Best Wealth Tracker App for Long-Term Goals

You do not build long term wealth by glancing at a checking balance. You build it by tracking the right numbers consistently and tying every dollar to a future purpose. If you are evaluating the best wealth tracker app for long term goals like FIRE, retirement, a home purchase, or a sabbatical, the tool you choose should translate daily spending into a clear multi decade plan.

What to look for in a wealth tracker built for long term goals

Most finance apps can show yesterday’s transactions. Fewer can help you reach a 10 to 30 year goal. When you compare options, prioritize features that close the gap between cash flow today and outcomes tomorrow.

- Full money and spending tracking, with accurate categorization and clear charts

- Custom categories and category groups aligned to your life and values

- Automatic transaction rules to keep data clean with minimal effort

- Custom labels on transactions for projects and life events, for example New York Trip 2025

- Budgeting with flexible, dynamic options and a safe to spend balance

- Subscription tracking to surface and reduce recurring charges

- Net worth tracking across assets and liabilities, including custom items

- Savings rate tracking and FIRE projections that use your real numbers

- Goal tracking that shows progress and trade offs in one place

FIYR is designed around these non negotiables. It is a modern alternative to Mint and Quicken if you want more flexibility and transparency, and a simpler, more affordable approach than premium tools like Monarch Money and Copilot Money.

Why FIYR stands out for long term planners

| Capability | Why it matters for long term goals | How FIYR helps |

|---|---|---|

| Full money and spending tracker | You cannot improve what you do not measure | Tracks income, expenses, and spending habits with clear charts |

| Custom categories and groups | Aligns budgets to your values and unique life | Build custom categories and category groups, then budget the way you live |

| Automatic transaction rules | Consistency without manual work | Create rules once, FIYR applies them to future transactions |

| Custom labels on transactions | A second dimension for trips, events, or side projects | Add labels like New York Trip 2025 to see all related spend across categories |

| Budgeting with dynamic options and safe to spend | Protects goals during irregular income or seasonal costs | Set flexible budgets and always see your safe to spend balance |

| Subscription tracking | Stops silent budget leaks | Detect and review recurring charges, then cut or renegotiate |

| Net worth tracking across assets and liabilities | Progress to goals lives here | Track everything you own and owe, including custom assets and liabilities |

| Savings rate calculator and FIRE projections | Connects habits to your timeline | See savings rate trends and modeled FIRE dates with your data |

| Goal tracking | Real time accountability | Create goals and monitor progress alongside cash flow |

| Guidance and education | Better decisions, fewer mistakes | Deep dive with our library on FIRE, investing, and planning |

For a deeper primer on how to size retirement targets and timelines, start with our guides on Unlocking FIRE and the 4 percent rule. If you want to tighten monthly cash flow to accelerate results, read Boost Your Savings Rate.

A practical setup for long term success in FIYR

Use this simple flow to go from zero to a working plan in a single session.

1) Define your long term goals and amounts

- Retirement or FIRE, a target annual spend gives you a ballpark portfolio size. The 4 percent rule is a useful starting point for many retirees, see our guide on the 4 percent rule. Pair it with your preferred FIRE style from Lean vs. Fat FIRE.

- Home down payment, decide your dollar target, date, and risk tolerance.

- Debt freedom, list balances, interest rates, and a target payoff date. Compare approaches using Debt Snowball vs. Avalanche.

- Emergency fund, choose a months of expenses target with our Emergency Fund Guide.

Create these as goals in FIYR so progress is visible next to daily spending.

2) Track net worth across everything you own and owe

Add checking and savings, brokerage and retirement, and any custom assets. Add liabilities like credit cards, student loans, and mortgages. Your net worth timeline will become the most reliable scoreboard for long term progress. For investing basics and sensible asset mixes, review Index Fund Investing for Beginners and the widely used Bogleheads three fund portfolio for context.

3) Build a budget that funds your future

Create custom categories and groups that reflect your life, for example Housing, Transportation, Childcare, Health, Fun, Giving. Use FIYR’s dynamic budget options to adapt in busy months while protecting your goals. Your safe to spend balance shows how much is available after accounting for fixed bills, goals, and planned variable expenses.

