Budgeting in Your 30s: The ‘I Have Bills Now’ Survival Guide

Your 30s are the decade where money stops being a vibe and starts being a recurring calendar invite.

In your 20s, you could “accidentally” spend $180 at brunch and call it “networking.” In your 30s, you do that and your future self sends you an invoice. Because now you have bills. Real ones. The kind that don’t care about your personal growth journey.

Meet Jordan, 34. Solid job, decent income, thinks they’re “pretty responsible.” Then they check their transactions and realize they’re paying for:

- A gym membership they use twice a year (both times were January)

- Three streaming services, two music apps, and one “meditation” app that mostly delivers guilt

- Delivery fees that add up to a car payment, just with worse resale value

Jordan’s problem is not intelligence. It’s adult life gravity.

And here’s the uncomfortable truth: in your 30s, budgeting isn’t about “cutting lattes.” It’s about building a system that can survive the chaos.

Why budgeting in your 30s feels harder (because it is)

Your 30s are when fixed costs metastasize.

- Housing gets bigger, pricier, and comes with surprises like “roof,” “HVAC,” and “why is water coming from there?”

- Transportation becomes less “cool car” and more “reliable box that starts in winter”

- Insurance starts sounding like a boring adult tax (because it is)

- If you have kids, childcare shows up like a second mortgage with worse customer service

Also, you’re busy. Time is scarce. And modern life is engineered to turn “I’m tired” into “I deserve this” into “Why is my credit card on fire?”

Here’s the part nobody talks about: your budget didn’t get worse, your life got more expensive and more complex.

The data punch: most people are one surprise away from panic mode

About 60% of Americans are still living paycheck to paycheck, according to CNBC’s reporting on recent surveys and consumer data trends.

That means a lot of people aren’t “bad with money.” They’re just running a system with zero shock absorbers.

And the Federal Reserve’s annual Survey of Household Economics and Decisionmaking (SHED) has repeatedly shown a big chunk of adults would struggle with an unexpected expense (the classic “$400 emergency” problem). That’s not a budgeting failure, it’s a resilience failure.

Sources:

Quotable takeaway: If your budget can’t handle real life, it’s not a budget, it’s a wish.

The “I Have Bills Now” Scoreboard (4 numbers that matter)

In your 30s, you don’t need 47 categories. You need a scoreboard.

Track these four numbers and your budget goes from fragile to functional.

| Metric | What it tells you | Simple way to calculate it | What “healthy” often looks like |

|---|---|---|---|

| Fixed-cost ratio | How trapped you are by monthly commitments | (Fixed bills ÷ take-home pay) | Lower is better, many households aim under ~50% to 60% |

| Savings rate | How fast you’re buying future freedom | (Savings + investing ÷ income) | Start where you are, then push it up steadily |

| Runway | How long you can survive a job/income hit | Emergency fund ÷ monthly bare-bones spend | 1 month is a start, 3 to 6 months is a common goal |

| Subscription load | How much “tiny monthly” adds up to “big problem” | Total monthly subscriptions | If you don’t know it, it’s too high |

One-liner: Your 30s budget should be a dashboard, not a diary.

