons:

- Timeline, bigger portfolio targets take longer. No surprise, just math.

- Tax drag, higher withdrawals can push you into higher brackets and trigger IRMAA surcharges in Medicare later.

- Lifestyle creep, tastes rise faster than you think. Guardrails are mandatory.

- Sequence risk, the bigger the absolute withdrawal dollars, the spicier the first 5 years of market returns. Read up on sequence risk and guardrails in our 4 percent guide, Unlocking the 4% Rule.

Tradeoff, FATFIRE is not a pass to stop planning. It is a license to make bigger plans on purpose.

The math, cleaned up

- FI number, target spend multiplied by 25 to 30, pick lower multiple if flexible, higher if conservative.

- Savings rate, the single biggest accelerator. Savings rate equals total savings divided by take-home pay. For a quick playbook on boosting it, start with Boost Your Savings Rate.

- Sequence-aware withdrawals, consider a guardrails approach instead of a fixed 4 percent. Spend a band around a target and adjust when markets move. We explain the logic in our 4 percent piece.

If you want a full primer on FIRE mechanics, the philosophy and math live here, Unlocking FIRE.

The FATFIRE Fit Test

Use this to pressure test your goals before you chase a number.

1) Lifestyle clarity, Write a perfect Tuesday and perfect month. Price each line.

2) Non-negotiables, Healthcare, proximity to family, school choices, travel cadence. Which are fixed vs flexible.

3) Place matters, Decide HCOL, MCOL, LCOL, or geo-arb rotation. Housing can swing your budget by 30 to 60 percent.

4) Work optional or work-free, Some people still consult because they want to. That trims the portfolio requirement.

5) Kids and college, Model peak kid years separately from empty nest years. Spending is not flat.

6) Tax map, Pre-tax vs Roth vs taxable accounts. The mix changes your gross-up.

7) Risk tolerance, If a 25 percent drawdown would wreck your sleep, use a lower withdrawal rate and more bonds.

8) Giving and legacy, Include what you want to do for others. Money with a mission travels farther.

9) Hedonic traps, Name your splurges and set caps. Fancy is fine. Fuzzy is expensive.

10) Exit ramps, Define what happens if markets misbehave. Smaller withdrawals, temp consulting, or location pivot.

If you cannot answer these cleanly, you do not need a bigger number. You need a clearer plan.

A practical system to get to FATFIRE faster

Here is the repeatable framework that actually moves the date on your calendar.

- Design first, money second. Price the life. Build the number. Then back into the plan.

- Build an income engine. Promotions, job hops, negotiation cycles, side businesses. High earners do not stumble into seven-figure portfolios. They manufacture them.

- Target a 50 to 70 percent savings rate in your high-earning years. It is aggressive, and it is how timelines compress. Treat windfalls like accelerants, not upgrades.

- Automate investing into low-cost index funds across U.S., international, and bonds. Keep fees and taxes low. The market does the heavy lifting if you stop interrupting it.

- Max the tax buckets. 401(k)s, IRAs, HSAs, and, if offered, after-tax 401(k) to Roth conversions. Use solo 401(k)s if self-employed. See our advanced guide, Maximize Your Retirement Savings.

- Model multiple withdrawal rates. Save until 4 percent works, then keep saving until 3.5 percent feels easy. That extra buffer is real sleep.

- Set guardrails. Spending floor and ceiling, annual rebalance, and trigger rules for when to tighten or loosen the belt.

Quotable version, Your budget is not broken, your system is. Fix the system and the numbers follow.

Common mistakes to skip on your way to FATFIRE

- Underpricing healthcare, especially pre-65. Build fat lines for premiums, deductibles, and out-of-pocket.

- Treating today’s income as permanent. Bonuses evaporate. Tech cycles turn. Model downside scenarios.

- Confusing status with satisfaction. A better zip code does not fix a boring Tuesday.

- One-size-fits-all withdrawal rate. Markets change. So should you.

Light tools to make this easier

You do not need 19 spreadsheets. You need clarity and feedback loops.

- Track income, expenses, and subscriptions automatically.

- Tag spending with custom labels, New York Trip 2025, so you know the real cost of memories.

- Watch your savings rate in real time and pair it with a FIRE date projection.

FIYR is built for exactly this style of planning, flexible budgets, custom categories and rules, net worth and savings-rate tracking, and a FIRE calculator to map the date to your number. If you want to see the whole picture in one place, that is the point.

The bottom line

FATFIRE is not about flexing. It is about freedom with cushion. If regular FIRE solves money anxiety, FATFIRE solves it and then hands you a wider menu. Start with the life, price it honestly, choose your multiple, and build the system that gets you there. The day your portfolio pays for a great Tuesday, on purpose, is the day the acronym stops mattering and your life starts speaking for itself.