4) Automate clean data with rules and labels

Set transaction rules so merchants and paychecks always land in the right categories. Layer labels for cross category views, for example New York Trip 2025 or Spring Side Project. With one label you can see total cost by category, such as Flights in Travel, Meals in Dining, and Tickets in Entertainment.

5) Inventory and trim subscriptions

Subscription tracking highlights recurring charges that no longer deliver value. Small wins compound into hundreds or thousands over years, which matters when you are chasing long term goals. The Bureau of Labor Statistics maintains current inflation data at bls.gov/cpi, a reminder that trimming recurring costs is one of the few levers you fully control when prices rise.

6) Measure your savings rate and project your timeline

Savings rate is the single most powerful variable in achieving FIRE. Track it monthly in FIYR and model your FIRE date with the app’s projections. If you need a quick refresher and tactics to lift this number, use Boost Your Savings Rate. For advanced retirement contribution strategies, explore Maximize Your Retirement Savings.

7) Review and rebalance on a schedule

Once a quarter, review your net worth trend, savings rate, big category variances, and contributions. If you invest through index funds, periodic rebalancing can keep risk in line with your plan. The Federal Reserve’s Survey of Consumer Finances provides helpful context for household balance sheets over time at federalreserve.gov/econres/scfindex.htm.

Key metrics to watch in FIYR

- Savings rate, your monthly percentage saved or invested, then your 12 month average