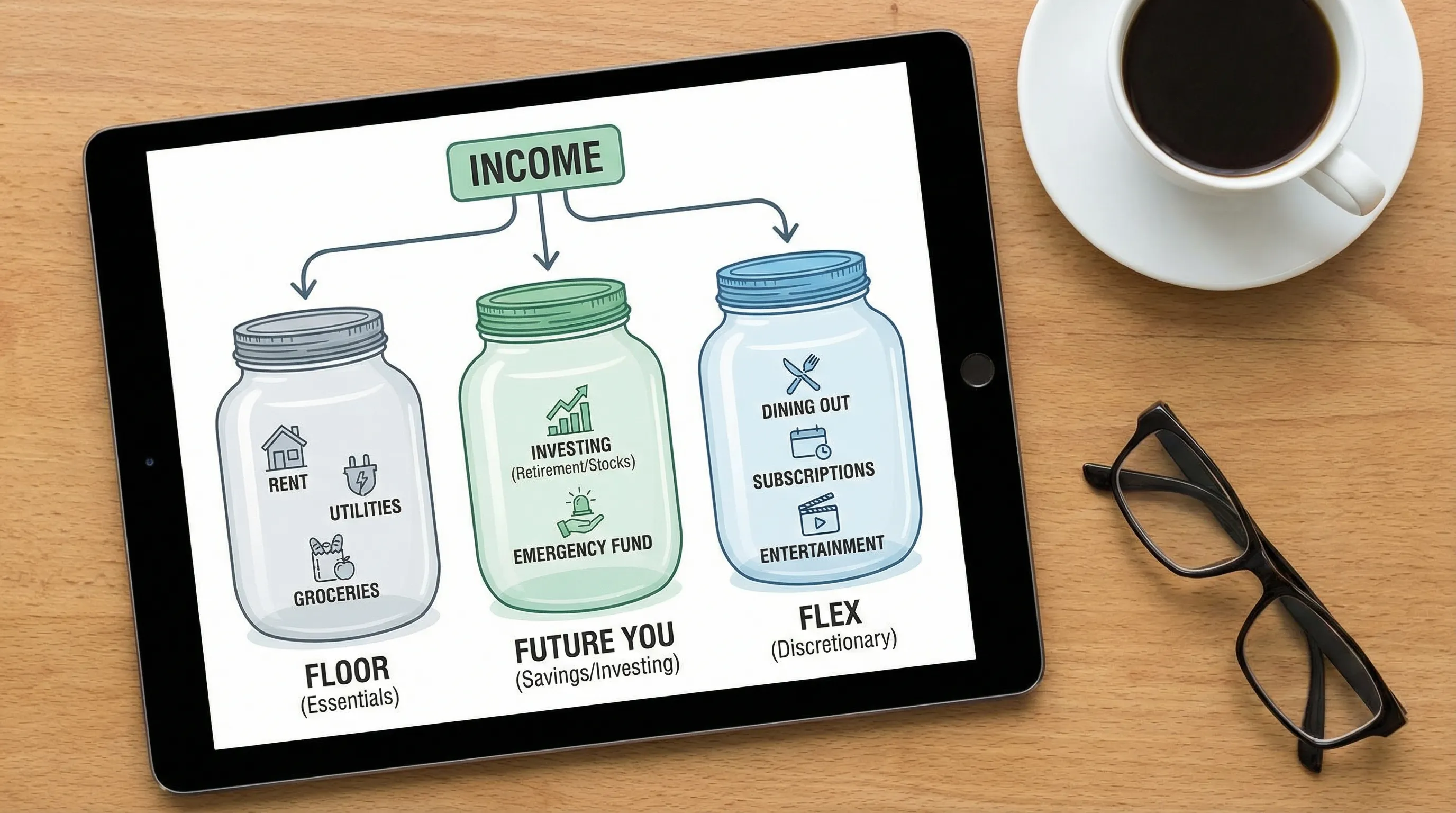

The 30s budgeting system that actually works (Bills-First, then Life)

You’re not here to become a monk. You’re here to stop getting blindsided.

Use this three-bucket structure:

1) Floor (the bills that keep your life running)

These are your non-negotiables:

- Housing (rent or mortgage)

- Utilities, insurance

- Minimum debt payments

- Groceries (real ones, not “$19.80 of sparkling water”)

- Transportation

- Childcare, if relevant

Rule: If your Floor is too big, your budget will feel like suffocation. That’s not a mindset issue. That’s math.

2) Future You (the stuff that makes you richer, safer, and less stressed)

This is where the magic happens:

- Emergency fund contributions (until your runway is real)

- Retirement/investing contributions

- Extra debt payoff (especially high-interest)

- Sinking funds (more on that in a second)

Rule: Future You gets paid before Past You buys another impulse upgrade.

3) Flex (everything else, yes including fun)

Flex is restaurants, shopping, entertainment, hobbies, travel, and “convenience spending because I’m exhausted.”

Flex is not evil. Flex is where life happens. The trick is to cap it in a way that keeps you sane and keeps you progressing.

Quotable takeaway: Bills first, future second, fun third. That’s adulthood.

The move that saves your 30s budget: “monthly-ize” the chaos

Your budget keeps “failing” because you keep pretending predictable expenses are surprises.

Examples:

- Car repairs

- Home maintenance

- Insurance premiums

- Holidays and gifts

- Annual subscriptions

- Medical and dental out-of-pocket

- Travel

These aren’t emergencies. They are appointments with your wallet.

The simple formula

Monthly sinking fund contribution = (annual cost ÷ 12)If you don’t know the annual cost yet, estimate, then adjust later. The point is to stop letting irregular expenses jump-scare you.

Here’s a starter list of classic “30s True Expenses” to set up as sinking funds:

- Home and car maintenance

- Health and medical

- Travel

- Gifts and holidays

- Professional costs (licenses, dues, conferences)

- Kid costs (activities, school stuff, birthdays)

One-liner: Your 30s budget needs shock absorbers, not inspirational quotes.

Your “safe-to-spend” number (the weekly guardrail that stops dumb decisions)

Most overspending happens because you’re using a terrible metric: bank balance vibes.

Instead, calculate a weekly safe-to-spend number for Flex.

A simple approach:

Weekly safe-to-spend = (Monthly take-home − Floor − Future You) ÷ 4.3Why 4.3? Because months are sneaky and average about 4.3 weeks.

Now you can look at a $68 DoorDash order and ask the only question that matters: “Is this coming out of my Flex allowance, or am I stealing from Future Me?”

Quotable takeaway: A budget without a safe-to-spend number is just a motivational poster with spreadsheets.

The 30-minute “Bills Now” audit (do this once, thank yourself monthly)

This is the fast, unsexy cleanup that creates instant breathing room.

Step 1: Find the money leaks

Scan the last 30 to 60 days of transactions and circle:

- Subscriptions you forgot existed

- Fees (late fees, bank fees, convenience fees)

- Convenience spending (delivery, rideshare, last-minute purchases)

You’re not looking for perfection. You’re looking for patterns.

Step 2: Pick one “chaos category” and cap it

Most people have one category that behaves like a raccoon with a credit card.

Common culprits in your 30s:

- Restaurants and delivery

- Amazon/Target “house stuff”

- Kid convenience spending

Set a cap you can actually hit. Then tighten later.

Step 3: Turn on automatic guardrails

This is where most budgets level up from “I’ll try harder” to “this runs even when I’m tired.”

Automation can look like:

- Recurring transfers to savings/investing on payday

- A subscription cap category

- Rules that consistently categorize common merchants

(Yes, this is also why modern tools beat spreadsheets and legacy apps. More on that below.)

One-liner: You don’t rise to the level of your goals, you fall to the level of your defaults.

Real life scenario: the 30s budget that doesn’t implode

Let’s go back to Jordan.

Jordan’s first pass was classic:

- Cut random stuff

- Feel deprived

- Rebound spend on Friday because “I deserve it”

So we changed the game:

- Built a Floor that included real life (including childcare and insurance)

- Added sinking funds for the predictable chaos

- Set a weekly safe-to-spend number

- Kept two “joy” categories intentionally funded (date nights and fitness)

What happened?

Jordan stopped “budgeting” and started operating a system. No guilt spirals. No end-of-month panic. Just clarity.

Quotable takeaway: The goal isn’t restriction, it’s control.

Where FIYR fits (especially if you miss Mint, but not the chaos)

A 30s budget lives or dies on two things: clean data and low friction.

FIYR is built for exactly this moment, when you want a modern replacement for Mint (and a calmer alternative to tools that feel like finance homework).

With FIYR, you can:

- Track income and expenses, with customizable categories that match your actual life (not a generic “Shopping” blob)

- Build flexible budgets and see a clear safe-to-spend signal

- Track subscriptions so “tiny monthly” doesn’t quietly eat your raise

- Track net worth (assets and liabilities) so progress is visible

- Track savings rate and project a FIRE timeline using real data

- Use labels like “New York Trip 2026” to see the true all-in cost of life events

If you’re in your 30s, the killer feature is not “pretty charts.” It’s a system you’ll still use when you’re slammed at work and someone in your house is always sick.

Frequently Asked Questions

What is the best budgeting method for budgeting in your 30s? A bills-first approach usually works best: fund your Floor (fixed bills), pay Future You (savings, investing, sinking funds), then spend what’s left in Flex with a weekly safe-to-spend number. How much should I be saving in my 30s? There’s no single perfect number, but your savings rate matters more than the label. Start with a realistic target you can hit consistently, then raise it as income grows or fixed costs shrink. Why do I feel broke even though I make more money than in my 20s? Fixed costs and convenience spending tend to grow in your 30s, and lifestyle upgrades often become subscriptions and commitments. More income plus more obligations can still equal “where did it all go?” How do I budget with kids in my 30s? Treat kid costs as part of the Floor (childcare, essentials) and create sinking funds for irregular kid spending (birthdays, activities, school costs). Then cap the “convenience” category, because that’s where budgets go to die. What should I do first if I’ve never really budgeted before? Track one month of real spending, build a simple three-bucket structure (Floor, Future You, Flex), and set one weekly check-in. Make it easy enough that you actually do it. Is a budgeting app worth it in your 30s? If it reduces friction and improves accuracy, yes. Your 30s are busy, and manual tracking tends to collapse under real life. Tools that automate tracking, subscriptions, and categorization can keep you consistent.Build a budget that survives your actual life

If your current system is a mix of bank-balance vibes, subscription amnesia, and “I’ll figure it out later,” you’re not alone. You’re just running the default settings.

FIYR helps you turn budgeting in your 30s into something calmer and more precise: track spending, set flexible budgets, monitor subscriptions, calculate savings rate, and see your net worth and FIRE trajectory in one place.

If you want to stop guessing and start steering, explore FIYR at blog.fiyr.app.