- Net worth delta, change month to month and year over year

- Goal funding rate, what percent of planned contributions you actually made

- Top three spending categories, and whether they match your values

- Subscription count and total, reviewed every quarter

- Safe to spend, consistently positive and aligned with upcoming cash needs

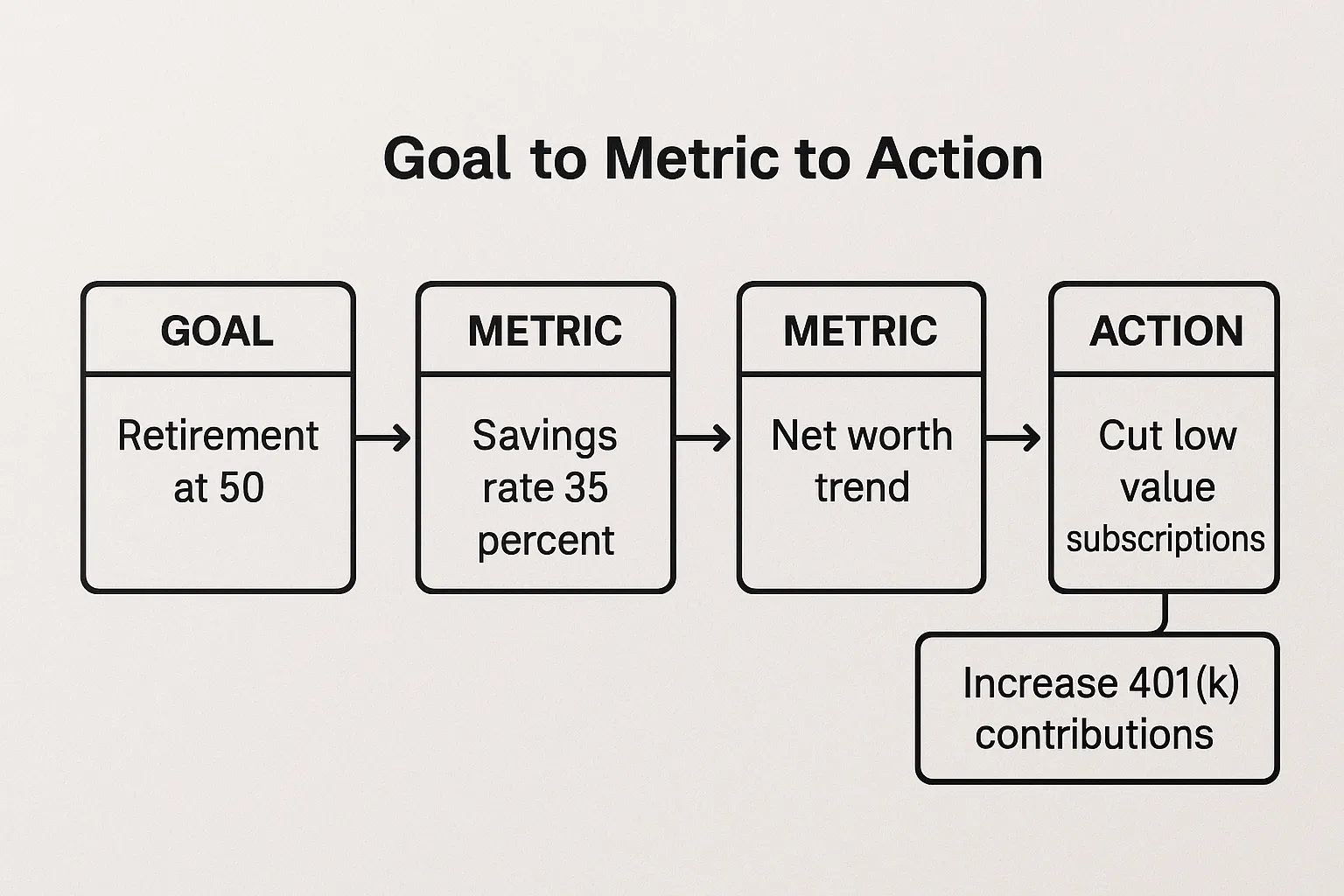

Tie these numbers to actions. If the 12 month savings rate slips, revisit subscriptions and high impact categories, or use the tactics in our Step by Step Guide to Financial Freedom.

Real world scenarios and how FIYR helps

Irregular income, creators, freelancers, and gig workers

- Dynamic budgets and the safe to spend balance help you adjust quickly in lean or fat months without derailing goals

- Transaction rules keep categorization consistent even when income sources shift

- Labels let you track projects or trips across categories without creating category sprawl

New families and first time budgeters

- Custom categories make room for childcare, healthcare, and new fixed costs without losing visibility on Fun and Giving

- Subscription tracking curbs creep during busy seasons

- Goal tracking keeps the emergency fund, debt payoff, and a future down payment visible alongside daily spending

Small business owners and self employed users

- Separate personal and business categories for clean cash flow views

- Use labels to tag business travel or equipment purchases for quick rollups

- Net worth tracking shows how personal assets and liabilities change as the business grows

Investors focused on long term compounding

- Net worth, savings rate, and contribution charts make investing progress tangible even when markets are choppy

- For a deeper dive on withdrawal math for future planning, see Unlocking the 4 percent rule. Modeling tools like FIRECalc and Portfolio Visualizer are also useful context, both discussed in that guide

Coming from Mint, Quicken, Monarch, or Copilot

- FIYR offers more flexibility and transparency than legacy apps like Mint or Quicken, with modern categorization, rules, and customizable net worth and goal tracking

- Compared with premium tools like Monarch Money or Copilot Money, FIYR emphasizes simplicity, customization, and affordability while keeping the features long term planners actually need

- Instead of trying to mirror an old category mess, start fresh. Build the category groups you want for the next decade, set transaction rules, then add labels for trips and projects. Your future self will thank you

Common mistakes to avoid

- Tracking everything but never connecting it to goals, always tie spending and budgets to goals in the app

- Ignoring savings rate, the best way to pull your FIRE date forward is to raise this number

- Creating too many categories, use labels for one off projects and keep categories simple

- Letting subscriptions run on autopilot, review and prune quarterly

- Chasing short term market noise, focus on contribution rate and asset allocation instead. For foundational investing principles, see Index Fund Investing for Beginners

The bottom line

The best wealth tracker app for long term goals connects daily choices to your 10, 20, and 30 year outcomes. FIYR does that by combining a full money and spending tracker, flexible budgeting with safe to spend, custom categories, rules and labels, subscription tracking, comprehensive net worth tracking, and FIRE focused guidance with savings rate and projection tools.

If your destination is financial independence, FIYR is built to be the map. Get oriented with Unlocking FIRE, pressure test your withdrawal plan with the 4 percent rule, raise the lever that matters most with Boost Your Savings Rate, then keep investing simple with Index Fund Investing for Beginners. Your numbers, your plan, your future.